log in

log inCanada has a mortgage rate transparency problem.

Too many lenders do not put their best cards on the table. To earn their best rate you have to dicker like you’re buying a rug at the bazaar.

These rate games make borrowing cost comparisons needlessly more difficult and inefficient. And that’s exactly what some lenders are aiming for.

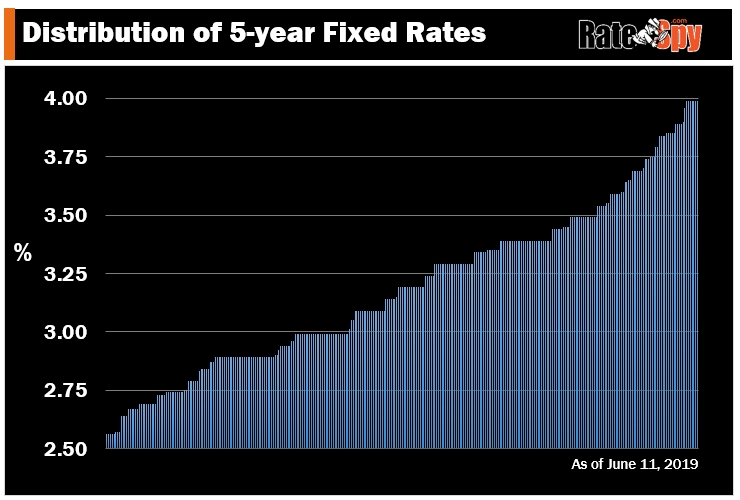

Take this chart, for example.

What this graph shows are all the advertised 5-year fixed mortgage rates that we track for prime borrowers who need purchase financing. For our purposes here, it displays rates up to 3.99% because few well-qualified borrowers pay rates above 4.00%.

The spread between the best and worst rates is a steep 1.43 percentage-points. Overpaying even half that much (i.e., paying 72 bps more) would cost someone $9,000 additional interest over five years on the average ($268,480) new mortgage.

Such wide rate dispersion never existed 20 years ago. Back in 1997, the gap between best and worst rates was only 1.05 percentage points, according to Cannex data.

Why Do Mortgage Rates Differ?

RateSpy currently tracks over 100 distinct interest rates for prime 5-year fixed purchase financing alone. (We monitor 300+ prime lenders but some of them price the same.)

Lenders advertise different rates on the very same type of mortgage for numerous reasons. Here are seven:

1) Most Lenders Like to “Go Fishing”

That is, they fish for uninformed consumers.

A recent poll by LowestRates suggests that roughly 3 out of 8 Canadians aren’t even aware that you can negotiate a bank’s mortgage rate. These are the customers many lenders crave most—that is, lenders that advertise above-average rates hoping to prey on ignorance.

Lenders also take advantage of loyalty. Someone once said: people change their spouse more than they change their bank. And banks know this. According to a RateHub survey, an incredible 4-in-10 still do business with their bank despite claiming their bank doesn’t have the best rates on any financial product.

2) Product Differences

To keep rates low, lenders often remove flexibility. In exchange for that rock-bottom deal, for example, they’ll often limit prepayment, porting or refinance options or impose bigger penalties for early termination. That’s why some of the lowest rates are called “low-frills” mortgages.

Other times a lender will lure people in with big cash rebates or free closing costs, in lieu of lower rates. Or they’ll be more flexible on the types of property or locations they lend on. That all has to be factored into mortgage pricing.

3) Funding Costs Differ

It usually costs lenders less to fund high-ratio insured mortgages than uninsured mortgages. The customer pays the insurance premium, risk of loss is lower and the capital costs are smaller.

Some lenders just have higher funding costs and/or operating expenses per loan to begin with. For example, a tiny credit union has to pay more for its funds than a giant multi-national bank, and has many fewer loans to spread its costs over.

And then there’s securitization (which refers to selling mortgages to investors). For a whole host of reasons that are beyond this story’s scope—like meeting investor targets or generating “replacement assets” in mortgage bonds—lenders are sometimes incentivized to offer lower rates for a short time.

4) Competition, or Lack Thereof

Smaller markets with less branch competition usually have higher rates. It’s why you’ll rarely get as good a rate in Tignish, PEI, as you will in downtown Toronto.

In general, the easier it is for a lender to hit its production targets (which vary based on its growth objectives), the higher its rates.

5) Relationship Pricing

Lenders want to make more money from  you than just your mortgage. So they mark up mortgage rates partly so they can “reward” you with “discounts” if you agree to buy other products.

you than just your mortgage. So they mark up mortgage rates partly so they can “reward” you with “discounts” if you agree to buy other products.

Incidentally, this is partly why CIBC got rid of its mortgage broker division. Brokers sold CIBC mortgages—under the bank’s “FirstLine” brand—at lower rates, but didn’t sell any other CIBC products. The bank didn’t like. It’s goal was to form greater “customer relationships.” (Read, create greater cross-sale.)

Relationship pricing is a dyed-in-the-wool business model of most credit unions. And no, this is not tied selling; it’s “preferential pricing” and it’s perfectly legal.

6) Risk Premiums

Every lender has a different risk-based pricing model. Companies each assess borrowers differently and therefore offer different rates to the very same borrower.

Many lenders more systematically target (slightly) higher-risk borrowers. They do so because the margins are better—given the rate premium for the slightly higher default risk. In other words, they might cater more often to folks with higher debt ratios, higher credit balances, lower credit scores, those who live in economically depressed regions, borrowers who can’t pass the federal stress test, etc.

For these lenders, it’s easier to quote a higher published rate and negotiate down if the borrower is well qualified, versus the other way around.

(It’s worth noting that we’re talking about prime lenders here, not subprime. The rates you see in the chart above are all from prime lenders.)

7) Intangible Premiums

Even Mortgage Professionals Canada acknowledges that “The interest rate is king in the mortgage space.” But many lenders still charge a premium for their supposed “service,” “convenience,” “advice” or the “trust” in their brand. They do it because many still pay more for these intangibles, and surveys back that up.

But the more that people realize they can get quality service, a fast & easy online interface and instant web-based advice without a big mark-up, the more old-school lenders will cede market share.

Who Loses the Most?

Product, risk and funding cost difference aside, the biggest losers (cost-wise) are the people who pay above-market rates without sufficient research.

Product, risk and funding cost difference aside, the biggest losers (cost-wise) are the people who pay above-market rates without sufficient research.

To be fair, however, some of these people value their time more than saving a few grand.

Either way, more than 2-in-5 Canadians get only one quote, according to Mortgage Professionals Canada. Those people are a gift to lenders, and one of the reasons most companies still don’t advertise their best rates.

Such lenders hope people take their inflated rates at face value, or worst case, consider them starting points for negotiation.

But that’s a problem if you’re in the minority. Reason being, according to a recent survey, 3 out of 8 people don’t know you can negotiate mortgage rates at a bank. That matches a prior survey that suggested 3 out of 8 people take the first rate they’re offered at renewal, the mortal sin of mortgages.

Research from south of the border found that consumers who obtain five rate offers saved “around 16.6 basis points on their rate…” On the average mortgage, that amounts to $2,095 +/- over five years, not an immaterial sum to most families.

The best part is, you don’t even have to pick up the phone or drive to a branch to see five offers. All you have to do is switch on your computer or smartphone and compare the lowest mortgage rates from your La-Z-Boy.

Rate Transparency is Coming

In the next five to ten years, Canada’s mortgage market will undergo a transformation. Most lenders who aren’t transparent will lose enough market share from prime (well-qualified) borrowers that they’ll be forced to advertise better rates online. People will no longer waste their time phoning a lender rep or driving to a branch to find the best deal.

In the next five to ten years, Canada’s mortgage market will undergo a transformation. Most lenders who aren’t transparent will lose enough market share from prime (well-qualified) borrowers that they’ll be forced to advertise better rates online. People will no longer waste their time phoning a lender rep or driving to a branch to find the best deal.

In fact, consumers have already spoken. LowestRates’ poll found that 53.7% of respondents say negotiating mortgage rates is “unfair.” An overwhelming 89.8% said that banks should transparently display the lowest mortgage rates without gimmicks.

Progressive lenders are listening to consumers’ cries. That includes the likes of Scotiabank (see its new low-rate eHOME mortgage), HSBC, motusbank, Tangerine and online discount mortgage brokers, to name just a few.

The rest have lots of catching up to do. And once they do, and once the vast majority use rate comparison tools, Canada’s rate market will be radically more efficient. That’s when Canadian families will finally enjoy the full fruits of mortgage competition, internet-style.

15 Comments

The variation in pricing is congruent with a more diverse (and arguably more competitive) market. There’s a similarly large variation in pricing for communication services like phone and internet.

If lenders offered fair and transparent mortgage pricing, they’d miss out on fat profits from clients that just sign the mortgage renewal letter at whatever rate the lender offers. It would also reduce many early termination penalties.

There’s also a less nefarious aspect to this. It’s well-known that lenders will adjust rates based things like shareholder sentiment on mortgage growth or their distribution of mortgage maturities. For example Scotia’s noncompetitive pricing for the past 18 months is likely an intentional way to moderate their residential mortgage growth. An now they want to grow again with great offers like the 4-year fixed rates you already wrote about. BMO seems to be opposite, with great rates last year, and mediocre rates this year.

Hey Ralph, There’s more competition than ever and lots more to come, thanks largely to the wonders that are Google, message boards, web-based news, social media and online rate shopping. But far too many borrowers still overpay needlessly, which is a key point of this story.

The discretionary pricing model you refer to is dying a slow death, as it should in a digital market. If lenders don’t offer fair and transparent mortgage pricing, they’ll miss out on profits from customers who refuse to play the “Can you talk to your manager to get me a rate exception” game.

P.S. Penalties at the largest lenders are based on posted rates minus the discount at origination. If big banks (who fund the majority of mortgages in this country) were more transparent on discounted rates, interest rate differentials would widen and they’d actually make more in penalty revenue, not less.

“Relationship pricing” is just another way of saying “I’ll give you a better mortgage rate if you buy overpriced accounts and investments.”

The only relationships people should have are with the most competitive providers of each individual financial product and that is never the same financial institution.

i just reduced my mortgage by 20 basis points through ratespy.com. the new scotiabank rate allowed me to go back to my lender and secure a better rate a few weeks before closing. banks and insitutions need to be more transparent as the article suggests with their lowest rates or prime borrowers will go elsewhere. thank god for ratespy!

Love these stories, Jon Paul. Many thanks for sharing and being a fellow spy!

Tangerine and HSBC both have discretionary levers to pull too. They are just more clever about it, and likely do it less frequently. I got a lower rate from both, than advertised on their sites.

Glad to see this dishonest pricing scheme being called out and it can’t end a day too soon. I dread my renewals because I know it involves haggling. At least we’re getting more transparency now thanks to you guys publishing all these rates. I used this info during my last renewal and got my lender down 15 bps on a 5yr variable.

Thanks Michael. Knowing the data helps people is what makes it fun. Nice work on your renewal!

I am with Scotia Bank and due for renewal. Have Recieved 3 calls from there reps re renewing. They offered a 2.7% rate. I informed them that my online offer on my account on Scotia’s web site is 2.37%. Answer from them we can’t match that.

Same bank?. So check your mortgage account renewal offer. Will always be better than phone offers

Hey Kerry, Thanks for sharing that anecdote. I have no good explanation as to why the same bank would offer you different rates. I have *a* explanation, but it’s not good, and it wouldn’t reflect well on the bank.

The moral is: renewal rates are always negotiable and like your tale suggests, automated online offers cost the bank less so they’re often priced more aggressively. This will increasingly be the case so it pays to check your bank’s app (assuming you’re satisfied with the other pros/cons of a big bank mortgage).

Just renewed with scotia app @2.30 fixed 3 years six months earlier. Rate dropped from 3.18%

I’m surprised they allowed me to renew earlier at a low rate! I’m not sure if 2.30% is the best available on a fixed three term but it’s good and the renewal on the app was smooth and no going to the bank. For scotia customers please download the app if your renewal is within six months. You might save some money renewing earlier

Hi A.D., If a 5-year fixed at a major bank is the best product for you, then 2.30% is quite fair for a renewal quote. That’s just 10 bps above Scotia’s excellent eHOME rates for new customers and just 16 bps above the lowest uninsured 5-year fixed rate in the country. Well done.

Explain how a 5 year,25 year mortgage works.Do you get a mortgage rate based on 25 years and pay it for 5 years and then refinance,renewal,or pay off the loan.

Hi James,

In Canada a 25-year mortgage generally refers to the amortization (the length of time your payments are spread over).

The most common term (length of mortgage contract) is only five years.

The most popular combination of term and amortization is a 5-year fixed mortgage with a 25-year amortization.

At the end of the five years, you can renew, pay it off in full or switch lenders.

You can refinance anytime unless it’s a “fully closed” mortgage. If you break a regular closed mortgage before maturity (e.g., before the five years is up) then you’ll pay a prepayment charge.