log in

log inSome quick hits on the mortgage/rate market (we’ll update these throughout the day):

4:14 p.m. Update

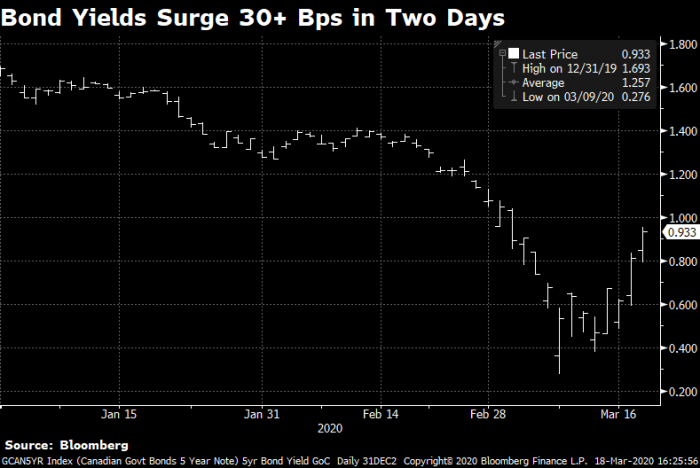

- Yields Soar: Canada’s 5-year bond yield launched 13 bps today as investors sold everything that wasn’t nailed down, including stocks and bonds, and rushed into cash. Rocketing bond yields are bullish for fixed mortgage rates and we’re seeing more lenders, including banks, react by lifting fixed rates again today.

- Spread’s Narrow a Tad: On a positive note, most key credit (risk) spreads decreased slightly. Lenders are watching credit spreads like a hawk. They’re a key element in many mortgage pricing models.

- Oil devastation: Crude prices (WTI) crashed to a 17-year low of $21.25. Given the economic pain this will cause (lost investment, unemployment, corporate defaults, etc.), it’s hard to fathom the BoC waiting much longer to cut rates again. The bond market is still pricing in another 50 bps in cuts.

12:25 p.m. Update

- BoC on Credit Liquidity: “The plumbing is working,” said Bank of Canada Governor Stephen Poloz at a press conference today, noting that the virus crisis is “temporary.” But he added, “We honestly don’t know what’s coming our way.” The Bank of Canada will assess the inflation impact of today’s $82 billion of fiscal aid before deciding on the next rate cut. This suggests somewhat lower chances of an emergency rate cut before its April 15th meeting, but Poloz said he’s not ruling it out.

- CMB Spreads Narrow: The difference between the “risk-free” 5-year Canada Mortgage Bond (CMB) yield and the 5-year government bond yield has narrowed meaningfully since the Bank of Canada started buying CMBs this week. That’s modestly good news for lenders, and by extension, fixed mortgage rates.

Source: Bloomberg

12:25 p.m. Update

- HELOC Bargains: Given the fact Canadians may start tapping HELOCs in record numbers, it’s astounding to see some lenders still offering HELOCs at a discount to prime rate. This will not continue. The latest HELOC rates.

11:50 a.m. Update

- Government Commitment: The Finance Minister says he’ll do “whatever it takes” to help the country cope with COVID-19’s financial hit. Measures announced today include deferring tax payments “until after August 31, 2020.”

11:18 a.m. Update

- Gauging Fallout: A global recession is underway, say Goldman Sachs and Morgan Stanley. In a worst case scenario, JP Morgan estimates 60% of Canada’s economy could be severely impacted by it. Additional Bank of Canada rate cuts will have little impact, but there is no reason for the overnight rate to not be near zero already. Odds are, it will happen soon. If the current trend in banks passing through BoC stimulus continues, banks should cut prime rate to 2.45%, or thereabouts, by next month.

- Proactive Measures: Policy-makers are doing a tremendous job providing emergency liquidity to mortgage lenders. So far, it’s working reasonably well. But, friction in the funding market is nonetheless forcing mortgage rates higher at most lenders.

10:19 a.m. Update

- Unprecedented Move: Big banks plan to defer people’s mortgage payments en masse up to six months, something that’s virtually unheard of. The story. Default insurer CMHC will allow 6-month deferrals as well, on insured mortgages. “We are also exploring, with others, potential relief measures for those who cannot make payments on uninsured mortgages and renters,” said Evan Siddall, president and CEO of CMHC (Source: CBC).

- Variable Outlier: HSBC has bucked the trend today by not slashing its floating-rate discounts from prime rate. It lowered its variable specials as follows:

5yr variable (purchase/switch): 2.34% to 1.84%

5yr variable (refi): 2.44% to 1.94%

HSBC now leads the nation with the lowest insured and uninsured 5-year variable rates. - Oil Collapsing Again: WTI crude is down to $24 a barrel, further raising the probability the Bank of Canada will cut another 50 basis points by April 15 or before.

9:58 a.m. Update

- Fixed Rates on the Rise: Amid higher risk/liquidity premiums in the funding market and yesterday’s surge in bond yields, RBC has raised its “special” fixed mortgage rates by up to 40 bps:

1yr: 2.94% to 3.14%

2yr: 2.69% to 2.99%

3yr: 2.69% to 3.09%

4yr: 2.74% to 3.14%

5yr: 2.94% to 3.34%

7yr: 3.09% to 3.49%

RBC’s variable mortgage rate remains at prime – 0% (2.95%), a multi-quarter high.

18 Comments

Yesterday you noted that the stress test was coming down to 5.04, any update on that?

Hi Tyler, Yep. Based on current rates it’s still slated to drop to 5.04% today. The Bank of Canada doesn’t update its website until tomorrow, however. Here’s the link: https://www.bankofcanada.ca/rates/banking-and-financial-statistics/posted-interest-rates-offered-by-chartered-banks/

I have 2 days to decide to renew at 2.29% fixed or prime -1.10%. Normally I choose variable but I feel banks are crooks and they could raise rates if they want to screw us.

Hi there

Where are you getting 2.29…. one of the big banks. ?

Thanks

@Niko

If your variable rate discount (-1.10%) is locked in, you’re not going to get screwed (by the bank) during the length of your term. -1.10% is fantastic. Sure, prime could skyrocket, but I can’t see how that is going to happen within a 5-7 year period.

My mortgage is due in May.

But should I lock into 2.64 percent with RBC early?

Debating if I should.. or if that’s even a good rate. Paying 2.69 now.

Just dont want to wait a month or two and kick myself for not locking in if it goes up.

OR it could go down

Hi Kyle, A few thoughts:

1) Make sure a 5-year fixed is right for you as there are other terms at attractive rates right now: https://www.ratespy.com/compare-lowest-mortgage-rates

2) Think about whether RBC is the best fit good fit given its less favourable penalty and prepayment policies, and given your personal situation

3) While not a firm prediction, there’s a chance fixed rates climb a bit in the next 30-60 days. If you’ve settled on a 5-fixed at RBC, use competitor’s rates as leverage in your negotiations and hold a rate (also note: many competing lenders provide cash back if your mortgage is big enough)

First National offered me 2.29% on a renewal. its up to 2.39 now.I have a choice of that or variable at prime -1.10?.

Just got 2.49 on renew fixed rate cibc

Solid.

My son and his wife need to re-negotiate their mortgage with RBC. It is due on April 4th – 5 year fixed at 2.79. They were offered 2.84 a week or so ago but when they emailed yesterday asking for 2.59 posted on RateSpy, they finally got a reply today which is offering them 2.99.

I told my son to ask about the RBC 2.74 – 5 year fixed which is on RateSpy this morning (apparently for new customers? according to RateSpy small print). My son and his wife are lower income and every dollar counts as they raise two small children.

Please advise, and many thanks for your great site and updates.

With gratitude, George B.

Thanks George, Please read this: https://www.ratespy.com/all-about-discretionary-rate-estimates-02231226

Just renewed my mortgage with Rbc at 2.44 5 yr fx

Dobby: Solid.

I was offered renewal rate( after some negotiations) 2.39% 3 year fixed by RBC on Tuesday.

Thanks @ TheSpy for your response yesterday explaining how you come up with posted rates. My son asked for 2.74% as your site indicated for RBC but they have refused and told him to accept their good deal offer of 2.99% over 5 years. Yes, he would have been better off acting sooner but his wife has been working 12 hour nursing shifts at local Toronto hospital to keep public safe and is fatigued. RBC knows this but banks have no emotion. Son and wife do not have wherewithal to explore elsewhere. Many thanks, George.

Anything under 3% is tremendous historically. The best to your family George. -rob

George, back in November First line offered me a renewal rate at 2.89%. My renewal date is March 27. I refused their rate thinking rates should go down in the next few months and their constant calling to accept basically solidified my thinking. Banks don’t offer great rates unless there’s something that they are going to profit from. Since then they kept lowering the fixed every month to 2.29% on March 9. They never offered me a variable rate until I asked and even then they kept pushing the fixed. So that basically told me to do the opposite of what the bank suggested and took the variable at prime -1.10%. I may be wrong but I’ve been variable for a long time and I just don’t see rates going up in the near future. My wife is also a nurse at a cancer centre and I’m a firefighter in Toronto and I can tell you that we have a long way to go before this COVID 19 things goes away. It’s not just RBC it’s all banks and major corporations. They don’t give a crap about anything except for profits. Take care and wash your hands.