log in

log inThere’s a widening chasm between what the Bank of Canada is telling Canadians about inflation and what corporate leaders expect.

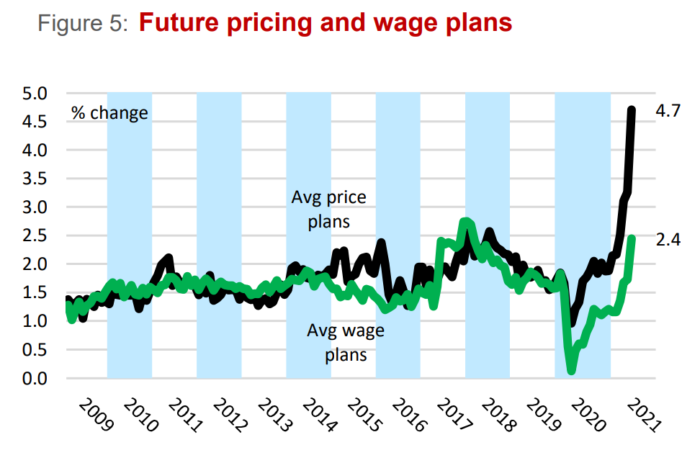

The following chart ain’t pretty, and it contrasts starkly with the BoC’s inflation outlook.

This graph from CFIB shows that businesses now plan to boost prices by 4.7% in the next 12 months.

That is not only 135% more than the BoC’s 2% mid-point target for inflation, it “is by far a record high,” writes Capital Economics.

Meanwhile, the BoC’s last monetary policy report in April forecasted inflation at just 2.3% in 2021—and 1.9% next year. With that kind of divergence, mortgagors with floating rates or an upcoming renewal have a right to be worried.

But When the BoC Hikes, Won’t Rates Eventually Fall Again?

Absolutely. There’s a chance rates revert lower in 4-5 years — after the Bank of Canada’s monetary tightening stalls economic growth.

And sure, this current bout of inflation will also simmer down to some degree, likely within 6-12 months, economists say (for whatever that’s worth).

But despite the BoC assuring us that today’s high inflation is “transitory,” only inflation from base effects (i.e., that caused by abnormally low inflation one year ago) is guaranteed to be short-term.

Inflation from temporary re-opening demand and temporary supply chain disruptions is a different story. It’s transitory too, but it’s not just short-term.

As CIBC Capital Markets’ Royce Mendes pointed out Friday in his podcast (one of the best macro rate commentary shows in Canada), if these two “transitory” inflation drivers last long enough to overlap with the natural “persistent” inflation resulting from an economy that’s back to pre-pandemic levels, we have a problem.

“And that’s exactly what’s going to happen,” Mendes predicts.

How much will escalating rates sting borrowers in the next 3-4 years? That depends on the unknowable, such as:

- Will we have another lockdown that defers rate increases?

- Will the BoC fall behind the curve on battling inflation and need to break its back with more hikes, sooner?

Mendes believes it will. “…The pace of hiking could be faster than the market anticipates,” he says, with the market currently expecting a terminal rate of 2% sometime in 2025 or 2026. If he’s right, then at current rates a 5-year fixed could easily outperform a variable, based on 5-year interest cost alone.

The Crux of the Matter

The burning question in financial markets today is: How long will core inflation stay elevated (e.g., above 2.50% or so)?

If one believes the BoC’s and economists’ projections, it won’t be long. But if we get five to six-plus months of worrisome inflation, you’re going to see central bankers turn hawkish “fast,” says former Fed Vice Chair Alan Blinder.

Is that possible? Of course. It’s been decades since inflation expectations were this detached from central bank targets. Supply shortages, pent-up spending and record government spending aside, this is the best opportunity companies have had to raise prices in ages. And they’ll raise every cent they can because, after all, people expect it.

That leads us to an underlying danger. If ordinary people believe they’re not earning enough to keep up with inflation, they’ll demand higher wages, fuelling an inflation cycle that can take many quarters or years to reverse.

That’s not an outlook typically viewed as compatible with a variable-rate mortgage. Let’s see what happens…

Sidebar

- The BoC is making things too complicated with so many different inflation measures, say critics. “CPI excluding food, energy and indirect taxes is the best measure to forecast total inflation,” writes Scotia Economics. “Not only is that measure of inflation best explained in a Phillips curve framework, it also beats other measures at forecasting total inflation by a wide margin since 2017 (when the BoC launched three additional inflation measures).”

6 Comments

Well, at least lumber is on it’s way back down to US$600/mbf.

https://www.cmegroup.com/markets/agriculture/lumber-and-softs/random-length-lumber.html

This was a great piece that I think more people should glance. I read a great article one time that described central bankers reporting on inflation like “putting the wolf in charge of the henhouse and asking it to report on the well-being of the chickens”. I also really liked how you related everything back to variable-rate mortgages to keep everything in perspective. It’s important to know what’s going on but also to keep asking “how is this going to impact me”. Thanks for sharing!.

The government keeps coming out with new inflation indicators because they don’t like the readings on the current indicators. There is major inflation manipulation going on IMO at the federal level.

I think all indicators world wide are indicating that inflation is picking up speed and momentum. The aspect of inflation that most models do not include is the psychological aspect. Once the regular person gets a sense that inflation is here and speeding up, they will start to buy more essentials before prices rise. they will hoard items and this will increase demand and increase money velocity, both of which will increase inflation. Interesting times ahead.

Inflation is made worse mostly by surging gas prices. Oil – the most manipulated thing in the market

The BoC will raise rates to create another ‘crisis’ like covid and then it will have the solution already planned, are you ready for this…lower rates:)