log in

log inDebt ratios are rising, but it’s not just because borrowers are taking on more debt.

They’re rising because the government changed the rules of the game. Last October it made all insured mortgage borrowers prove they can afford a payment at the 5-year posted rate (currently 4.64%). Those artificially higher payments (coined the “stress test”) have increased people’s debt ratios, at least on paper.

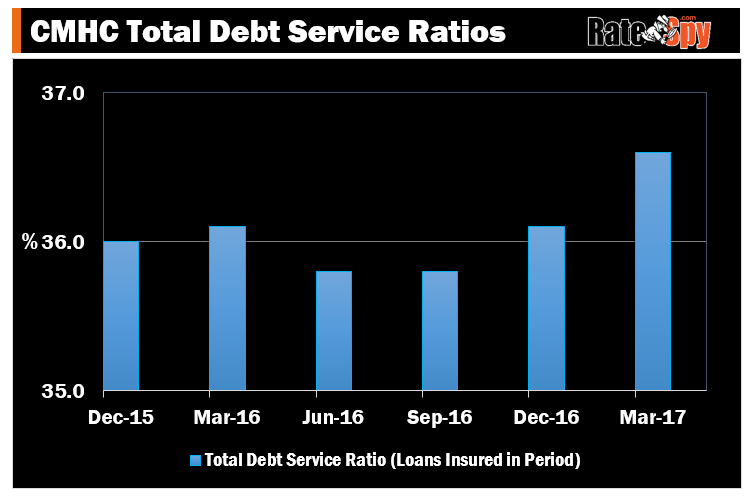

Numbers from Canada Mortgage and Housing Corporation (CMHC) are now bearing that out.

Average total debt service (TDS) ratio jumped half a percent from Q1 2016 to Q1 2017. Given this number hasn’t changed much for ages, “a variation of 0.5% points (or more) is…considered important,” says CMHC spokesperson Audrey-Anne Coulomb.

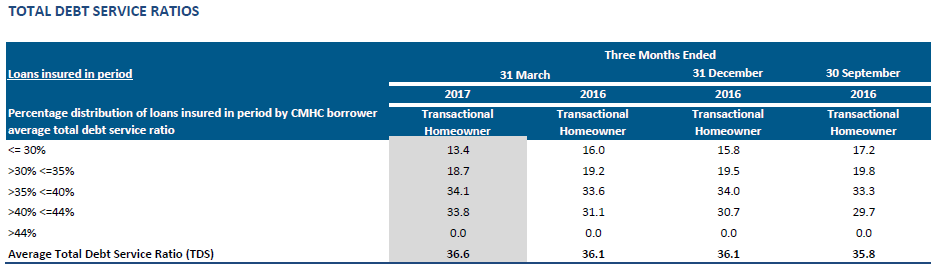

But more than that, there were big shifts in the distribution of debt ratios. For example, in Q1 2016, 16% of new CMHC-insured borrowers had a TDS ratio of 30% or less. Fast forward 12 months and that distribution is down to 13%, a material 2.6 percentage point decline.

At the same time, the percentage of people in the highest debt ratio bracket (i.e., those with a 40.1-44% TDS) jumped from 31.1% to 33.8% (a big 2.7 percentage point bump).

What this means, in part, is that it’s getting harder to qualify for an insured mortgage.

At least 1 in 5 new borrowers can no longer pass the aforementioned stress test, based on their desired purchase price and property characteristics. (This is our best guess based on government estimates, as no one tracks the number of willing homebuyers who can’t meet CMHC’s 44% TDS limit.)

So if you’re making less than a 20% down payment, keep all of this in mind. Some of you out there will have to buy a cheaper property than you thought, defer your purchase, scrape together a bigger down payment and/or find a co-signor.

2 Comments

CMHC’s just released consumer survey is interesting. 19% of buyers said the new rules impacted their decision, 11% raised their down payment (presumably to avoid mortgage insurance), 6% bought a cheaper place and 5% moved somewhere else than originally planned. So most are aren’t lowering their expectations, they are just avoiding the new rules or moving farther out to get the house they want.

Here is what that report says in whole:

• Fifty-three percent of buyers were aware of the latest mortgage qualification changes, and 19% noted that it impacted their purchase decision. For example, 11% of buyers said they increased their down payment, 6% purchased a smaller home, 5% purchased in a different location, and 3% delayed their purchase.

Half of people weren’t aware of the rule changes, so obviously more people were affected but didn’t know it.

Of the people who knew about it, 14% downgraded the property they were buying or didn’t buy at all.

I think it’s important to note that all of us can live in a mobile home or commute 2 hours each way and not be affected by CMHC’s rule changes. But is that what we want?