log in

log in“Lower for longer” has become the mantra in the rate market. But mantras don’t last forever.

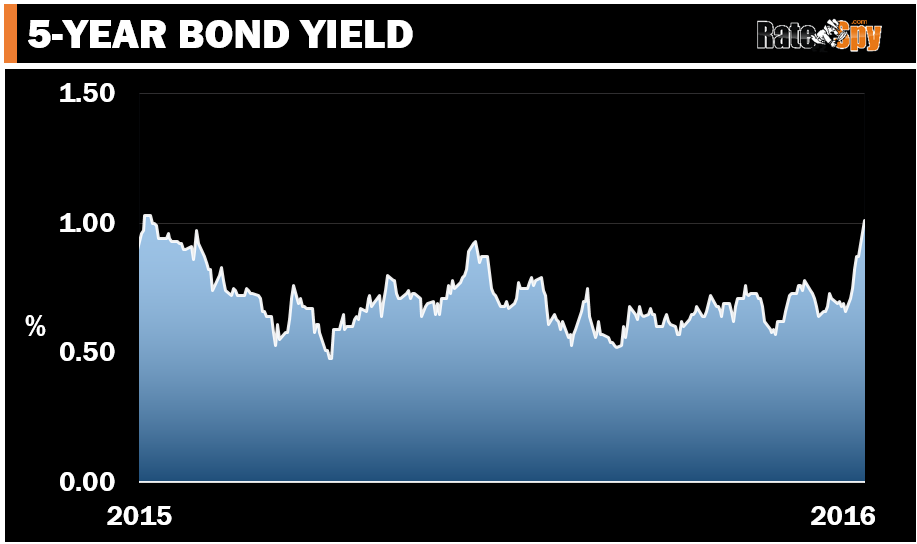

Trump is a rate market shock. He has single-handedly transformed how investors perceive North American growth prospects, inflation and default risk in the U.S. bond market. That’s driven Canada’s bellwether 5-year bond yield near one-year highs.

Combine this with Ottawa’s regulatory changes, and suddenly today’s record-low 5-year fixed rates look like a steal (more on that).

But if you want one, get em’ while they’re hot. Odds are this is no flash-in-the-pan spike in yields. Over the last week, Canada’s 5-year yield—which steers fixed mortgage rates—has surged the most since mid-2013. That’s when the U.S. Federal Reserve announced it would slow its U.S. bond buying (i.e., “taper” quantitative easing).

This “taper tantrum,” as it was coined at the time, caused our 5-year yield to rocket 70+ basis points in just three short months during the summer of 2013.

The start of this current move looks eerily similar.

What to Do

A few lenders have already announced higher 5-year fixed rates (up to 15+ bps), effective at midnight tonight. More will follow.

If you’re mortgage shopping and have:

- A big mortgage relative to your income

- A long remaining amortization (e.g., 15-20+ years)

- Aversion to risk

- A need to refinance and consolidate debt, and/or

- Less sound finances (e.g., a higher debt load or less stable employment)…

…you cannot go wrong with a deep discounted 5-year fixed rate, especially if you can find one near 2.14% or less. Variables and short-term rates simply don’t give you enough protection for the potential rate risk they now pose.

If you’re mortgage shopping and have:

- A small mortgage relative to your income

- A short remaining amortization

- Risk tolerance

- A short mortgage holding timeframe, and/or

- Strong finances…

…there’s still value in the 1-year fixed and 2-year fixed space. You’ll save at least 1/3 of a point up front versus a 5-year fixed and have more flexibility in the event rates drift back down.

If you already have a short term or variable-rate mortgage…

…do not lock in unless you know you can’t handle (the thought of, or the actuality of) a 10%+ hike in your monthly interest costs. Certain disinflationary supertrends like demographics, technology, high debt loads, etc., will absolutely limit how much rates can rise over the long-run.

Moreover, most lenders overcharge you when you convert from a variable to fixed. I just saw one bank quote 2.60% to a well-qualified client who wanted to lock in her variable. They might as well have reached into her bank account and stolen $5,000 (the extra interest she’ll pay versus typical 5-year rates).

Also keep in mind that Trump’s U.S. stimulus won’t benefit Canada near-term. So if the Bank of Canada did take variable rates higher, it likely wouldn’t happen for several months, if not quarters.

And then there are the wild cards. Unforeseen trade barriers, a global crisis (and no, not nuclear war, you anti-Trumpians) or plunging oil prices could be deflationary for Canada, and for Canadian rates. But these are potential catalysts whereas Trump’s economic growth is a known catalyst. That’s why now is not the time to gamble on variable or short-term rates…for most new mortgagors.

7 Comments

So I’m wondering how long this “Trump effect” will dominate markets before hard data returns to the driver’s seat? Sure, his campaign promises point to greater economic growth in America’s future. But what if it doesn’t manifest? Could we expect rates to come back down if the data doesn’t support the expectations attached to Trump’s win?

Timely question, thanks William. Canada could easily get an economic reality check before Trump’s stimulus kicks in. For one thing, his major election promises still need to be OK’d by congress. By the time things like U.S. tax cuts, infrastructure spending and deregulation start generating more jobs and discretionary income (indirectly) for Canadians, we could be talking late 2017 and beyond. Incidentally, the Bank of Canada projects our economy will be back to full capacity by mid-2018 — and that was B.T. (before Trump).

In the meantime, it’s going to be an emotional rollercoaster rate market. As always, bond traders are the best interpreters of economic events. So keep an eye on Canada’s 5-year bond yield: http://bigcharts.marketwatch.com/quickchart/quickchart.asp?symb=TMBMKCA-05Y&insttype=&freq=&show= . New record-low mortgage rates are probably out of the question unless it slides all the way back below 0.50%. And that’s a longggg way back given all the panic selling that’s occurred in the bond market this month.

Our mortgage is 5yr variable started July 2015. So just under 3.5yrs left on the mortgage. Should we lock in?!

How much could they rise and how quickly? Is this something that goes up a full percent overnight? Would another bank pay my penalty fee to break a mortgage if I wanted to switch to another bank that was offering me a better fixed rate?

Hi there TFB, We’re posting a story on these points tomorrow so I’ll link to it here.

Cheers…

Thank you I just saw this message and the story.

I guess what you’re saying is it’s a higher risk gamble these days and better to try switching to fixed ASAP 😉

Thank you for all the info you have provided!

Fixed rate fear mongering …yet again…game is to scare retail mortgage debtors…into a fixed rate…so on their end they can quantify risk matched assets,,,,rise and repeat…..in this slow growth environment…they can not raise rates..it would collapse the system…in 2010 they tried this BS…rates have only fallen from then LOL

It’s not about rate predictions. Nobody is fortune teller here. It’s about risk management.

Locking in is a waste for a lot of people, but not because we think rates will stay low. Trump’s trillion-plus stimulus package could easily be inflationary for Canada, we just don’t know how much. So if you’re risk averse and/or not as financially secure, why not be conservative with term selection — especially since fixed-variable spreads are skimpy.