Decade Discounts: With rates near perma-lows, according to some, people aren’t exactly lining up to lock in for 10 years. That’s especially true with penalties being so large on 10-year fixed terms, that is, until a mortgage passes its five-year anniversary—at which point the Interest Act limits penalties to three months’ interest. Nevertheless, effective rates on 10-year fixed mortgages just hit a record low today, according to RateSpy’s records. The cheapest 10-year is now just 2.84% through select brokers. The offer applies to all loan-to-values and all deal types (purchase, switch or refinances). The property must be owner-occupied and located in Ontario. Here are the best 10-year fixed rates we’re tracking at the moment.

Best-Case Scenario: If you’re in the mood for good news, Bank of Canada Governor Stephen Poloz delivered today. He said the best-case scenario for Canada’s economic recovery is still the “most likely scenario.” But he cautioned, “significant” monetary stimulus will be needed to rebuild jobs and spending. That’s essential to keep inflation near-target, given that deflation and high debt loads are the “two main ingredients of depressions…”

Don’t Tinker, Says NBC: “Now is not the time to tinker with mortgage rules,” write National Bank analysts. “Introducing more restrictive underwriting criteria at this time is likely to add further stress to a housing market that is experiencing a significant slowdown…It could exacerbate house price declines that negatively impact the broader economy through wealth effects, not to mention rising losses [for lenders and default insurers].”

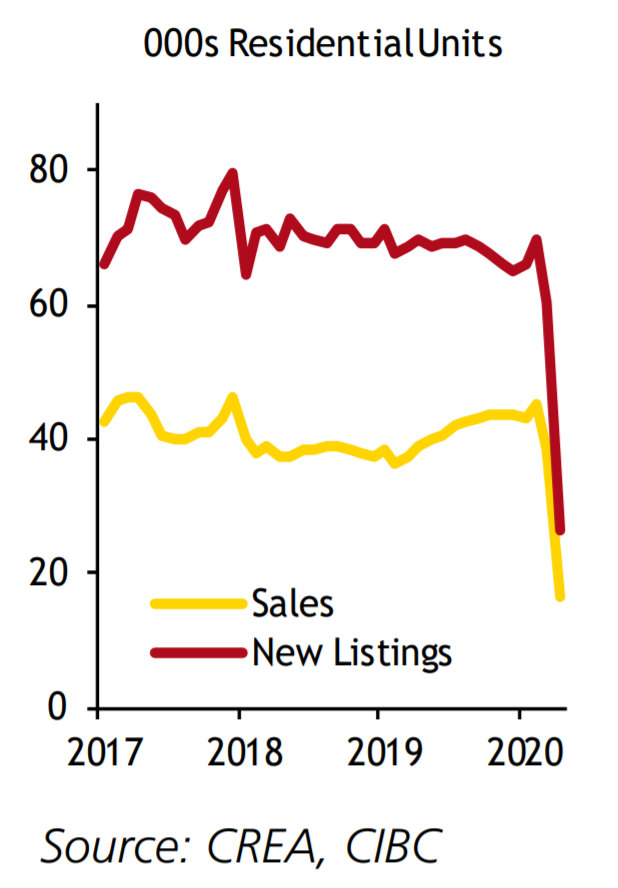

Mini-Rebound: Home sales picked up “notably” in the first half of May, says CIBC. That follows plummeting sales and listings in April, as the following chart from CIBC shows. The bank’s economists expect disproportionate demand for less expensive housing types in the weeks ahead. That “compositional effect” is pulling down average sale prices faster than normal.

Favourable Rate Resets: Tens of thousands of borrowers stand to save when their mortgage renews next. In the same report as above, CIBC Economics says, “…The weighted average mortgage rate currently paid by borrowers [is] roughly 50 basis points higher than the current rate…” It shared these other insights as well:

“…Lower-income borrowers are participating in [mortgage deferrals] at a higher rate…” (no surprise)

Landlords report a “better-than-expected” 9 out of 10 renters are paying their rent. (a surprise)

Only 18% of jobs lost since February were full-time “high paying” jobs.

Status Quo: RBC said today it sees no significant change in monetary policy near-term, once incoming Governor Tiff Macklem takes control of the Bank of Canada next week. Macklem’s first rate decision as BoC chief comes Wednesday, June 3.

Quotable: “It’s probably not going to be a quick, sharp V-shaped type of recovery that people were expecting initially.”—George Davis, RBC Capital Markets’ chief technical strategist (Financial Post)

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

What is Poloz’s “best case” scenario? That the economy bounces back next year to 80% or 90% of what it used to be? You don’t get high inflation when output is lower than it was when inflation was 2%. I don’t see inflation being a threat for years.

“The first, “best-case,” scenario assumed that containment measures would be lifted at least in part during May. This scenario would see a decline in the economy during the first quarter of 1–3 percent, and a further decline in the second quarter that would take the economy to around 15 percent below its level at the start of the year. The third quarter would then see a significant but partial rebound in the level of activity and then a gradual recovery back to trend over the next year or two. Very little structural damage was envisioned under this scenario.”

Hi Maggie, Check the site for rate. But first get proper advice on the right mortgage term for *you*, based on your finances, risk tolerance, five-year plan, etc.

Hi Waqas, Thanks for the report. There’s definitely room for negotiation there. RFA is a good lender so if you want to stay there and don’t need to make any mortgage changes, use the other offers on this site as leverage.

Hey Marc, Coming out of a recession, there’s a reasonable chance yields stay low for the next 18 months. They could rise a bit if/as the market prices in a recovery, but the odds of you renewing below 3% may be better than you think.

My mortgage isn’t due until 2022, at 3.24% by the time that is due it’ll probably be back up there again it would be nice if the banks offered lower interest rates to people who remortgaged a year ago

I refinanced in March on a 3 yr variable at prime – 0.95 which is now 1.5% with the option to lock in fixed anytime at current available rates if prime starts rising.

Hi !! I bought a new house in Feb 2020 and I have a variable interest rate of 1.85% with cibc right now. Should I fix my rate right now ? Please guide me

Hi! I got a 5 year variable mortgage back in September 2018 . With the rate drops currently it’s at 1.5% . Please advise if I should continue or change it to fixed ?

Thanks

Who did you get the variable 1.34% mortgage through a bank? I just finished talking to my Coast Capital Credit Union the best as of today with my 890 credit score through them ( 2.34 5 year fixed or 2.05 5 year variable) doesn’t seem that good when I look at some of the deals here but that being said a good friend of mine that use to work at RBC told me they would only give extremely good rates to the very odd person it was like a lottery seems to be true when you see some of these rates that people are posting here what is your opinion?

log in

log in

23 Comments

What is Poloz’s “best case” scenario? That the economy bounces back next year to 80% or 90% of what it used to be? You don’t get high inflation when output is lower than it was when inflation was 2%. I don’t see inflation being a threat for years.

Hi Dr-Munzato,

From Poloz on April 30:

“The first, “best-case,” scenario assumed that containment measures would be lifted at least in part during May. This scenario would see a decline in the economy during the first quarter of 1–3 percent, and a further decline in the second quarter that would take the economy to around 15 percent below its level at the start of the year. The third quarter would then see a significant but partial rebound in the level of activity and then a gradual recovery back to trend over the next year or two. Very little structural damage was envisioned under this scenario.”

Source: https://www.bankofcanada.ca/2020/04/teachable-moments-from-the-pandemic/

If the 10 year fixed rate drops another 0.5% it would be interesting.

Hey Mike, Agree, albeit if 10-year money drops a half point, five-year mortgages should improve at least 30-40 bps as well.

I have a mortgage with TD Bank that is due soon. What is the best rates and bank to explore.

Hi Maggie, Check the site for rate. But first get proper advice on the right mortgage term for *you*, based on your finances, risk tolerance, five-year plan, etc.

I’m with RFA bank in Canada my renewal is due they offered me prime – .20 or 2.59 fixed for 5 years

Hi Waqas, Thanks for the report. There’s definitely room for negotiation there. RFA is a good lender so if you want to stay there and don’t need to make any mortgage changes, use the other offers on this site as leverage.

I have a year and 6 months, until mine is due! Its at 3.24% on a 4 year term, im screwed, it will back to that by that time

Hey Marc, Coming out of a recession, there’s a reasonable chance yields stay low for the next 18 months. They could rise a bit if/as the market prices in a recovery, but the odds of you renewing below 3% may be better than you think.

My mortgage isn’t due until 2022, at 3.24% by the time that is due it’ll probably be back up there again it would be nice if the banks offered lower interest rates to people who remortgaged a year ago

Refinanced at 2.25% (variable, 5 years) with Merix.

Offered by CIBC 05/25: 2.49% 4yr fixed or 2.25% 5yr variable.

I refinanced in March on a 3 yr variable at prime – 0.95 which is now 1.5% with the option to lock in fixed anytime at current available rates if prime starts rising.

Well done, DH. 3yr variables are more flexible than 5yr variables. I wish there were more of them available at good rates.

Hi !! I bought a new house in Feb 2020 and I have a variable interest rate of 1.85% with cibc right now. Should I fix my rate right now ? Please guide me

Hi Prashant and Omar,

Are you asking us to predict future interest rates? 🙂

We’ll answer your question in today’s post.

Renewed 4 year fixed with CIBC @ 2.45% on May 19/2020…!

Hey Dal, If a 4yr fixed and big bank mortgage are the most suitable options for you, then 2.45% is certainly a decent rate for a no-hassle renewal.

Hi! I got a 5 year variable mortgage back in September 2018 . With the rate drops currently it’s at 1.5% . Please advise if I should continue or change it to fixed ?

Thanks

Hi Omar,

Personally I would stick with your variable.

I do not see the BOC raising interest rates anytime soon.

You have two more years to enjoy a low rate, I would only lock in if they were offering you a fixed rate at sub 2%.

But you need to evaluate your situation based upon your own situation.

I just locked in a 5 YR variable April 2020 for 1.34%, and I plan on riding this out for the full term (first time ever).

Though if a good fixed 5 year came up (sub 1.5%), I might be tempted to switch.

1.34% is obviously tremendous, Refi-Guy. Nice timing.

As for sub-1.5% 5yr fixed rates, that would require negative bond yields so let’s hope that doesn’t happen. 🙂

Who did you get the variable 1.34% mortgage through a bank? I just finished talking to my Coast Capital Credit Union the best as of today with my 890 credit score through them ( 2.34 5 year fixed or 2.05 5 year variable) doesn’t seem that good when I look at some of the deals here but that being said a good friend of mine that use to work at RBC told me they would only give extremely good rates to the very odd person it was like a lottery seems to be true when you see some of these rates that people are posting here what is your opinion?