log in

log inBy Chantal Chapman, Special to RateSpy

If you’re a homebuyer with a down payment less than 20%, you’re now subject to Canada’s new mortgage rules. As a prospective purchaser, you probably want to know where you stand. Here’s a quick rundown…

The biggest change you’ll face is the government’s new “stress test.” It forces insured borrowers to prove they can afford a payment at the Bank of Canada’s 5-year fixed posted rate (currently 4.64%). The purpose is to ensure you can handle your payments if interest rates soar. The side effect is that it reduces the mortgage size you can qualify for.

Your credit score matters more than ever

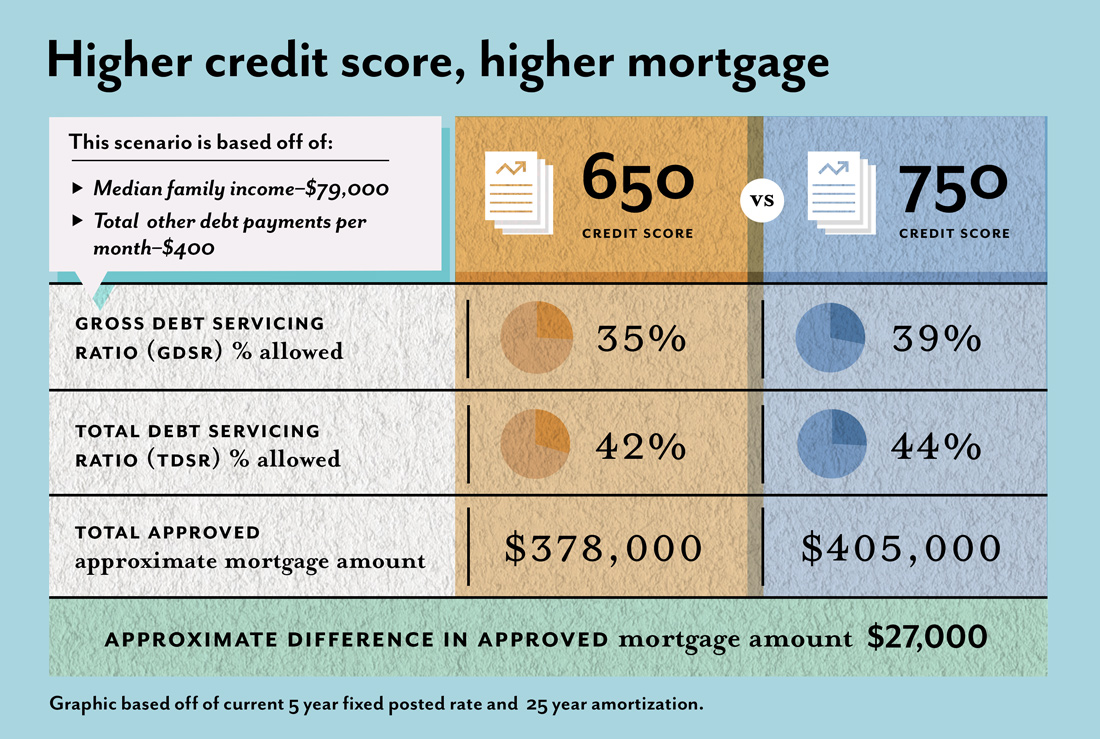

Canadian lenders must follow specific rules if your mortgage is insured by CMHC, Genworth or Canada Guaranty, which is typically required if your loan-to-value is above 80%.

These lenders and insurers measure you against standard “debt service ratios”—specifically the Gross Debt Service Ratio (GDSR) and Total Debt Servicing Ratio (TDSR)—to determine if you can cover all of your monthly obligations and mortgage payment.

GDSR is your mortgage payment, heat, taxes, and 50% of any condo/strata payment, divided by your monthly income.

TDSR takes the calculation above and adds other debts like credit cards, lines of credit, car loans, etc., and divides all that by your monthly income.

The limits of your debt ratios (for mortgage approval purposes) depend largely on your credit score.

- If your score is under 680, your max GDSR is 35% and your max TDSR is 42%

- If your score is over 680, your max GDSR is 39% and your max TDSR is 44%

Here’s a calculator where you can check your ratios: Click

What does this all mean?

People with higher credit scores get rewarded with more borrowing flexibility—an additional four points on the GDSR and two points on the TDSR.

That means you can get a bigger mortgage with the same amount of income. (Whether borrowing more is wise is another matter.)

For example, someone with a household income of $79,000, a credit score of 650 and $400 a month in debt payments, will have a GDSR limit of 35% and a TDSR limit of 42%. At that calculation you’d be approved for a mortgage of approximately $378,000 (based on today’s five-year posted rate and 25-year amortization).

Now take all of the same factors and apply it to someone with a higher credit score of 750. This person can have a GDSR up to 39% and a TDSR up to 44%. (Note that lenders consider anything above a 35% GDSR and 42% TDSR to be an exception, which generally requires a stronger overall application.)

Now, all of a sudden this stronger-credit borrower can get approved for a mortgage of roughly $405,000. That’s a meaningful jump. We’re talking $27,000 (7%) more buying power when you’re out shopping for a home. (see table)

How do you get your score up?

Two of the biggest things that impact your credit score are missing payments and your credit utilization ratio (i.e., how much of your credit you have used). These factors make up 35% and 30% of your score, respectively.

If your score is below 680 and you’re hoping to buy a home, you’ll want to improve it. Not only does a higher score let you borrow more (mind you, we don’t recommend pushing your TDSR above 38-40%) but you’ll save on your interest rate too. That’s because some lenders reserve their best rates for folks with scores of 680 or above.

If your score is low strictly because of utilization, you can improve it in as little as 30 days. The trick: pay down all of your loan balances (particularly your revolving credit) so that they are less than 70% of your credit limits.

If your score is low because of your payment history, it will gradually improve over about 12-18 months with on-time payments. Just make sure you have at least two accounts (loans, credit cards, etc.) that are reporting to the credit bureau, each with a credit limit of at least $2,000.

The recent mortgage rule changes are out of your control, but having a strong credit score is in your control. So if you’re planning to own a home, bolstering your credit is a smart first step.

Chantal Chapman is a credit score expert and Financial Fitness Coach for Mogo who is passionate about educating millennials on personal finances. She is also the founder of Holler for Your Dollar, a financial consulting firm that jump-starts anyone who’s ready to dive into entrepreneurship. Prior to that, Chantal was a Vancouver-based mortgage broker for over a decade.

2 Comments

I think Rob wrote an article about an unscrupulous telco sending accounts to collection shortly after a customer ports their cell service to a new provider. Telus did this to my wife, knocking her score down significantly with a R9. Even though credit bureau rules say R9 is for debt more than 120 days past due, they let companies mark an account R9 after as little as 30 days past due.

Hey Ralph,

I feel ya man. Virgin Mobile shafted me the same way. The phonecos do this all the time to people and it’s an out-and-out travesty.

It’s a further slap in consumer’s faces that the credit bureaus report this garbage like they report regular accounts. Compared to one’s payment history on revolving or installment credit, how people handle their cell phone bills is often a much weaker indication of how they’ll pay an important trade line, like a mortgage.

Almost no other companies infuriate consumers more than telcos. Some people just tell them to screw off because they’ve been treated so poorly, and don’t pay their bill. Then they find they can’t get a mortgage because their score dropped 90 points. It’s repugnant and consumer rights groups should be all over it.