log in

log inCanada’s debt situation appears to be getting better…if you just look at mortgages.

But something sinister lurks beneath the surface. And it’s made of plastic.

Indebtedness has been outgrowing incomes in this country, despite stringent new mortgage restrictions. Canadians now owe $1.78 in credit market debt for every dollar of household disposable income, just under the record high.

And we keep hearing that “Mortgages are the main contributor to the total debt burden,” as we did from CMHC yesterday.

But that messaging—which has flowed out of Ottawa regularly since it started clamping down on mortgages—betrays a faster emerging threat. It’s no longer just sky-high mortgage balances that we have to worry about.

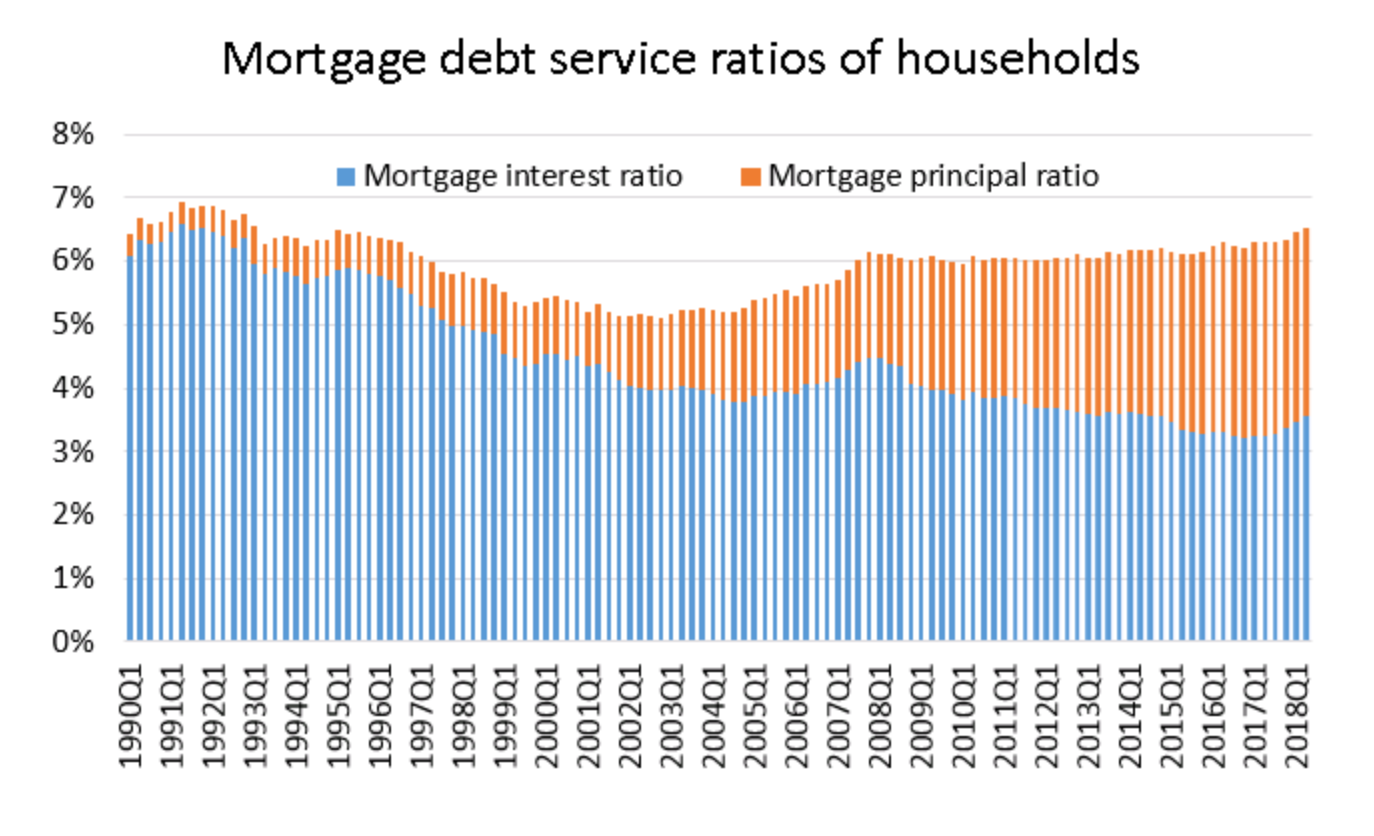

In fact, CMHC points out that the total cost of mortgage payments relative to total disposable income has been stable, fluctuating near 6% for the past 10 years.

But the composition of debt is changing.

The flow of new mortgages (as tracked by StatsCan) has slowed so much that it’s now being overtaken by the flow of credit card debt—for the first time in over 15 years!

And sure, mortgage debt is 2.5 times larger than consumer debt (including HELOCs), according to research firm Environics Analytics. But at the end of 2017, 48.6 cents out of every household dollar going towards interest expense went to consumer debt interest.

Barring a catastrophic crash, you can sell your house and erase your mortgage and HELOC debt. You can’t sell your credit card.

And lest we forget, three in four mortgages have fixed rates. Rates on credit cards and credit lines are riskier as they expose leveraged borrowers to climbing rates. That’s not to mention that credit card rates have hovered around 22% since 1995, according to the Bank of Canada.

Incidentally, CMHC points out that “A rise in the mortgage rate would impact about half of all mortgage loans within the first year following an increase.” (The bank of Canada pegs the number at 47%, which includes the 1 in 4 mortgages that renew every year plus floating-rate mortgages.) But rising rates wouldn’t impact half of all mortgage payments in the next year, since variable-rate mortgages have fixed payments.

Cracks Keep Forming in Family Balance Sheets

Cracks Keep Forming in Family Balance Sheets

They’re hairline cracks for the most part, but if you’ve driven down Toronto’s Gardiner Expressway, you know how big hairline cracks can get.

With all the incessant talk about mortgage debt, policy-makers may be taking their eyes off the non-mortgage debt ball.

Average credit scores are now dropping for the first time in several quarters. The decrease is modest so far and might be partly indicative of credit bureau reporting changes. But it also reflects higher credit utilization.

Most telling is the fact that credit card balances are suddenly growing more than double their pace from just one year ago.

In fact, “for the first time in seven years, the percentage limit used by credit card borrowers increased despite an increase to credit limits,” wrote National Bank Financial in a report today. “This suggests borrowers are increasingly using credit cards as a source of financing, in our view,” the bank concluded.

With growing credit loads, elevated interest rates and the end of the business cycle nearing, trimming overspending and interest expense are the keys to not living off Cheese Whiz in retirement.

Unfortunately, as CMHC states, “Highly indebted households have usually few debt consolidation options to respond to increasing debt service costs.” Ironically, it is recent mortgage policies—e.g., the stress test, eliminating insured refinances, etc.—that are directly responsible for depriving families of debt consolidation options.

Those refinance restrictions are now creating profound debt risk for a subset of the population who accumulate debt without being irresponsible (think debt from medical expenses, divorce, layoffs, death of a family member, failed business attempts and so on). By limiting restructuring options for people who would never miss a mortgage payment, no one wins—except maybe high-interest lenders (particularly credit card companies and private lenders). Canadians in need of help simply pay more interest, retire later, slow their consumption and add drag to the economy and employment.

And that’s not to say we should promote borrowers continually racking up debt and paying it off with home equity. We absolutely should not. But everyone deserves one chance to right their ship when it becomes awash with debt. Today’s federal refinance policies, positioned as the only viable solution by CMHC, OSFI and the Department of Finance, have drastically increased the cost of second chances.

Constraints on refinancing may discourage debt buildup among a small ratio of borrowers, but make no mistake, these very same policies will create new peril for banks, consumers and policymakers. As hundreds of thousands of homeowners resort to high-interest debt, their debt loads will become too heavy to carry. That could add rocket fuel for defaults and unemployment in future cyclical downturns. And if/when that happens, and unemployment spikes, those hairline cracks may become chasms.

7 Comments

How many 20% interest credit cards does it take to equal the profit of one mortgage. Roughly. Anyone know?

I agree with making sure people can afford their mortgage but here is what I don’t understand.

Let’s say you have a $300,000 mortgage and $50,000 in high interest debt. If the bank stress tests you and you don’t pass, you can’t refinance that debt at good rates. That means you have to pay much higher monthly payments which is more risky for everyone. So how is the bank better off by not granting the mortgage, assuming the homeowner can afford a mortgage at the 5 year fixed rate?

To me it seems like it’s safer for banks to let someone refinance into one low 5 year fixed payment and cancel all their other credit.

The pencil pushers in Ottawa think they can slow borrowing and lower risk by making refinancing harder or more expensive. Doing that is as futile as making marijuana illegal (again). People are still going to smoke up. They will just pay more to do it.

And after the refinance they go out and within two years have another $50K high interest debt – rinse, repeat. As they say, refinance is often a case of “extend to pretend”. At some point, homeowners have to change their perspective and expectations of an infinite amount of free money from a house that can only go up in value… So what is the public policy argument that you need government backed refinance???? Its available at a modest premium over purchase. So you want a government guarantee to support your bad habits, but don’t like the terms and conditions that come with it…

This is the second time I’ve read that everyone should have at least one opportunity to remove themselves from a bad debt situation by being able to refinance their homes. Actually the last person who commented said everyone should have the “right” to do this. Really? Borrowing to own a home isn’t a right. It’s a privilege. And why should a bank (or any other organization) be obligated to take on the risk to extricate these people from their situation (self inflicted or not)? Btw – every homeowner does have the opportunity to remove themselves from their debt burden. What better option is there than being able to sell the house and completely pay off their debts? A fresh start. These people should be happy there isn’t an imminent crash in the housing market like what happened in the US. Instead they claim they’re victimized by the very people that enabled their lifestyle to begin with. It never ceases to amaze how much people can rationalize their own poor decisions.

Yolo, This discussion centres on borrowers who “would never miss a mortgage payment.” The argument is simple. The sweeping removal of refinance options is a net negative, both economically and socially. (Said options had been available for years until recently, with excellent loan performance.)

The argument is not that lenders should be obligated to lend. The suggestion is that lenders should have the option to help low-risk borrowers one time with less prohibitive (but still safe) underwriting rules. Debt challenges are frequently not the result of bad decisions but even if they are, when people make mistakes—and everyone makes mistakes—it benefits all of us if they have a (one time) cost-efficient chance to recover. Selling a house is often sub-optimal for obvious reasons, including but not limited to transaction costs, tax implications, lost appreciation, the family impact, etc.

David, One does not pay a “modest premium” unless he/she meets rulemakers’ new more unforgiving refinance requirements. No one is arguing that the government take on materially more risk. The argument is the exact opposite, that overall risk could be reduced with more sensible refinance policy.

+1 Spy. What you said makes perfect sense which is why the Liberals will never do it. They would never admit their mistake in a million years. More important for them to appear that they know what they are doing than to do the right thing for Canadians.