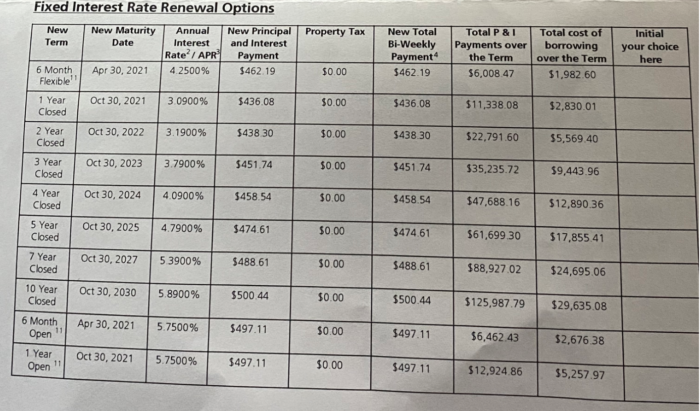

Check out these hideous renewal offers from a Big 6 bank. Yes, that’s right, banks are still quoting loyal customers non-discounted posted rates—the rates virtually nobody is supposed to pay.

This particular bank must really hate its customers. Fortunately, the borrower, who was extremely well-qualified, came to us for a second opinion. We told him to thank his bank for assuming he is too stupid or lazy to shop around.

He then got the bank’s retention team on the phone and read them RateSpy’s 300-basis-point lower rates. “Miraculously,” the bank relented on its wretched malodorous offers and quoted him a reasonable rate: 1.89% for a 5-year fixed.

The moral: Banks still send out these insulting renewal letters, hoping they’ll catch you napping, hoping you’ll be blind to the competition and hoping you’ll just initial in the convenient little box. Thankfully, RateSpy readers don’t step into these rudimentary traps.

A Use for Cash Back Mortgages

A few lenders (e.g., RMG Mortgages) are now offering five-year 3% cashback mortgages at record-low rates, and they’re proving quite popular.

The cash can be used for almost anything. One area where it’s particularly useful if a borrower needs to pay off debt to bring their total debt service (TDS) ratio down, so they can qualify for the mortgage.

Online brokers are selling these 3% cash back products for as low as 2.19% with a 5-year fixed term.

Note: 3% cash back is like getting a roughly 65-bps discount off a standard 5-year interest rate.

This 2.19% deal requires default insurance or 35%+ equity. The maximum purchase price is $999,999 and the minimum credit score is 680. Early termination results in a partial clawback of the cash. Federal rules prohibit cash back from being used for your down payment.

If true, and if the States gets another shot of fiscal aid, that would be bullish for U.S. and Canadian mortgage rates, OTBE.

“The country’s sales-to-new-listings ratio — a measure of market balance — is at its highest level in two decades, signalling demand vastly outweighing the supply of housing.” (via Financial Post)

Literally just got one of these “renew by default” packages in the mail. We had been aggressively paying down our mortgage on a 5yr variable and only have about $80k at renewal. Our current rate is 1.7%. they offered a 2.4% 2 yr fixed rate. I got them to renew at a 1.72% for 5yr, keeping my prepayment privilege so I can wrap it up whenever I want.

Frankly, the package they sent was embarrassing (to them): was a PC financial mortgage until it was recently rebranded.

Hey Laura, Thanks for sharing this tale in the forum. Glad you saw right through your bank. Lenders play these games because they know people are prone to renew with them, even when the lender’s ruse is revealed.

Spy, I’m in a 1.75% variable rate mortgage with HSBC that I signed a few months ago. I’m thinking about locking in at 1.84% for five years. My only concern is the prepayment penalty calculation.

I don’t really understand the IRD calculations. But it looks to me like it only gets atrocious when there’s a drop in the rates. With the rates being as low as they are, it seems like the risk of a large prepayment penalty is fairly small. Is my understanding correct?

Hi Jon, IRDs at big banks are often brutal (way more than 3-months interest), even if rates go sideways. You can test this theory with HSBC by running sample calculations. For example, you can assume you’ll break in 2 years and that rates stay where they are today.

@Jon, if you are on a variable rate, the IRD does not come into play. It should be 3 months simple interest. With respect to IRD being low for fixed rates, not true. HSBC will calculate what they can lend at (same remaining term) by reducing the posted rate by the discount they gave you. You will make up the difference as penalty.

@Aarvee, thanks for the response! My concern is that after locking into a fixed rate, if I need to break the mortgage, the penalty might be excessive (compared to the 3 months interest I’d pay if I had to break the variable).

If HSBC calculates the penalty by reducing their posted rate by the discount they gave me, and the posted rate has either stayed the same, or gone up, doesn’t that mean the penalty would be small?

prepayment amount x (annual interest rate – (Posted Rate – Discount Rate)) x days between prepayment and maturity / 365

So, assuming I locked in to 5 years at 1.84. With the posted rate at 4.74, that means my discount is 2.9.

SCENARIO #1

Let’s say I needed to break it a month later, and the posted rates hadn’t changed.

SCENARIO #3

Let’s say rates have gone down, and posted has decreased to 3.74

(annual interest rate – (Posted Rate – Discount Rate))

(1.84 – (3.74 – 2.9)) = 1 (Would have to spend 1% interest on remaining balance for the term, yuck)

SCENARIO #4

And I guess this is what I hadn’t considered. Even if the posted rate for a 5-year stays the same (or increases), as my term progresses, if I needed to break it, I would have to take the posted rate for the next longest term.

For example, if I have 1.5 years remaining on my term, I need to use their 2-year rate for the calculation (which is generally going to be much lower than the 5 year rate).

Using today’s numbers:

(1.84 – (3.19 – 2.9)) = 1.55

So, to sum up, for HSBC, there are two risks:

1. If their posted rates go down, you’re at risk of a large IRD penalty.

2. Depending on where you are in your term, they will use a shorter-term (i.e. lower) rate in the calculation. That’s partially offset by having a shorter term remaining for interest to apply to

Am I missing something? I feel like I might finally have a good grasp of this. Sorry for the huge post!

Here’s a sample hypothetical calculation for someone breaking one of their 5yr mortgages at today’s rates, assuming two years remaining and assuming rates hadn’t changed from three years ago.

= $100000*(0.0184-(0.0319-0.029))*730/365

= $3,100 penalty per $100,000 of balance

Thank you Ratespy! I have been following your site for 4 weeks. I was able to secure with your insight and my good relationship with BMO an awesome rate of 1.69 % for a 5yr fixed rate uninsured mortgage.

@Jon,

With rates being as low as they are, your 2nd summary point is the main risk. As you can see in HSBC’s posted rates, the rate keeps getting lower as your remaining term gets shorter. So the IRD can get huge.

Term Rate

1 year 2.49%

2 year 3.19%

3 year 3.59%

4 year 4.09%

5 year 4.74%

I am currently refinancing as well and going with HSBC but for a variable rate. For fixed rates its better to go to a lender with fair penalty policies… not the banks (Tangerine is a notable exception).

log in

log in

15 Comments

Literally just got one of these “renew by default” packages in the mail. We had been aggressively paying down our mortgage on a 5yr variable and only have about $80k at renewal. Our current rate is 1.7%. they offered a 2.4% 2 yr fixed rate. I got them to renew at a 1.72% for 5yr, keeping my prepayment privilege so I can wrap it up whenever I want.

Frankly, the package they sent was embarrassing (to them): was a PC financial mortgage until it was recently rebranded.

Hey Laura, Thanks for sharing this tale in the forum. Glad you saw right through your bank. Lenders play these games because they know people are prone to renew with them, even when the lender’s ruse is revealed.

I wonder what percentage of people are stupid enough to just sign back the renewal. It must be high enough to justify the banks doing it. Sad.

Hey Macro, Unfortunately, a meaningful minority.

Spy, I’m in a 1.75% variable rate mortgage with HSBC that I signed a few months ago. I’m thinking about locking in at 1.84% for five years. My only concern is the prepayment penalty calculation.

I don’t really understand the IRD calculations. But it looks to me like it only gets atrocious when there’s a drop in the rates. With the rates being as low as they are, it seems like the risk of a large prepayment penalty is fairly small. Is my understanding correct?

Hi Jon, IRDs at big banks are often brutal (way more than 3-months interest), even if rates go sideways. You can test this theory with HSBC by running sample calculations. For example, you can assume you’ll break in 2 years and that rates stay where they are today.

See its IRD formula here: https://www.hsbc.ca/mortgages/calculators/prepayment-details/

See its posted rates here: https://www.hsbc.ca/bank-with-us/todays-rates/#mortgage

Note: HSBC is not worse than most other big banks in this regard. But if you want lower penalty risk, you need to pick a fair penalty lender: https://www.ratespy.com/fair-penalty-lenders-which-lenders-have-the-lowest-mortgage-penalties-05109252

@Jon, if you are on a variable rate, the IRD does not come into play. It should be 3 months simple interest. With respect to IRD being low for fixed rates, not true. HSBC will calculate what they can lend at (same remaining term) by reducing the posted rate by the discount they gave you. You will make up the difference as penalty.

“by reducing the posted rate by the discount they gave you”

That’s where they get ya…

@Aarvee, thanks for the response! My concern is that after locking into a fixed rate, if I need to break the mortgage, the penalty might be excessive (compared to the 3 months interest I’d pay if I had to break the variable).

If HSBC calculates the penalty by reducing their posted rate by the discount they gave me, and the posted rate has either stayed the same, or gone up, doesn’t that mean the penalty would be small?

prepayment amount x (annual interest rate – (Posted Rate – Discount Rate)) x days between prepayment and maturity / 365

So, assuming I locked in to 5 years at 1.84. With the posted rate at 4.74, that means my discount is 2.9.

SCENARIO #1

Let’s say I needed to break it a month later, and the posted rates hadn’t changed.

(annual interest rate – (Posted Rate – Discount Rate))

(1.84 – (4.74 – 2.9)) = 0 (So, three months interest applies)

SCENARIO #2

Let’s say rates have gone up, and posted has increased to 5.74

(annual interest rate – (Posted Rate – Discount Rate))

(1.84 – (5.74 – 2.9)) = -1 (So, three months interest applies)

SCENARIO #3

Let’s say rates have gone down, and posted has decreased to 3.74

(annual interest rate – (Posted Rate – Discount Rate))

(1.84 – (3.74 – 2.9)) = 1 (Would have to spend 1% interest on remaining balance for the term, yuck)

SCENARIO #4

And I guess this is what I hadn’t considered. Even if the posted rate for a 5-year stays the same (or increases), as my term progresses, if I needed to break it, I would have to take the posted rate for the next longest term.

For example, if I have 1.5 years remaining on my term, I need to use their 2-year rate for the calculation (which is generally going to be much lower than the 5 year rate).

Using today’s numbers:

(1.84 – (3.19 – 2.9)) = 1.55

So, to sum up, for HSBC, there are two risks:

1. If their posted rates go down, you’re at risk of a large IRD penalty.

2. Depending on where you are in your term, they will use a shorter-term (i.e. lower) rate in the calculation. That’s partially offset by having a shorter term remaining for interest to apply to

Am I missing something? I feel like I might finally have a good grasp of this. Sorry for the huge post!

Hey Jon,

Here’s a sample hypothetical calculation for someone breaking one of their 5yr mortgages at today’s rates, assuming two years remaining and assuming rates hadn’t changed from three years ago.

= $100000*(0.0184-(0.0319-0.029))*730/365

= $3,100 penalty per $100,000 of balance

Thank you Ratespy! I have been following your site for 4 weeks. I was able to secure with your insight and my good relationship with BMO an awesome rate of 1.69 % for a 5yr fixed rate uninsured mortgage.

Thanks for sharing Robin! 1.69% is absolutely outstanding for a 5yr uninsured. Way to go!

@Jon,

With rates being as low as they are, your 2nd summary point is the main risk. As you can see in HSBC’s posted rates, the rate keeps getting lower as your remaining term gets shorter. So the IRD can get huge.

Term Rate

1 year 2.49%

2 year 3.19%

3 year 3.59%

4 year 4.09%

5 year 4.74%

I am currently refinancing as well and going with HSBC but for a variable rate. For fixed rates its better to go to a lender with fair penalty policies… not the banks (Tangerine is a notable exception).

Hey Aarvee, Generally agree. Tangerine has some of the most consumer-friendly mortgage features in the business.