Fleeting Deal: Canada Life’s stellar 5-year fixed deals (2.34% insured and 2.49% uninsured) could vamoose this week. If a fixed 5-year is suitable for your circumstances and if you’re closing in the next 90 days, it’s a hard deal to beat. Unfortunately, for those who like a long payback period, Canada Life only allows up to a 25-year amortization. No 30s. (P.S. If you call a Canada Life mortgage rep, ask them if they can do a little better. We hear they have some discretion on the rate.)

RBC: “We expect property values to fall briefly: Surging unemployment and the market’s illiquidity will compel a growing number of tight-squeezed [home] sellers to make price concessions…We think the recovery will come in stages—taking buyers up to a year to regroup and rebuild confidence amid high unemployment. Based on these assumptions, we project home resales to dive by nearly 30% this year in Canada to a 20-year low of 350,000 units.” In AB and much of SK, however, all bets are off.

More Bank Relief: To provide further access to mortgage capital, the banking regulator is now letting banks issue more covered bonds (CBs). Whereas banks could previously issue up to 5.5% of their assets in CBs, they can now (temporarily) issue up to 10%. But the extra 4.5% must be sold to the Bank of Canada. It’s a smart move by OSFI that will shore up bank funding, and ultimately pay off for consumers by way of lower uninsured mortgage rates.

Deposit Anomaly: Deposit rates are climbing, something you wouldn’t expect given a 150-bps plunge in Canada’s key interest rate. The main driver: banks are lifting deposit rates in hopes of attracting cheaper capital than they can raise through other avenues—all of which have become more expensive. Rising deposit rates are just one more factor keeping mortgage rates buoyant, especially at non-prime lenders that rely far more heavily on deposits than Big 6 banks.

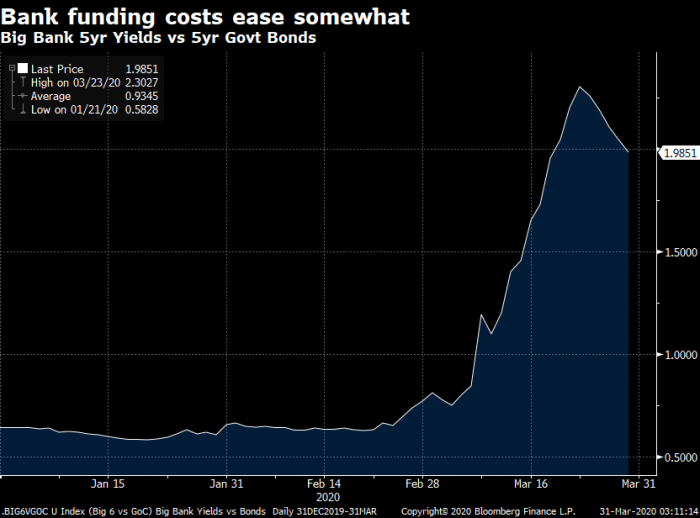

Some Mortgage Spreads Narrow: In the last seven days, the risk/liquidity premiums that banks have been forced to pay investors for longer-term lending capital have eased a bit. We can thank government intervention for that. This takes some of the upward pressure off fixed mortgage rates, for now. The cost of short-term funds—like those used to finance variable-rate mortgages—have not improved in a similar fashion.

Source: Bloomberg

Tip of the Iceberg: Jobless claims now represent about 8% of the workforce, and are just getting started.

Another Tough Day: Alberta oil (WCS crude) fell to another record low on Monday—just $4.26 a barrel. At this pace, it’ll be free pretty soon. The lower oil drops, the more worried Alberta lenders get.

Historic Relief: A summary of the government’s massive COVID-19 relief package, from NBC. Canada saw a fraction of this support during the 2008 credit crunch, which shows how serious of a mess we’re in.

9:29 a.m. Update

This Act of God is No Out: Buyer’s remorse from COVID-19 is no excuse to back out of a home purchase, write Haider & Moranis, who add: “…Standard residential real estate transactions do not include force majeure provisions.”

Income Interruption Before Closing: CMHC told us this about insured borrowers who get laid off before their mortgage closes: “The mortgage insurers provided further guidance to lenders on the treatment of applications, in light of the current environment related to COVID-19. Where a lender has been advised that a borrower with a previously approved application is experiencing income disruption due to COVID-19 and the borrower still wants to move ahead with the application, the mortgage insurer may proceed with its previous mortgage loan insurance approval under certain conditions. Note that each application is treated on a case-by-case basis and that it is up to the lender to decide if the application may move ahead or not.”

Bank Rate Updates: Following the BoC’s half-point rate cut on Friday, banks dropping advertised floating rates to prime + 0% seems to be the trend:

CIBC lowered its variable rates by 50 bps:

3yr closed: 2.95% to 2.45%

5yr closed: 2.95% to 2.45%

5yr open: 4.75% to 4.25%

RBC also cut its variable rates by 50 bps:

5yr closed: 2.95% to 2.45%

5yr open: 5.45% to 4.95%

5yr closed (Special): 2.95% to 2.45%

TD dropped its variable rates 50 bps as well:

5yr closed: 3.15% to 2.65%

5yr open: 4.10% to 3.60%

Bearish on Home Values: Expect many more real estate bears to emerge from hibernation. They’ll be echoing comments from the likes of economist David Rosenberg, who told BNN last week: “The big underpinning [for housing] has been this immigration wave…That underpinning is gone.” And, “When you have a situation when people are…losing their jobs…the housing market from the domestic demand side is going to be very weak…We’re going to be in for a very significant correction—especially in the GTA—in residential real estate for the next several months, if not longer than that.” Showings in the GTA are reportedly down over 80%+ in the last few weeks.

Rate Cuts Won’t Juice Housing: Senior Deputy Governor of the Bank of Canada, Carolyn Wilkins, stated this week, “It’s unlikely that the housing market is going to be fuelled…in an uncomfortable way” by the BoC’s rate cuts.

2022: “…We don’t forecast the Fed hiking until after 2021…”—Priya Misra, Head of Global Rates Strategy at TD Securities (via Bloomberg)

Renewers Beware: Anyone who wants to switch lenders and has a maturity date (renewal date) in the next ~30-40 days closing should get confirmation in writing that the new lender can close that quick. If there’s any doubt, ask your existing lender to renew you into an open mortgage, if possible.

Swamped Phone Lines: A banker we spoke with this weekend thinks banks have received 250,000+ requests for mortgage payment deferrals. Last week, as just one example, Scotiabank’s head of real estate secured lending, John Webster, said on a DLC Group webinar that the bank has been getting 20,000+ mortgage-related calls a day. Most of them are for mortgage payment deferrals. And that’s just the tip of the iceberg because the unemployment spike is only beginning. We’re two days away from the first of the month. Many who haven’t been able to arrange payment deferrals will miss their mortgage and rent payments. We’ll start seeing the fallout from that intensify in the next 1-3 months.

Double Hump: Just when people think a pandemic is licked, superbugs often make a return engagement, as these historical charts of the Spanish Flu — with two humps or waves of the virus — demonstrate.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Mr Spy,

I have a fix 4yr with 2.69% which I got 5mo ago. With current situation I also got approved for variable 5yr with prime-1.01%. I am hesitant to switch since I need to pay $8k penalty, and I am not sure how long prime will stay low. Mr. Spy, based on your experience and my current rate and penalty, do you think it is wise to switch or I will loose money long run??

@David64 FYI, your penalty might double. I assume the penalty is using the posted rates in the calculation. If the banks were to drop the posted rates by .25-.50, then you might be paying more, which could be a lot more. (I know this because my penalty to break my mortgage jumped form 8200 to 14000….and it could jump again)

You have to do the math. Say you got 1.47%, on a 500k mortgage, you’ll save 295.83 per month * 12 * 5 = $17,749.8 and you’ll pay an extra $10,600 off your mortgage. Lots of assumptions here, like rate saying 1.47, which mostlikely be 1.5years, but then most-likely creep up. One article Ratespy said BoC will probably do 3 0.25% increases in a row.

Hi Fabian, It’s our pleasure, thanks for reading. While we can’t make a personal recommendation on this forum, I can say this. Most folks with a remaining amortization of just 5 years have lots of equity and a low balance. For those reasons and the fact that so much of their payment is going towards principal each month, they can usually take more risk. For the majority of folks in this situation (there are exceptions), they’re usually best served with the lowest possible rate they can find — with ample prepayment privileges and a fair prepayment charge. Just be sure the switching costs are cheap enough if you change lenders, so you’re not consuming all of the interest savings.

“RBC already reduced their posted rate by 39bps just 3 weeks ago. That increased my penalty from 5k to 9k. You think they will reduce it again?”

Therein lies hidden devil in big bank mortgage contracts.

@David64: The trend this month has been an increase in posted short-term fixed rates. But it’s impossible to say what will happen next and when. The market is extremely volatile.

@Michelle, go wih the 5yr variable. One great thing about TD is that you can lock in to a 3-5yr fixed from the 5yr variable without penalties. Once fixed rates drop well below 2.53%, lock into a 3 or 4yr. I’d avoid locking into a 5yr given the risk of higher penalties if you need to get out of it early.

Mr Spy my current mortgage rate is prime – .10 with B2B Bank. My current mortgage bal. is $307,000. My renewal is next year around august. I am currently occupying the property. I do not have a Heloc . Is it advisable to break the mortgage & find a new lender with better rates ?

Hi AR, The penalty might eat up the interest savings. But if you have some other reason to refinance or lock in, it might make sense. Run your situation by a mortgage advisor to confirm.

Hi Pilo, Would genuinely love to help but there’s just not enough info here to make a call for you. And we can’t make personalized product recommendations in this forum anyhow. The right choice depends largely on your 5-year plan and financial circumstances. Those are all exceptional rates from a pure interest cost perspective, especially the HSBC variable, but each has its own risks and restrictions.

My mortgage renewal with my bank will be 3rd week of May; my bank has offered me a 5 year fixed of 2.37% (valid till April 30). My current rate with them is 3.49%. Do you anticipate rate to drop further from 2.37%? Thinking about going for early renewal.

Hi Dip, Anything’s possible but given all the funding pressures banks have faced, it would be risky to bet on falling 5-year fixed rates in the next 30 days. 2.37% is a superb rate for a 5-year fixed. That is, assuming a 5-year term is right for the borrower, and assuming the bank’s features (penalty policy, refinance options, etc.) fit one’s needs.

No one can tell you what to do because no one knows your financial, employment, equity, asset or housing situation. There is more to selecting a rate than trying to guess future rates. No one knows the future.

Hello,

my mortgage renewal is due on June 1st. My current rate is 2.95%. TD is offering me the same deal as above mentioned:

5 YR Fixed – 3.07%

5 YR Variable – 2.53% (prime – 0.07%)

should I go for it or wait and see what happens in the next 2 month?

Hi Dana, Waiting entails risk. It’s smarter to secure a rate today — at TD or elsewhere — and then reassess on May 1. Just leave yourself plenty of time to close (30 days minimum). BTW, I’m not in love with either of those two rates assuming the borrower is well qualified.

In regards to mortgage switches. If my mortgage was insured by CMHC when I first got it 13yrs ago, for rates, do I still qualify for the rates posted up to 95%(loan-value). Mine is at about 50%(l-v) with an excellent credit score. Also, if I switch lenders, how does that work in regards to the extra mortgage (ife) insurance, do we just get to carry it over to the new lender….Credit union, Bank…

Hi Rob, If your CMHC insurance is still in force then likely yes.

As for mortgage life insurance, if it’s lender-sold it’s probably not portable to a new lender. If it’s broker-sold (e.g., from Mortgage Protection Plan) than it probably is.

Has First National dropped their prime rate yet?

On their website still shows 2.95%. We have a variable mortgage so it is obviously very important to us.

long-time follower first time comment.

I’m having my income property re mortgaged at 600k. Looking at buying an income property at 550k, when housing prices drop. I’ve been with the RBC for 35 years, they are saying to stick with the variable rate for both mortgages.

Would you please advise best course of action?

Hi Stonegage, It depends on a few dozen factors (starting rates, your 5-year plan, income situation, debt situation, cash flow requirements, etc. etc.). Best bet is to get independent advice from a broker and compare it to what RBC is saying.

log in

log in

25 Comments

Mr Spy,

I have a fix 4yr with 2.69% which I got 5mo ago. With current situation I also got approved for variable 5yr with prime-1.01%. I am hesitant to switch since I need to pay $8k penalty, and I am not sure how long prime will stay low. Mr. Spy, based on your experience and my current rate and penalty, do you think it is wise to switch or I will loose money long run??

@David64 FYI, your penalty might double. I assume the penalty is using the posted rates in the calculation. If the banks were to drop the posted rates by .25-.50, then you might be paying more, which could be a lot more. (I know this because my penalty to break my mortgage jumped form 8200 to 14000….and it could jump again)

You have to do the math. Say you got 1.47%, on a 500k mortgage, you’ll save 295.83 per month * 12 * 5 = $17,749.8 and you’ll pay an extra $10,600 off your mortgage. Lots of assumptions here, like rate saying 1.47, which mostlikely be 1.5years, but then most-likely creep up. One article Ratespy said BoC will probably do 3 0.25% increases in a row.

Dear Ratespy,

First off this website is an incredible source of information. Thank you!

Question, we are up for Renewal on June 2020. we currently have 2.59% Fixed five years with BMO.

i have 5 years left to the mortgage, should i look into getting a 5 year Variable or fixed mortgage rate?

Many thanks,

Fabian

Hi Fabian, It’s our pleasure, thanks for reading. While we can’t make a personal recommendation on this forum, I can say this. Most folks with a remaining amortization of just 5 years have lots of equity and a low balance. For those reasons and the fact that so much of their payment is going towards principal each month, they can usually take more risk. For the majority of folks in this situation (there are exceptions), they’re usually best served with the lowest possible rate they can find — with ample prepayment privileges and a fair prepayment charge. Just be sure the switching costs are cheap enough if you change lenders, so you’re not consuming all of the interest savings.

My mortgage matures on April 1st! Worst timing ever. TD is offering the following renewal rates:

5 YR Fixed – 3.07%

5 YR Variable – 2.53% (prime – 0.07%)

What to do?? (my current rate is 2.74%)

@Tyler

RBC already reduced their posted rate by 39bps just 3 weeks ago. That increased my penalty from 5k to 9k. You think they will reduce it again?

“RBC already reduced their posted rate by 39bps just 3 weeks ago. That increased my penalty from 5k to 9k. You think they will reduce it again?”

Therein lies hidden devil in big bank mortgage contracts.

@David64: The trend this month has been an increase in posted short-term fixed rates. But it’s impossible to say what will happen next and when. The market is extremely volatile.

@Michelle, go wih the 5yr variable. One great thing about TD is that you can lock in to a 3-5yr fixed from the 5yr variable without penalties. Once fixed rates drop well below 2.53%, lock into a 3 or 4yr. I’d avoid locking into a 5yr given the risk of higher penalties if you need to get out of it early.

Mr Spy my current mortgage rate is prime – .10 with B2B Bank. My current mortgage bal. is $307,000. My renewal is next year around august. I am currently occupying the property. I do not have a Heloc . Is it advisable to break the mortgage & find a new lender with better rates ?

Hi AR, The penalty might eat up the interest savings. But if you have some other reason to refinance or lock in, it might make sense. Run your situation by a mortgage advisor to confirm.

Dear Rob,

My mortgage matured on April 22, I got locked the following rates:

5-year fixed 2.24 (1,500 cash back) MCAP

5-year variable 1.34 ( Prime – 1.11% + cash back $2,000) HSBC

My lender offered Home Trust

5-year fixed 2.44

5-year variable 1.5 (Prime – 0.95%)

What do you recommend? My actual rate 5-year fixed 2.64%

Hi Pilo, Would genuinely love to help but there’s just not enough info here to make a call for you. And we can’t make personalized product recommendations in this forum anyhow. The right choice depends largely on your 5-year plan and financial circumstances. Those are all exceptional rates from a pure interest cost perspective, especially the HSBC variable, but each has its own risks and restrictions.

My mortgage renewal with my bank will be 3rd week of May; my bank has offered me a 5 year fixed of 2.37% (valid till April 30). My current rate with them is 3.49%. Do you anticipate rate to drop further from 2.37%? Thinking about going for early renewal.

Hi Dip, Anything’s possible but given all the funding pressures banks have faced, it would be risky to bet on falling 5-year fixed rates in the next 30 days. 2.37% is a superb rate for a 5-year fixed. That is, assuming a 5-year term is right for the borrower, and assuming the bank’s features (penalty policy, refinance options, etc.) fit one’s needs.

@Michelle

No one can tell you what to do because no one knows your financial, employment, equity, asset or housing situation. There is more to selecting a rate than trying to guess future rates. No one knows the future.

Hello,

my mortgage renewal is due on June 1st. My current rate is 2.95%. TD is offering me the same deal as above mentioned:

5 YR Fixed – 3.07%

5 YR Variable – 2.53% (prime – 0.07%)

should I go for it or wait and see what happens in the next 2 month?

Hi Dana, Waiting entails risk. It’s smarter to secure a rate today — at TD or elsewhere — and then reassess on May 1. Just leave yourself plenty of time to close (30 days minimum). BTW, I’m not in love with either of those two rates assuming the borrower is well qualified.

In regards to mortgage switches. If my mortgage was insured by CMHC when I first got it 13yrs ago, for rates, do I still qualify for the rates posted up to 95%(loan-value). Mine is at about 50%(l-v) with an excellent credit score. Also, if I switch lenders, how does that work in regards to the extra mortgage (ife) insurance, do we just get to carry it over to the new lender….Credit union, Bank…

Hi Rob, If your CMHC insurance is still in force then likely yes.

As for mortgage life insurance, if it’s lender-sold it’s probably not portable to a new lender. If it’s broker-sold (e.g., from Mortgage Protection Plan) than it probably is.

Can one get a 30 year amortization on a uninsured mortgage?

Thanks

Hey Cal, One can *only* get a 30-year amortization on an uninsured mortgage.

Has First National dropped their prime rate yet?

On their website still shows 2.95%. We have a variable mortgage so it is obviously very important to us.

Hi Michal, Yes, 2.45%

long-time follower first time comment.

I’m having my income property re mortgaged at 600k. Looking at buying an income property at 550k, when housing prices drop. I’ve been with the RBC for 35 years, they are saying to stick with the variable rate for both mortgages.

Would you please advise best course of action?

Hi Stonegage, It depends on a few dozen factors (starting rates, your 5-year plan, income situation, debt situation, cash flow requirements, etc. etc.). Best bet is to get independent advice from a broker and compare it to what RBC is saying.