log in

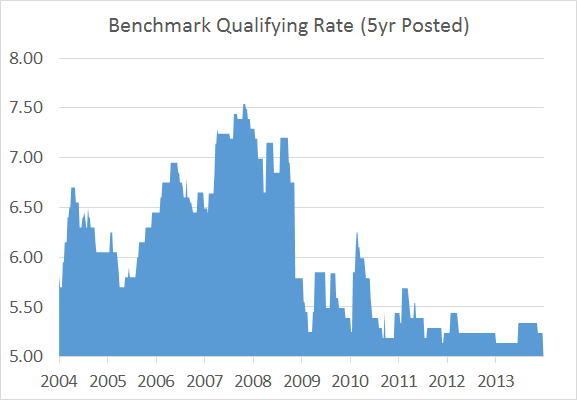

log inThis week the Bank of Canada’s “benchmark rate,” a measure of 5-year posted mortgage rates, dropped to an all-time low of 4.99% (from 5.24%).

The benchmark rate is an important number used by lenders to qualify you for a mortgage (i.e., calculate how big of a mortgage you can afford).

It’s also used as the basis for:

• Cashback mortgage rates

• Rate guarantees – This applies predominantly to the retail (non-broker) channel where many lenders still price off the posted rate, and offer the lower of the rates available at the time of approval or closing.

• Calculations of mortgage prepayment charges (aka. early breakage penalties)

• Capped variable rates (i.e., variable rates that have an upper limit)

The benchmark qualification rate applies to people getting mortgages with either a variable rate or a term less than five years, at a federally regulated lender–like a bank. (The method differs for people getting fixed mortgages with a 5-year term or longer. For those folks, lenders still qualify them using the actual rate of their mortgage.)

Here’s an example of how the new 4.99% qualifying rate affects things.

Prior to this week’s change, you could go into a bank and get a $300,000 variable rate mortgage with roughly $66,450 of income. (Based on a 5.24% qualifying rate, a 25-year amortization, a maximum 39% gross debt service ratio, 1% property taxes and no other debts.)

Now, with the qualifying rate falling to 4.99% you need to earn just $65,245, about 2% or $1,200 less.

Put another way, variable and 1- to 4-year fixed borrowers can now qualify for roughly a 2% bigger mortgage.

More about the Benchmark Rate

• You can find the current Benchmark rate here (look for data series V121764)

• It is calculated as a mode average of 5-year posted rates advertised by the six biggest banks (BMO, CIBC, National Bank, RBC, Scotiabank and TD) at noon Eastern time each Wednesday.

• “Mode average” refers to the number repeated most often. For example, suppose these are the 5-year posted rates for the Big 6 banks: 4.85%, 5.09%, 5.09%, 5.24%, 5.34%, 5.49%. The mode average (and hence the Benchmark qualifying rate) would be 5.09%.

• The Benchmark rate is posted on the Bank of Canada’s website every Thursday by approximately noon Eastern time.

Factoid

• Prior to last week, Scotiabank was the only Big 6 bank with a 4.99% posted 5-year fixed. It dropped to 4.99% in March 2012–two years ahead of competitors.

• Why didn’t other lenders drop their 5-year posted rates sooner? One reason, according to a banker we spoke with, was that “Lenders were very resistant to dropping (the 5-year) posted rate because of what it might do to their pipeline” (e.g., it would have forced some lenders–who price rate guarantees off posted rates–to offer lower rates to people at the time of closing, in cases where rates fell after those people had applied).