Joe Biden has won the U.S. presidency, reports AP. Now rate-watchers will wait for the U.S. bond market to open Sunday at 6 p.m. ET to see the short-term rate impact.

Biden’s apparent win isn’t the main thing bond traders are concerned with. What matters more is whether the Republicans maintain control of the U.S. Senate. If they don’t, the fear is that Democrats might deficit-spend the country into oblivion and issue too much new debt (U.S. bonds)—both of which would be bullish for mortgage rates. And yes, Canadian mortgage rates too, given the economic linkage between our two countries.

The world will therefore be watching on January 5 when two key Senate races have a run-off. If the Republicans maintain the Senate, political gridlock will ensue and this U.S election fiasco may ultimately have only a modest effect on rates.

Near-term, few expect any extraordinary increase in bond yields. Indeed, with the Biden camp threatening to escort Trump out of the White House, and Trump vowing legal challenges, conflict-shy investors could buy bonds to ride out the storm. Through year-end, TD Bank has dim hopes of stimulus and projects a potential 20 bps drop in 10-year rates before Biden’s inauguration.

Of course, Canadian rates will also hinge on domestic inflation prospects. And those prospects are more bullish for our mortgage rates than U.S. factors, thanks partly to:

a higher degree of fiscal support on our side of the border

improved economic relations with the U.S. post-Trump

“On a GDP basis, the Canadian economy may recoup more ground than G-7 peers,” writes Bloomberg Economics. And most economists are calling for widespread vaccine availability by mid-next year. Hence, if yields drop near-term, there’s nothing to suggest the drop will be significant. That’s another way of saying, we may not be far from the bottom of this rate cycle.

Further out, rate hikes may be thwarted by persistently weak growth. Bloomberg Economics sees our annual GDP growing “in the 1.4%-1.5% range in the decade through 2030.” Growth below 2% is simply not consistent with a significant jump in mortgage rates.

Debt Advice from the Government

“Minimize your debt,” recommends the Financial Consumer Agency of Canada (FCAC). Seemingly good advice on the surface. But it doesn’t draw a distinction between good and bad debt. Clearly there is good debt or the Bank of Canada wouldn’t be cutting rates to incentivize borrowing. Good debt can be used to finance income-generating assets, for example.

We asked FCAC for its take on this. It replied, “Responsible borrowing can help consumers build a good credit history or improve their overall financial situation.” But, “it is important that regardless of the reason the consumer is borrowing [they consider]:

how much they will be able to repay each month

whether the monthly payments fit into their budget (try this tool)

will they still be able to afford the payments if their financial situation changes

what happens if they miss a payment.”

Even when borrowing to improve their lot, “Consumers may be more vulnerable if a larger share of their disposable income is applied to repaying their debt, leaving less flexibility in their monthly budget to cope with unforeseen events or a change in their circumstance, such as job loss or illness.”

“Consumers should shop around and compare their options before making a decision on which loan or credit product is right…,” FCAC adds. “Consumers should also read the terms and conditions of the credit or loan agreement carefully and take a close look at interest rates and fees.” No arguments there. See other FCAC borrowing tips here…

CMHC Yields Market Share to Sagen

The market share of private default insurer Sagen keeps rising. The company now pegs it in the “high” 30% range, 4-5 points more than last year.

Before CMHC stopped allowing higher debt service limits July 1, 2020, about 35% of Sagen’s transactional insurance was to borrowers with GDS ratios over 35% and/or TDS ratios over 42%. Now, thanks to CMHC’s abandonment of that market, 41% of Sagen’s volumes last quarter were in this segment.

Quick Hits

The latest word on quantitative easing (QE) is that the Bank of Canada will likely increase its weekly 5-year bond purchases by about $200 million, to $1.2 billion per week. Other things equal, that’s material enough to have a depressing effect on the 5-year yield, which in turn should keep 5-year fixed rates from running too high.

Mortgage growth is holding up near 5.7%, reports Bloomberg, thanks partly to lower rates driving more refinances.

“Condo supply is soaring in most major markets, especially in urban cores,” says RBC.

Thanks to record-low rates, monthly mortgage payments are lower today than one year ago, despite a sizable jump in average prices.

Canary in the coal mine? CIBC’s 31- to 60-day mortgage delinquencies have risen to 37 bps from 12 bps in July and 26 bps in August, reports Bloomberg.

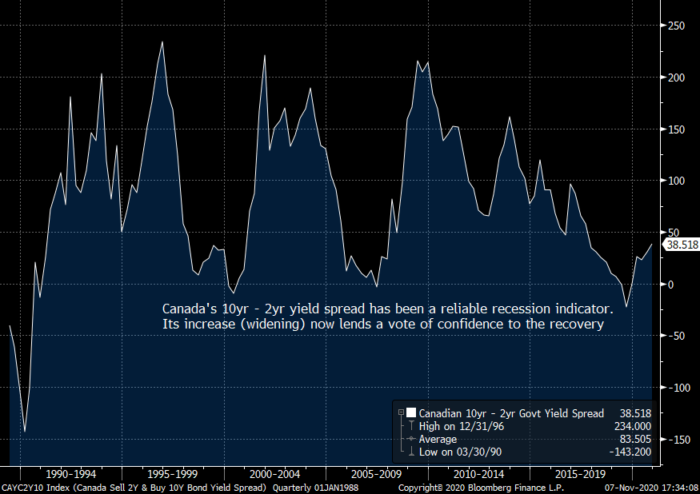

Last year’s negative yield curve predicted recession, as it usually does. Now, Canada’s curve has been steepening, reinforcing that we’re on the path to recovery. Higher rates two years out are now a materially higher probability than lower rates.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Evan Siddall’s rash decision to abandon 44% TDS will not result in any meaningful loss avoidance for CMHC. Nor will it do anything to prevent people from overleveraging. Every single 44% TDS borrower is already stress tested at ridiculously high rates. In other words, that 44% is actually 37% or so based on real life actual rates. 37% is well within reasonable risk thresholds.

CMHC will soon be the #2 insurer and the Canadian taxpayer owners of this crown corp will suffer as a result.

Hi pfmedium, We’d probably need to see 5-year bond yields close above 0.55% to 0.60% or so. Once that happens, some of the most competitive lenders will start lifting their rates.

log in

log in

4 Comments

Evan Siddall’s rash decision to abandon 44% TDS will not result in any meaningful loss avoidance for CMHC. Nor will it do anything to prevent people from overleveraging. Every single 44% TDS borrower is already stress tested at ridiculously high rates. In other words, that 44% is actually 37% or so based on real life actual rates. 37% is well within reasonable risk thresholds.

CMHC will soon be the #2 insurer and the Canadian taxpayer owners of this crown corp will suffer as a result.

Glad to see yields not up in the pre-market: https://www.cnbc.com/pre-markets/

Hoping I can refinance a bit more cheaply by month end.

Hi spy, how long do you think it could take before fixed rates rise on the vaccine announcement today?

Hi pfmedium, We’d probably need to see 5-year bond yields close above 0.55% to 0.60% or so. Once that happens, some of the most competitive lenders will start lifting their rates.