log in

log inThe Feds would like you to think they want to help first-time buyers. The Liberals’ over-hyped and costly First-time Home Buyer Incentive is a case in point.

“The First-time Home Buyer Incentive makes it easier for you to buy a home,” they say.

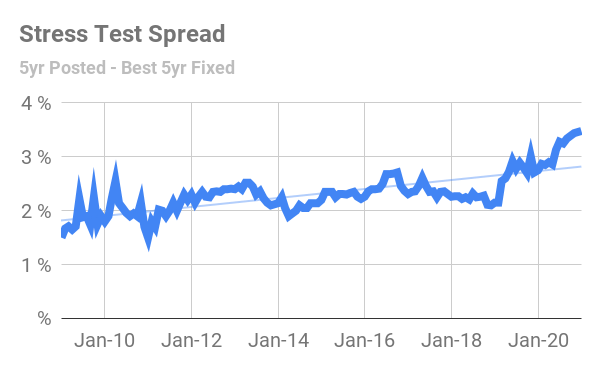

What the government omits to mention is that it’s stood by and allowed the mortgage qualifying rate (“stress test”) to become scandalously burdensome. This chart below says it all.

If you’re a hopeful first-time homebuyer getting a default-insured mortgage (i.e., you have less than a 20% down payment), Department of Finance officials are now forcing you to prove you can afford a rate that’s a whopping 348 basis points above the lowest 5-year fixed rate on the market.

That is a record.

In other words, the government’s mortgage stress test has never been tougher relative to true mortgage rates that people actually pay.

That means not only are home prices running away from you, but Ottawa’s bureaucrats, whose salaries are paid by your taxes, are essentially saying, “Too bad, so sad. Even though your chances of default are less than 1 in 200 statistically, we’ll let the stress test get harder and harder. If you don’t like it, rent! Forget about building equity and saving for your retirement through mortgage principal payments.”

Now, few (including this author) would advocate dramatically loosening credit amid: (A) an epic run-up in home values, and (B) amid supply mismanagement (at the federal and provincial levels) that’s resulted in too few homes and too much appreciation near major employment centers.

But it’s bloody-well time for a degree of reasonability from Ottawa. In no case should regulators impose a minimum stress test rate that is 3.7 times the actual rate first-time buyers pay.

That is entirely unnecessary. There is virtually no chance rates will soar 348 basis points in less than five years in addition to borrower incomes not increasing over that time span in addition to borrowers not being able to refinance or sell before default.

Heck, 5-year forward rates—one of the best indicators of where 5-year rates will be five years from now—are only projecting a 93-basis-point jump in rates by 2026 (source: Bloomberg).

If you’re a typical first-time buyer in a big city, the government seemingly doesn’t give a hoot about your mortgage qualifying woes. If it did, it would do something about its drastically over-inflated stress test rate, like the Liberals pledged to do in December 2019….before abandoning those plans last March.

Opinion / editorial content solely reflects the views of the author.

8 Comments

Well said sir.

First time home buyers get shafted while people who won the housing lottery i.e the majority of home owners over the past decade can leverage their first home to purchase another. The cycle continues.

Thanks FormerUW

The paper pushers at DOF don’t want prices going up faster. They have this backwards view that people should now rent instead of buy. That is why all these policies have come out encouraging new rental supply. Unfortunately this stance ignores the truth, which is that most Canadians don’t want to rent. They want to buy. 94% want to buy: https://www.newswire.ca/news-releases/canadian-millennials-dream-of-being-homeowners-but-most-arent-planning-for-it-cibc-poll-680903401.html. Their stress test policy is just one more example of Finance officials solving the wrong problem.

Hi Duff, Lots of truth in there.

Does anyone still do second mortgages above 80% LTV?

Hi Ed, Yes, in certain major urban centres. Chat with a local broker for options.

Is there a list or web resource to find or engage with 2nd mortgage lenders ( excluding private) or financial institutions?

Thanks

Hi Abi, Unfortunately, I know of no such list available to the general public. It would be extremely helpful if such a list existed and was comprehensive and up to date.

Cheers…