Rate Influencers: When people ask, “What’s the best rate?” most just want you to reel off a number with minimal complexity. Many don’t realize all the elements that determine mortgage pricing. That’s why it’s almost impossible to spit out an accurate quote on the fly. If you want a standard 5-year fixed, for example, factors that impact your mortgage rate include but are not limited to:

Macro-economic factors (such as economic growth, inflation, fiscal policy, etc.)

Discounting (Is the lender willing to sell for less to gain market share? Will the mortgage salesperson buy down the customer’s rate using his/her commission?) This multitude of considerations is why today’s rate comparison sites are meant to be the starting point for rate research, not the final word. There are still factors we can’t assess for you, for example, like credit and property type. But given time we’ll be factoring in these too. That’ll make your journey here much more efficient.

RBC cuts: The golden lion trimmed a bunch of fixed rates on Wednesday, including:

The following special fixed rates:

1yr: 2.74% to 2.64%

2yr: 2.39% to 2.29%

3yr: 2.49% to 2.39%

4yr: 2.54% to 2.44%

5yr: 2.59% to 2.49%

7yr: 3.24% to 3.14%

The following special variable rate:

5yr: 2.25% to 2.15% (prime – 0.30%)

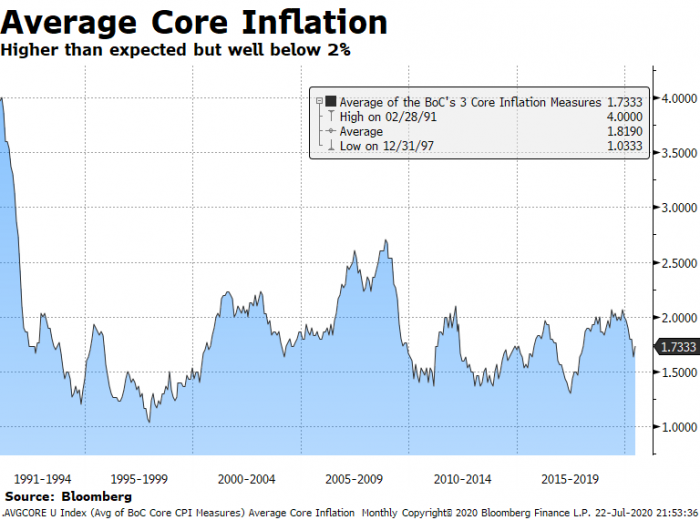

Inflating: Average core inflation surpassed expectations Wednesday, coming in at 1.73%. The bond market didn’t care. We’re still comfortably below the Bank of Canada’s 2% target. And until core inflation exceeds that number, rate hikes aren’t on the table (claims the BoC).

Stat of the Day: “…The number of immigrants arriving to Canada dropped by 80% year-on-year in April,” says TD Economics. That’s bad news for landlords near-term and negative for home values longer-term (since immigrants take a few years to buy, on average). TD says that will contribute to a “mild decline next year” in home prices.

S&P Affirms: That Canada still has AAA credit, in its opinion. (The story)

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Hi meems, They’re both important. A smaller down payment (<20%) will actually get a qualified borrower a cheaper insured rate. Although, if you factor in the insurance premium the total borrowing cost will usually be more. A down payment of 35%+ will often yield the lowest uninsured rate.

Meanwhile, high debt ratios (e.g., greater than 42-44% of gross income going towards housing and debts) can disqualify you from the lowest rates altogether. Those with extreme debt ratios (50%+) pay rates that are 2-3 points higher, minimum.

Hi Ratespy. Thanks for everything you do!

Small mortgage up for renewal < 200k. Offered 2.04 5yr fixed or 2% 5yr variable. Typically we've done variable. 50% chance we can be mortgage free in 3 yrs with prepayments. Should we go variable or fixed?

Hi RateSpy, regarding having a good credit score, is there a specific score one generally needs to get the best rates? Or does it kind of work on a sliding scale?

Thanks!

log in

log in

5 Comments

Hi. I’m just wondering, is down payment more important than debt ratio for determining a mortgage rate?

Hi meems, They’re both important. A smaller down payment (<20%) will actually get a qualified borrower a cheaper insured rate. Although, if you factor in the insurance premium the total borrowing cost will usually be more. A down payment of 35%+ will often yield the lowest uninsured rate.

Meanwhile, high debt ratios (e.g., greater than 42-44% of gross income going towards housing and debts) can disqualify you from the lowest rates altogether. Those with extreme debt ratios (50%+) pay rates that are 2-3 points higher, minimum.

Hi Ratespy. Thanks for everything you do!

Small mortgage up for renewal < 200k. Offered 2.04 5yr fixed or 2% 5yr variable. Typically we've done variable. 50% chance we can be mortgage free in 3 yrs with prepayments. Should we go variable or fixed?

Hi RateSpy, regarding having a good credit score, is there a specific score one generally needs to get the best rates? Or does it kind of work on a sliding scale?

Thanks!

Hi FT Buyer,

You’ll want to target a score of 700+ to get 99%+ of the best rates out there.

A score of 680-699 also gets you most of the best rates but you’ll miss out on a few.

This is assuming you meet all other general underwriting guidelines of course.