log in

log in In Canada, the cheapest mortgage rates are usually available on insured (or insurable) mortgages. But refinances cannot be insured thanks to rule changes in 2016.

In Canada, the cheapest mortgage rates are usually available on insured (or insurable) mortgages. But refinances cannot be insured thanks to rule changes in 2016.

That’s been a problem for folks with existing mortgages—particularly those who have “collateral charges.”

Collateral charges are mortgages that readvance or have a line of credit attached to them. Examples include the:

- RBC Homeline

- Scotiabank STEP

- TD FlexLine

- BMO Readiline

- CIBC Home Power Plan

- National Bank All-in-One

- HSBC Equity Power Mortgage

- MCAP Fusion

- Etc.

Until last year, if you wanted to change lenders with a collateral charge it usually required a refinance. That meant you couldn’t get super-low “insurable rates,” the best of which will save you about 1/4 point off your rate (i.e., ~$1,100 over five years per $100,000 of mortgage).

But there’s now a little trick that many outside of the mortgage business don’t know.

The HELOC Shuffle (a.k.a. “Collateral Transfer”)

If you’ve got a HELOC, one of the latest and greatest mortgage products these days is called the “Collateral charge transfer.”

We asked the country’s largest default insurer, CMHC, to explain it and here’s what they said:

“A borrower may initiate a switch of a prior uninsured home equity line of credit—combined with a mortgage loan—from one Approved Lender to another…”

CMHC adds, “…The switch transaction is eligible for CMHC insurance with the receiving lender provided that (the borrower qualifies, and…)

- the non-amortizing loan (i.e. HELOC) is converted to an amortizing loan at the time of switch

- there is no increase to the outstanding balance

- the amortization period does not exceed the lesser of the remaining amortization or 25 years

- the loan-to-value ratio does not exceed 80%

- the new charge is registered in first position.”

It Works for HELOCs in Second Position Too

If you have a mortgage plus a second separate HELOC secured against your property, you too can get a great insurable rate.

And CMHC confirms, you can switch over your mortgage (even if it’s presently uninsured) and keep your HELOC — so long as the HELOC “remains separate and distinct and ranks behind the CMHC-insured loan.”

In other words, if you default, the CMHC-insured mortgage must be paid out from proceeds first, and then the HELOC lender gets its money (if anything is left over).

Some Tips

Here’s the thing: Most lenders don’t support this right now.

If you’re in this boat, what you want to do is to ask the mortgage provider if they offer “collateral charge transfers.”

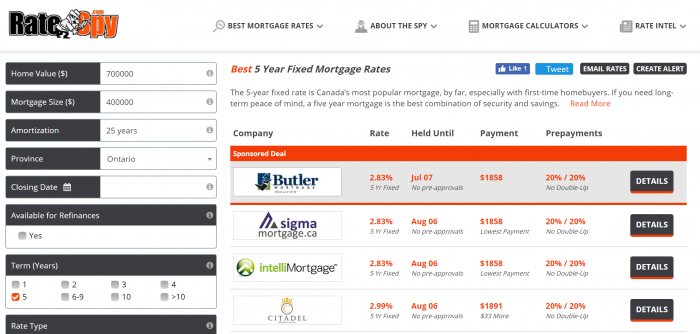

Some of the best rates on RateSpy do support collateral transfers, meaning that qualified borrowers with a collateral charge can currently fetch 5-year fixed rates below 3%:

In many cases, these brokers/lenders even pay some of your switching fees.

Mortgage brokers have been able to do this for a number of months now, but it’s not common knowledge on the street. (Hence this story!)

“We are doing those deals right now with several of our major lenders at rates below 3.00% on a 5 – year fixed, says Ron Butler of Butler Mortgage. “We cannot guarantee to do it every single time; it has to fit CMHC’s guidelines, but if it does fit it’s an unbeatable mortgage renewal offer.”

If you have a collateral charge and are coming up for renewal, hopefully this saves you some dough.

18 Comments

That sounds like you can have the effect of a refinance, since the HELOC gets added to the amortizing loan. The borrower could just max out their HELOC, do the switch, and then it’s rolled into the mortgage installment loan.

Yup.

So wouldn’t the home owner have to pay CMHC insurance all over again to get the lower rate?

Hi Eve,

With “insurable” mortgages, the lender pays the insurance premium.

Are there any lenders which are offering HELOC as a second charge if the CMHC insured first charge is from a different lender?

Try Simplii, Manulife or Tangerine.

I just got my secured line of credit through Simplii financial and my mortgage is with MCAP. Only cost $150 to set it up as well!

Cool. Thanks Vic and Tony.

Hello Tony,

What rate were you able to negotiate on the secured line of credit?

How did Simplii calculate the amount of the credit line?

Did it use 80% of current value vs outstanding mortgage balance or original mortgage vs. outstanding mortgage?

Thanks

Ray,

While I don’t know about Simplii, I think you’ll find lenders are not consistent and clear about the rules. Some lenders say you need 35% equity, and others say 20%. Some lenders even quote both rules depending on the product.

From what I understand of the OSFI rules, the available credit on the HELOC cannot exceed 65% of the property value. The total of a HELOC and a 1st mortgage cannot exceed 80%.

Hi Ray, Ralph. Unfortuntately, I was not able to negotiiate the rate. They offered me Prime (3.95%) +.50% which I think is fairly standard.

I honestly couldn’t tell you how Simplii calculated the amount of the credit line. They asked how much we were looking for and approved us for that amount in 2 days. I think Ray’s second point is how it should be calculated. Keep in mind that Simplii is in second position behind my mortgage through MCAP

Simplii has been quoting prime + 0.50% for a HELOC in second position, with a $150 set-up fee.

Not sure how many Canadians would want to roll over their HELOC into a regular mortgage via the collateral charge transfer. A lot actually use the principal portion to pay the interest on the HELOC so it doesn’t make a dent in their cash flow. So there’s that…

Mike. You don’t have to lose your HELOC. You can transfer it into a new mortgage plus HELOC. We do them for clients all the time.

I have a RBC Home line…and just pay interest…want to revert back to mortgage to increase equity…can I do this?

Tim

Absolutely. RBC Homelines of credit are fully open if you don’t have an RBC mortgage. You can lock into a fixed rate with RBC or pay the discharge fee and get your mortgage from any other lender.

If I have no other outstanding debt, and am able to contribute an extra $1,000 a month on top of a regular mortgage payment, am I better off with the Manulife One account or not? How can I figure this out – they;re site says I can pay it off in 14 years, but I want to be able to verify this independantly

I’m not aware of any independent calculators for the Manulife One. I’ve been looking myself for a long time.

I can’t comment on your case but here is how to look at it. Let’s say have two choices:

1) A regular $250,000 mortgage

or

2) A Manulife One with two parts:

$250,000 fixed mortgage

$50,000 line of credit account (LOCA)

The difference is that the Manulife One allows you to deposit income into the LOCA like a chequing account. If you deposit $5,000 of income for instance, you’re only charged interest on $20,000 of LOCA debt for as long as that income stays in the account. That is the advantage in a nutshell.

Unfortunately the LOCA rate is prime + 0.50% so the interest cancellation doesn’t make up for the higher rate in my experience.