People hear the Bank of Canada predicting no rate increases until 2023 and take that as gospel. Maybe they shouldn’t.

The Bank of Canada’s key overnight rate—which more directly impacts floating-rate mortgages—doesn’t constrain fixed mortgage rates in the same way. The latter are driven more by what the bond market thinks the Bank of Canada (and the economy) will do in the future.

Bond yields continued their march higher on Monday, as:

This is not what inflation hawks want to hear. And there are untold said hawks dumping government bonds as we speak. (When selling pushes down bond prices, interest rates rise.)

A smattering of non-bank lenders have begun hiking fixed rates, including the biggest non-bank lender in Canada, First National. Others are threatening to hike rates imminently.

So far, we’re seeing announcements of 10-30 bps increases, depending on the lender and term. Expect further hikes given the 5-year Canada Mortgage Bond (CMB), which guides fixed rates at some of Canada’s most competitive insured/insurable lenders, closed near its high today after soaring 30 bps since February 1.

There’s still no sign of increases from the big guns (major banks), but if this yield climb persists, it’s just a matter of time.

Canada’s 5-year Bond Yield

New Mortgage Record

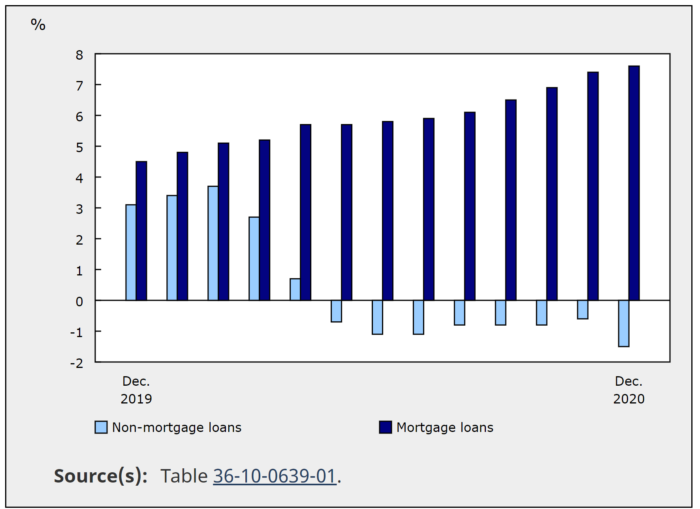

Real estate secured lending balances reached an all-time high in 2020, reports StatsCan. Mortgage debt and home equity lines of credit totalled $1,927.9 billion at the end of December, up 7.6% year-over-year. That’s on the back of 12.6% higher home sales.

Interestingly, non-mortgage debt declined 1.5% versus the prior year. That was thanks in part to government income subsidies.

5-year “breakeven rates” in the bond market suggest U.S. inflation could average 2.37% over the next five years, according to Bloomberg. That would be conspicuously above the Fed’s 2% target—which is noteworthy given the long-term correlation between U.S and Canadian inflation.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Inflation will be very high when the economy returns to normal. Because velocity of money will increase and M2 has already increased. Double – digit inflation is very likely.

Double digit inflation? We have been for year biting our nails about running out of ways to stimulate the economy by lowering rate further, but al of a sudden we have no room to tamp it down on the other side? Come on. As nflation rises, so will interest rates rise to control it. We had enormous room on that side of the scale. Double digit inflation is fearmongering.

The problem is that there is no room for interest rates to rise. If interest rates rise, the market will collapse. You can compare TNX and QQQ index in the last 5 days.

What does that mean, no room to rise? They’re already rising!

Are you saying rates can’t increase 1-2 percentage points? If so, you better check a historical rate chart. Saying the market will collapse if rates rise is empty speculation. Rates ran up big in 1994, 1999, 2005, 2009, 2013 and 2017 and the TSX and housing prices did not crash. Not sure where you are getting your data. On top of that, borrowers are stress tested today with 2-3 higher rates.

I’ll leave predictions to others but a collapse seems highly unlikely.

@JaReal

By market , I mean the stock market and my emphasize more on technology stocks that make sense to invest in if interest rates are low.

Another important point is that , since 2018 the continuous reduction of interest rates has subsidized investment on low return investments and stocks have become addicted to low interest rates .

I currently have 1.15% (Insured 5 yr variable rate) with 4.2 yrs remaining with $740K mortgage left. Should I continue or lock in for 5 yrs. fixed rate If I get close to 1.35% or even lower? I am not selling home for next 5 years.

1.15% is exceptional and for someone who’s well qualified (I don’t know your situ) it’s probably not worth breaking unless the possibility of 150+ bps higher rates would create too much risk for you.

Know that rate hikes are probable within a few years. So by floating your mortgage you’re making a calculated bet that BoC hikes will take longer than expected or be limited to 75-100 basis points. That’s not totally irrational.

P.S. People are now looking at 1.59% (+/- 10 basis points) for an insured 5yr fixed.

So I talked to my bank today, BMO and they quoted me 1.74% fixed for 5 years. When I mentioned HSBC’s rates they said they typically don’t compete with HSBC. Huh? Finding it hard to come up with reasons to stay with BMO, is this a typical response from major banks regarding HSBC?

Hey Scott, Banks always say rubbish like that. They tell people that they benchmark their pricing against “peers” because they think a Big bank mortgage is something special. It’s not. And banks who don’t compete should be left in the dust.

Now, that said, if your bank has a particular product you need (I like BMO’s Readiline and Cash Account when the rates are good, and 1.74% is decent for a readvanceable — assuming penalty risk is not a concern) then it may be an offer worth taking. If you needed a readvanceable, for example, I’d steer clear of HSBC’s Equity Power Mortgage because it doesn’t auto-readvance.

Scott, try contacting your RVP. Ask them to request a rate exception.

I helped a family member get 1.49% on a 4yr fixed with BMO for an early renewal at the end of January. And that was on a rental, not an owner-occupied residence. Documents were signed in early Feb. This was for their standard mortgage with 20/20 prepayment privs, not the low-frills “smart fixed”.

@JaReal

I challenge your historical view . I believe every situation is unique and we can use history to learn from it not copy from it . So you can check today stock market and compare with TNX rate increase and its impact on the market , the conclusion is so obvious .I think if the interest rate increase , we would not have hot market anymore.

Please see this clip https://www.youtube.com/watch?v=zH8Tg9nCzhc

To update, I tried to get to the regional VP to ask for a rate exception and instead a client relationship guy contacted me. Been with bank 4 months after being a high performance sports coach (soccer). So I am guessing my getting a good rate at BMO won’t happen.

log in

log in

16 Comments

Inflation will be very high when the economy returns to normal. Because velocity of money will increase and M2 has already increased. Double – digit inflation is very likely.

Double digit inflation? We have been for year biting our nails about running out of ways to stimulate the economy by lowering rate further, but al of a sudden we have no room to tamp it down on the other side? Come on. As nflation rises, so will interest rates rise to control it. We had enormous room on that side of the scale. Double digit inflation is fearmongering.

The problem is that there is no room for interest rates to rise. If interest rates rise, the market will collapse. You can compare TNX and QQQ index in the last 5 days.

Sina…….good, accurate and factual observation.

@Sina

What does that mean, no room to rise? They’re already rising!

Are you saying rates can’t increase 1-2 percentage points? If so, you better check a historical rate chart. Saying the market will collapse if rates rise is empty speculation. Rates ran up big in 1994, 1999, 2005, 2009, 2013 and 2017 and the TSX and housing prices did not crash. Not sure where you are getting your data. On top of that, borrowers are stress tested today with 2-3 higher rates.

I’ll leave predictions to others but a collapse seems highly unlikely.

@JaReal

By market , I mean the stock market and my emphasize more on technology stocks that make sense to invest in if interest rates are low.

Another important point is that , since 2018 the continuous reduction of interest rates has subsidized investment on low return investments and stocks have become addicted to low interest rates .

@Sina

I challenge your inverse rate-stock theory because history often doesn’t support it.

But even if the stock market falls how would that make a significant difference to the mortgage market?

Banks making billions and will continue.

However, end users will be squeezed…

Know your limit and stay within it.

Hi Spy,

I currently have 1.15% (Insured 5 yr variable rate) with 4.2 yrs remaining with $740K mortgage left. Should I continue or lock in for 5 yrs. fixed rate If I get close to 1.35% or even lower? I am not selling home for next 5 years.

Any Advice would be helpful.

Thank you.

Hi Tejas,

1.15% is exceptional and for someone who’s well qualified (I don’t know your situ) it’s probably not worth breaking unless the possibility of 150+ bps higher rates would create too much risk for you.

Know that rate hikes are probable within a few years. So by floating your mortgage you’re making a calculated bet that BoC hikes will take longer than expected or be limited to 75-100 basis points. That’s not totally irrational.

P.S. People are now looking at 1.59% (+/- 10 basis points) for an insured 5yr fixed.

So I talked to my bank today, BMO and they quoted me 1.74% fixed for 5 years. When I mentioned HSBC’s rates they said they typically don’t compete with HSBC. Huh? Finding it hard to come up with reasons to stay with BMO, is this a typical response from major banks regarding HSBC?

Hey Scott, Banks always say rubbish like that. They tell people that they benchmark their pricing against “peers” because they think a Big bank mortgage is something special. It’s not. And banks who don’t compete should be left in the dust.

Now, that said, if your bank has a particular product you need (I like BMO’s Readiline and Cash Account when the rates are good, and 1.74% is decent for a readvanceable — assuming penalty risk is not a concern) then it may be an offer worth taking. If you needed a readvanceable, for example, I’d steer clear of HSBC’s Equity Power Mortgage because it doesn’t auto-readvance.

Scott, try contacting your RVP. Ask them to request a rate exception.

I helped a family member get 1.49% on a 4yr fixed with BMO for an early renewal at the end of January. And that was on a rental, not an owner-occupied residence. Documents were signed in early Feb. This was for their standard mortgage with 20/20 prepayment privs, not the low-frills “smart fixed”.

@JaReal

I challenge your historical view . I believe every situation is unique and we can use history to learn from it not copy from it . So you can check today stock market and compare with TNX rate increase and its impact on the market , the conclusion is so obvious .I think if the interest rate increase , we would not have hot market anymore.

Please see this clip

https://www.youtube.com/watch?v=zH8Tg9nCzhc

My apologies, I am not sure what an RVP is? Also I am in NS but I don’t think that matters much in this case. Thanks.

To update, I tried to get to the regional VP to ask for a rate exception and instead a client relationship guy contacted me. Been with bank 4 months after being a high performance sports coach (soccer). So I am guessing my getting a good rate at BMO won’t happen.