log in

log in After five months of buildup, the government’s controversial First-Time Home Buyer Incentive is now live. Kind of.

After five months of buildup, the government’s controversial First-Time Home Buyer Incentive is now live. Kind of.

Applications for the program, which lowers borrowers’ interest and default insurance costs (using taxpayer dollars that may or may not be recouped), are supposed to be available here. But the forms aren’t on the government’s website yet, despite the September 2 launch date.

In any event, if you haven’t heard, here’s how the program works and here’s my prior FTHBI review. CMHC has a dedicated information number if you have questions: 1-877-884-2642.

Now for the latest FTHBI bulletins…

- If you want to sign up, here’s the basic process:

- Apply (once they add the application to this website)

.- Your closing date must be after October 31, 2019

- Try this eligibility calculator first

- Give the completed form to your mortgage broker or lender

- Wait for approval

- “Approval for the FTHBI happens concurrently with mortgage loan insurance approval,” CMHC says. “We anticipate that the process, including timing, will be unchanged from what currently occurs with mortgage / mortgage loan insurance approval.”

- “The lender will receive the approval and confirm to the borrower that the Incentive is approved.”

- Notify your lawyer or notary that you’re using the FTHBI

- Don’t be surprised if your lawyer mutters something unsavoury under their breath about having to learn a new down payment process

- “The homebuyers’ lender will be providing instructions to the homebuyers’ lawyer/notary to ensure the incentive is funded.”

- “…Homebuyers are asked to contact 1.833.974.0963 to activate their FTHBI payment and provide the name of the lawyer/notary,” CMHC adds

- Before closing, the lawyer/notary requests incentive funds from the FTHBI administrator

- The administrator sends the incentive funds to your lawyer/notary and the mortgage is closed

- Apply (once they add the application to this website)

You may be wondering why we call it a subsidy. Well, that’s exactly what it will be for many buyers. It uses taxpayer revenue to subsidize borrowing costs of borrowers who could qualify without it. While it’s possible the government could recoup those funds overall, it’ll almost certainly lose money on people who sell before their home value appreciates enough. (CMHC needs your home to shoot up in value so its share of your equity is big enough to offset its costs).

You may be wondering why we call it a subsidy. Well, that’s exactly what it will be for many buyers. It uses taxpayer revenue to subsidize borrowing costs of borrowers who could qualify without it. While it’s possible the government could recoup those funds overall, it’ll almost certainly lose money on people who sell before their home value appreciates enough. (CMHC needs your home to shoot up in value so its share of your equity is big enough to offset its costs).- Our informal poll of lenders, including one lender that CMHC consulted with, leads us to believe the program is generally unpopular among lenders. It requires costly infrastructure and systems investments with no quantifiable benefit. There are clearly going to be lenders that don’t want to participate.

- CMHC says the program works in all markets, even expensive ones. “In the first quarter, 32% of units sold in Toronto and 20% in Vancouver were under $499,000,” it says. What it doesn’t highlight is that for $499,000 in Toronto/Vancouver you’ll get more square footage in a dollhouse. Moreover, you need to earn $118,500 with no other debt to qualify for a $499,000 home with 5% down and CMHC’s 5% incentive — i.e., not your typical first-time buyer income.

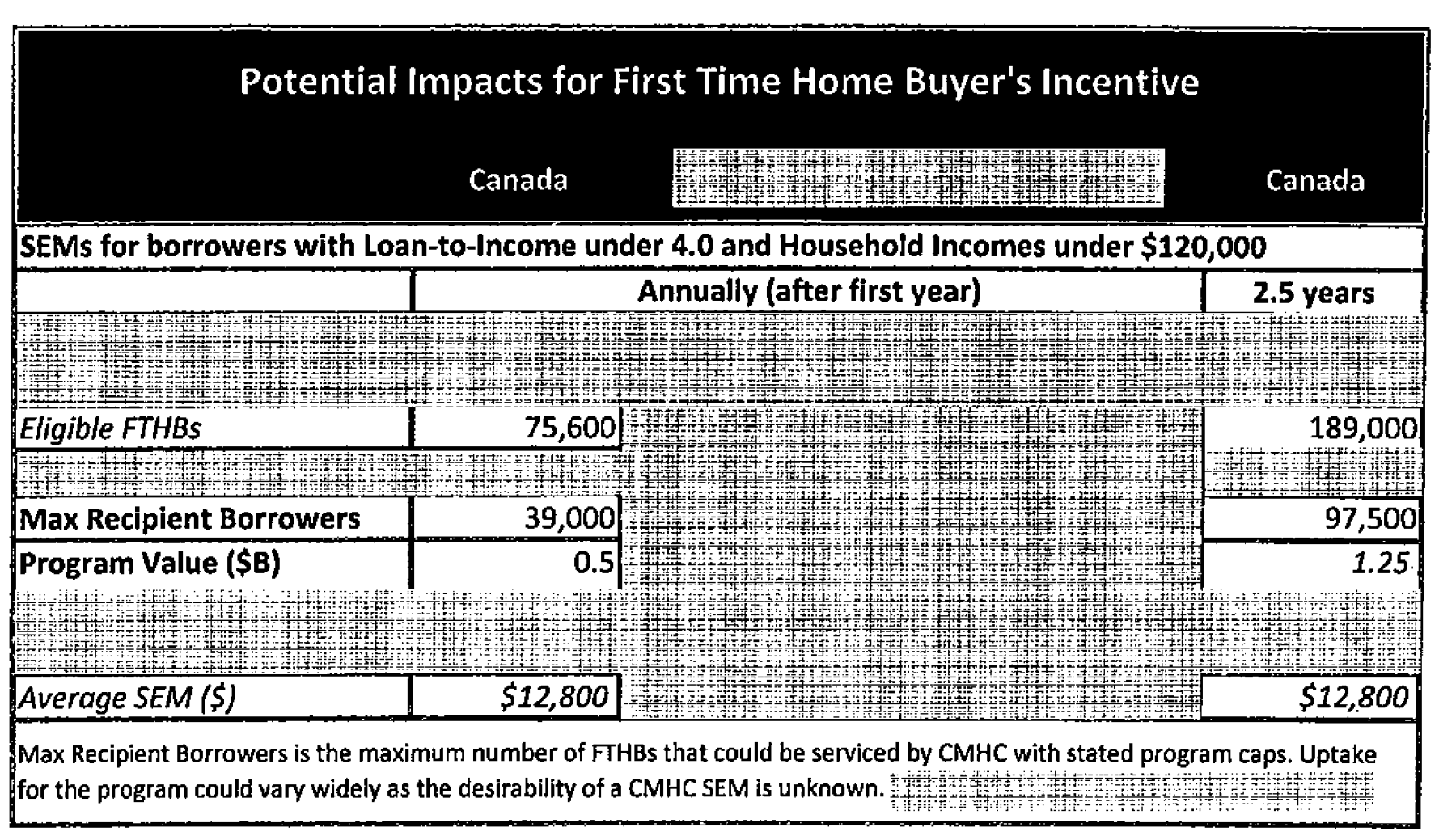

- According to this heavily redacted Finance Department document received from MP Tom Kmiec’s office, up to 97,500 borrowers will get an average of $12,800 in incentives (shared equity mortgages) through the first 2.5 years of the program. Kmiec’s Assistant, Kieran Moloney, claims they’ve been trying to get the government’s math on how it expects 100,000 borrowers to benefit from the program, but they’ve been rebuffed by the DoF and CMHC since April.

- If you’re a first-timer who’s interested in the FTHBI, get it while it’s hot. If the Liberals lose the election next month, there’s a very real chance the new government will can this program.

{kind=link}

7 Comments

I can’t see many lenders being happy with this program. It does nothing to drive more volume and requires expensive systems updates and new workflows. Speaking only for ourselves, we will not be promoting it. It’s a needless scheme and resources that went into developing it could have been much better spent elsewhere.

Update: The applications forms are now on the website here: https://www.placetocallhome.ca/fthbi/first-time-homebuyer-incentive#9

So based upon this calculator i can get 30,000

less house to save 750 dollars a year …

Most people qualify for less house with this “incentive” which is why most people won’t use it.

My nephew applied for the 10% incentive on a new build Minto townhome and looks to save almost $250 per month. makes perfect sense for him and saves him almost $3K per year.

Why the hell should my tax dollars go towards saving your nephew mortgage interest??

What a waste of resources. The administration cost of setting up this program will likely eat through most of its budget, and for what benefit? I can’t wait to see the figures on how many people actually end up falling for this scheme.