Despite record-low short-term interest rates, most banks are offering junk 1-, 2- and 3-year rates on uninsured mortgages through the broker channel.

We’re seeing 5-year variable pricing as low as 1.45% or less at major banks. Yet, on a one-year fixed, for example, they quote mortgage brokers over 2.40%. That’s well above the discretionary rates bank customers are reporting to us. Those preferential rates are being made available via banks’ proprietary sales forces. (Keep in mind, we’re talking about non-default-insured rates here. More on insured rates below.)

Banks obviously have a reason for wanting to lock in broker clients to longer terms.

One reason is to avoid churn when these mortgages mature. In other words, they’re worried brokers will originate the loan, collect their finders’ fee and take the client elsewhere at maturity. A lower probability of renewal revenue makes shorter terms less appealing to banks.

A related reason is the compensation banks must pay brokers to originate such loans. Shorter terms leave less time for banks to amortize those commissions.

The moral of the story: if you want a 1- to 3-year fixed deal on an uninsured mortgage, don’t go looking to brokers. But if you need a short term on a high-ratio or insurable owner-occupied mortgage, brokers virtually cannot be beat.

Fed: Rate Levels Tied to Vaccine

The path for North American mortgage rates rests largely on ““progress on vaccinations,” suggested Fed Chair Jerome Powell today. “There’s nothing more important to the economy now than getting vaccinated.”

Recovery remains more of a second-half 2021 story, he suggested, noting “The risks are in the near term, frankly.”

Inflation is a distant threat, he said, but when it finally comes time for the Fed to hike rates, it’ll telegraph its plans in advance. “Nobody will be surprised when the time comes,” Powell told reporters.

Lenders Edgy About Condo Risk

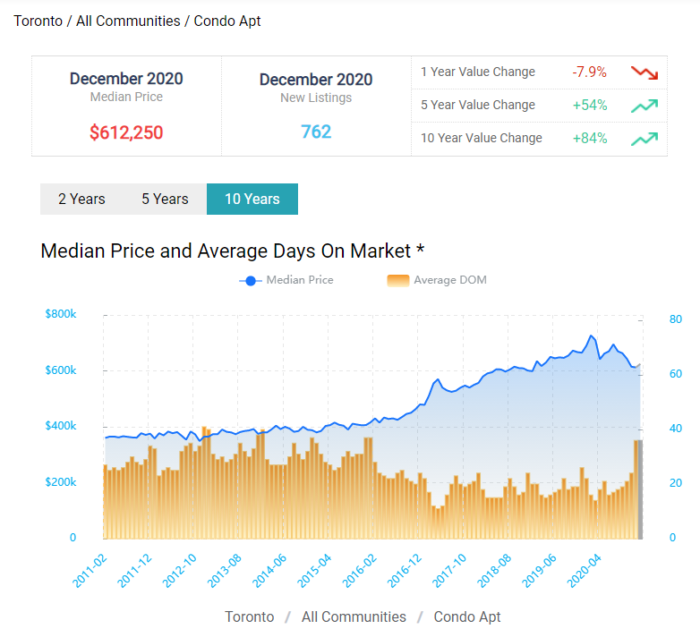

Condo inventories in some markets have surged with people exiting big cities and rents collapsing. We hear from lenders that they’re particularly nervous about areas like Toronto’s CityPlace and Liberty Village, where listings have exploded and rental investors (often deemed “weaker hands”) are plentiful. In many cases, it’s resulting in borrowers getting scaled-back loan amounts or declined altogether.

This chart below from HouseSigma shows a $100,000+ selloff in the average Toronto condo, from the top. That’s an equity loss in the tens of thousands for average condo owners who purchased in the last couple of years. Those who were leveraging their condo equity to buy more condos are especially feeling the heat.

That said, Toronto’s condo descent is slowing somewhat for now. Buy-the-dippers are taking advantage of the weakness ahead of an expected economic and immigration rebound this year.

This & That

Since the global financial crisis, average Canadian home prices have become 46% more expensive than U.S. home prices, estimates BMO (as of December 2020). It concludes that Canadians make a “choice” to spend more on housing than those in other countries. Report

“…In the past 12 months, mortgage debt growth has perked back up (+7.5% y/y, the fastest in more than nine years),” BMO says.

Whaddya know: If you don’t have a job you’re more likely to defer your mortgage payments. CMHC Report

“If you look at the number of mortgage deferrals that are left in the system, it’s a small fraction of what it was. No smoke, no [deferral] cliff…”—CIBC economist, Ben Tal via the Globe and Mail

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Branch-level discretionary rates can be even lower than the bank’s own (commissioned) mortgage reps. Last month TD mortgage specialists were quoting rates 5-10bps higher than discretionary rates in-branch.

My opinion on the condo situation is that people will still move to Toronto. There will still be demand, including over 400k immigrants in 2021. So while some move out of the city, some will still be moving in. My guess is that prices will probably hit the floor and then bounce later this year.

I currently have the option of paying a 3%, fixed) until the end of 2023 with the hope of a better rate. Any thoughts? A broker said he still thinks mortgage rate will still be <2% in late-2023.

Are you getting a non-prime mortgage? Is that why the rate is above 2%? What’s the term and lender?

As for 2023, it’s obscure. There’s no way to know what will happen. If you want to know what professional economists think, they’re expecting a 65+ basis point jump in rates (5-year bond yields) by 2023. Odds are, we’re “close” to the bottom in rates for this rate cycle, but rates could drag along that bottom for God knows how long.

Hey Scot, If things got really bad, you could theoretically see the overnight rate at -0.50% and the 5-year yield at -0.70%. Germany and other countries are already there. If current spreads persisted (and they probably wouldn’t) and banks lowered prime rate accordingly, one could theoretically see:

Prime Rate at 1.70%

Variable rates at roughly 0.35%

5yr Fixed rates of roughly 0.75%

My last message was mangled somehow so it did not make sense, but thank you for the answer! My question was that I have a current interest rate above 3% with two years remaining. I currently have the option of paying a penalty of about $700 for a 2.24% interest rate with my current lender or riding out my current mortgage until the end of 2023 with the hope of something better. A broker told me that he expects rates to still be low (below 2%) at the end of 2023 so it wouldn’t make sense to pay a penalty now and renew early for 2.24%. I just wanted to know if you had any thoughts. Do you think interest rates be on the upswing in 2023 or 2025? Thank you!

Regarding “A broker told me that he expects rates to still be low (below 2%) at the end of 2023”

I trust you laughed out loud at his delusion of prophecy. Do not factor in someone’s rate guesses. Instead, rely on what can be known: your 5-year plan, historical rate performance, your risk tolerance, mortgage rate comparisons, etc.

log in

log in

9 Comments

Branch-level discretionary rates can be even lower than the bank’s own (commissioned) mortgage reps. Last month TD mortgage specialists were quoting rates 5-10bps higher than discretionary rates in-branch.

Hey Ralph, That’s been known to happen, but it’s bank specific, often region-specific and it’s not the general industry norm in our experience.

My opinion on the condo situation is that people will still move to Toronto. There will still be demand, including over 400k immigrants in 2021. So while some move out of the city, some will still be moving in. My guess is that prices will probably hit the floor and then bounce later this year.

I currently have the option of paying a 3%, fixed) until the end of 2023 with the hope of a better rate. Any thoughts? A broker said he still thinks mortgage rate will still be <2% in late-2023.

Any thoughts on 2023, The Spy?

Hi “Any advice…”

Are you getting a non-prime mortgage? Is that why the rate is above 2%? What’s the term and lender?

As for 2023, it’s obscure. There’s no way to know what will happen. If you want to know what professional economists think, they’re expecting a 65+ basis point jump in rates (5-year bond yields) by 2023. Odds are, we’re “close” to the bottom in rates for this rate cycle, but rates could drag along that bottom for God knows how long.

Hey Spy! Based on the BOC rate and the 5 year bond yield, are there “theoretical lows” for 5-year uninsured fixed/variable rates?

Hey Scot, If things got really bad, you could theoretically see the overnight rate at -0.50% and the 5-year yield at -0.70%. Germany and other countries are already there. If current spreads persisted (and they probably wouldn’t) and banks lowered prime rate accordingly, one could theoretically see:

Prime Rate at 1.70%

Variable rates at roughly 0.35%

5yr Fixed rates of roughly 0.75%

My last message was mangled somehow so it did not make sense, but thank you for the answer! My question was that I have a current interest rate above 3% with two years remaining. I currently have the option of paying a penalty of about $700 for a 2.24% interest rate with my current lender or riding out my current mortgage until the end of 2023 with the hope of something better. A broker told me that he expects rates to still be low (below 2%) at the end of 2023 so it wouldn’t make sense to pay a penalty now and renew early for 2.24%. I just wanted to know if you had any thoughts. Do you think interest rates be on the upswing in 2023 or 2025? Thank you!

Any Advice…

Regarding “A broker told me that he expects rates to still be low (below 2%) at the end of 2023”

I trust you laughed out loud at his delusion of prophecy. Do not factor in someone’s rate guesses. Instead, rely on what can be known: your 5-year plan, historical rate performance, your risk tolerance, mortgage rate comparisons, etc.