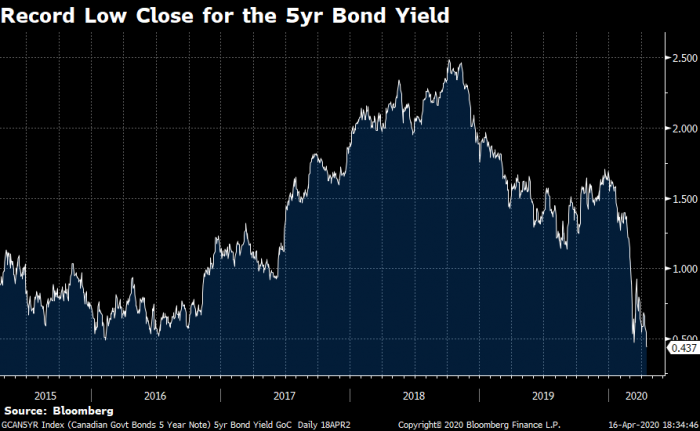

Record Broken: Canada’s 5-year bond yield moves fixed mortgage rates and it closed at another all-time low today. That coincides with a roughly three-week low in risk/liquidity premiums. Together, these two factors are driving fixed mortgage rates lower, with numerous lenders trimming rates 5-15 bps this week.

More Hope: “With a vaccine more than likely out of reach for this year, the near-term hope…rests on finding an anti-viral treatment that can improve the odds of survival…” (Bloomberg story) And an effective anti-viral may be closer than some think. Check out this story.

Fixed-rate Discounts Improving, But…: Normalcy is slowly returning to fixed-rate mortgage pricing. But there’s still a long way to go before borrowers enjoy historical discounts on conventional 5-year fixed rates. This time last year, the lowest widely available uninsured 5-year fixed was 145 bps over the 5-year government bond. Today that that spread is 221 bps. If spreads get back to the 150-bps range in 6-12 months and bond yields linger around these levels, a new borrower with a $300,000 5-year fixed could save up to $17,000+ in interest over five years.

Today’s notable rate changes:

BMO cut three posted fixed rates, which will increase prepayment penalties for BMO borrowers who break their mortgage early:

1yr: 3.64% to 3.29%

2yr: 3.89% to 3.54%

3yr: 4.29% to 4.05%

CIBC is bucking the trend by raising its “special” 5-year fixed rate:

5yr: 2.99% to 3.09%

HSBC lowered several special offers:

2yr fixed: 2.44% to 2.34% (the lowest 2yr in the nation)

5yr variable (high ratio): 2.35% to 2.10% (P-0.35)

5yr variable (refi): 2.65% to 2.40% (P-0.05)

Econo-talk: Economists react to yesterday’s BoC rate announcement (Rates.ca story)

Closer to “Normal”: Most (not all) lenders are reporting relatively normal turnaround times on approvals, particularly given that purchase financing has nosedived. For the most part, closing timeframes are also shortening now that lenders and law societies are almost all on board with e-ID verification and e-closings.

1 in 8: That’s how many mortgages are being deferred at big banks.

Prepare for more drama in real estate reporting

The “Great Reckoning”: News headlines like that may be just the beginning. If home prices widely fall in April like many expect, the drama will begin (we’ll get official month-over-month numbers from across the country in the first week of May). And, while hype is economically counterproductive and predicting a crash is premature, price declines may justify the concern. This all has much greater implications, of course. As Bloombergreports, “If [real estate] collapses, there’s not much that can pick up the slack.” “Not much” can be replaced with “nothing.”

Chinese Homebuyers go MIA in Vancouver: Guess why. The story

Mortgage Arbitrage: “While the government is spending a great deal of money funding initiatives like the Insured Mortgage Purchase program, it is buying triple A-rated securities at extremely elevated spreads and financing those purchases through the issuance of risk-free government debt at materially lower yields. As a result, the government stands to earn significant net interest margin by providing this [mortgage] liquidity.”—First National

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

I submitted an application to HSBC back in March when they were offering Prime -1.11%, I got an email from the Mortgage Specialist saying I have been approved as April 8, that I just needed to wait for the final papers to sign, today I got a notice saying that their pricing team change the policy earlier this week April 13 and no longer honor the rates of when my application was approved I got this notice tonight April 16 and my mortgage renews next Friday April 24. I am in shock they are doing this just now. Is there any suggestion you could give me? Do I have options? Is this possible? You see why did they wait just 5 working days prior to my maturity date?

Just to correct that HSBC sent me the notice that they can no longer respect the rates offered as per the submission date. However, they change this policy on April 13 and I got an email on April 8 saying that I was approved ….

Hi Pilo, Did they say why they would no longer honour your rate?

If it was no fault of your own, I would escalate to the branch manager immediately. Proof of a submitted application and proof of approval at a given rate is usually enough to hold that rate, unless you couldn’t meet the conditions of the approval.

“There has been a sudden policy change from our Pricing team this week and they announced they won’t backdate the offer to the date you submitted the application (as we thought initially). Instead, they can only be backdated to the day we started the official pre-approval application on March 27th. So the Prime – 1.11% won’t be eligible anymore for this application. Instead, the rates are per below:“

I have the screen shot of the date I applied, March 18, with the application number and the email from the Mortgage specialist on April 8 notifying that I was approved…. we already did the appraisal And they made me to open the bank accounts with them, we were waiting for the payout statement to sign the final documents !!!! I am still in shock I can’t believe this is happening !!!

Do you foresee lenders removing the “risk premium” for lack of a better term which from my understanding is 1 of the major reasons behind the higher spread we are seeing today between the bond yields and the current fixed rates?

Or do you foresee even with bond yields being as low as they are, that lenders will be reluctant to offer the lowest fixed rates given the economic climate/job market we are experiencing?

Was there any takeaways from around or following the 2008 market crash where lenders added a premium to fixed rates and despite low bond yields, did not lower fixed rates as much as 1 would have expected? Thanks

Hi Gary, As credit spreads shrink in the mortgage funding market, lenders slowly pass that savings through to borrowers. But there’s so much going on right now. It’s not just bond market rates and credit spreads driving mortgage rates. Higher provisions for unemployment-driven credit losses, less favourable deposit margins, housing valuation risk and weak loan growth are all factors that will ensure banks don’t sacrifice margin by quickly slashing rates. But give it enough time and we’ll get back near “normal” (i.e., 5yr Canada bond yield + 150 bps). In 2008, it took 6-9 months from peak crisis to relative normality.

log in

log in

10 Comments

Dear Spy,

I submitted an application to HSBC back in March when they were offering Prime -1.11%, I got an email from the Mortgage Specialist saying I have been approved as April 8, that I just needed to wait for the final papers to sign, today I got a notice saying that their pricing team change the policy earlier this week April 13 and no longer honor the rates of when my application was approved I got this notice tonight April 16 and my mortgage renews next Friday April 24. I am in shock they are doing this just now. Is there any suggestion you could give me? Do I have options? Is this possible? You see why did they wait just 5 working days prior to my maturity date?

Dear Spy,

Just to correct that HSBC sent me the notice that they can no longer respect the rates offered as per the submission date. However, they change this policy on April 13 and I got an email on April 8 saying that I was approved ….

Hi Pilo, Did they say why they would no longer honour your rate?

If it was no fault of your own, I would escalate to the branch manager immediately. Proof of a submitted application and proof of approval at a given rate is usually enough to hold that rate, unless you couldn’t meet the conditions of the approval.

Please let me know how it works out.

This was the notice I got:

“There has been a sudden policy change from our Pricing team this week and they announced they won’t backdate the offer to the date you submitted the application (as we thought initially). Instead, they can only be backdated to the day we started the official pre-approval application on March 27th. So the Prime – 1.11% won’t be eligible anymore for this application. Instead, the rates are per below:“

Dear Spy,

I have the screen shot of the date I applied, March 18, with the application number and the email from the Mortgage specialist on April 8 notifying that I was approved…. we already did the appraisal And they made me to open the bank accounts with them, we were waiting for the payout statement to sign the final documents !!!! I am still in shock I can’t believe this is happening !!!

Pilo, Drop me a line at [email protected]

Hi Mr Spy,

Do you foresee lenders removing the “risk premium” for lack of a better term which from my understanding is 1 of the major reasons behind the higher spread we are seeing today between the bond yields and the current fixed rates?

Or do you foresee even with bond yields being as low as they are, that lenders will be reluctant to offer the lowest fixed rates given the economic climate/job market we are experiencing?

Was there any takeaways from around or following the 2008 market crash where lenders added a premium to fixed rates and despite low bond yields, did not lower fixed rates as much as 1 would have expected? Thanks

Hi Gary, As credit spreads shrink in the mortgage funding market, lenders slowly pass that savings through to borrowers. But there’s so much going on right now. It’s not just bond market rates and credit spreads driving mortgage rates. Higher provisions for unemployment-driven credit losses, less favourable deposit margins, housing valuation risk and weak loan growth are all factors that will ensure banks don’t sacrifice margin by quickly slashing rates. But give it enough time and we’ll get back near “normal” (i.e., 5yr Canada bond yield + 150 bps). In 2008, it took 6-9 months from peak crisis to relative normality.

Check HSBC website. If it still shows 120days rate lock, then you should get it. Use it as an evidence when you communicate with them

Dear Spy,

I sent you an email as per your post above!

Thanks for your support !