CMHC on Payment Deferrals: “CMHC has provided increased flexibility to defer mortgage payments on its insured homeowner mortgage loans, which means lenders are now able to defer payments on a borrower’s CMHC-insured mortgage up to six months without CMHC’s approval. Borrowers should speak to their lenders directly by going through their default management department to confirm if they are eligible for this deferral and the terms and conditions for resuming their payments.”

Closed Houses: “Open houses are quickly becoming extinct,” notes Royal LePage CEO Phil Soper in this story.

3:23 p.m. Update

Potential Overreaction: Selection bias and other statistical errors are unnecessarily driving our economy to the brink, argues this Stanford professor. Once the market senses things aren’t as bad as advertised, we’ll see a rally like never before. Either way, standing in front of a herd of wildebeest is ill advised, even if you know they’re about to run off a cliff.

End Game: “We have to remember that this crisis has an end game, a vaccine.”—CIBC economist, Ben Tal

2:34 p.m. Update

Call Centre Pandemonium: Lenders are being overloaded with calls from borrowers trying to defer their mortgage payments. Wait times are hours in some cases. Some borrowers are even lying about losing their jobs, according to lenders. Hence, some deferral requests are being declined. Remember: mortgage payment deferral is largely at the lender’s discretion and each lender’s policies are somewhat different.

BoC Keeps Buying: The Bank of Canadabought another $305 million in Canada Mortgage Bonds today. That’s helping liquidity somewhat, which helps keep mortgage rates lower than they otherwise would be.

Hedging Issues: Bond market volatility is making rate hedging so expensive, one commercial lender today said it’s now limiting commercial mortgage rate holds to 30 days.

1:21 p.m. Update

Cataclysmic GDP: JP Morgan estimates the U.S. economy (i.e., GDP) will shrink a shocking 14% in the second quarter. Even if JPM is off by a few points, that is depression-era magnitude. Canada depends on the U.S. for much of its GDP and we’re already reeling from oil patch devastation. Canadian homebuyers still partaking in bidding wars need a head check. GDP will bounce huge once people get back to work, but residual damage to the economy will be severe and housing won’t be unscathed.

Spread Check: The gap between the best 5-year fixed and variable rates is fluctuating wildly as rates change. As we speak, it’s over half a point. In other words, you’ll pay a 50-basis-point premium for a 5-year fixed rate today. That boosts the upfront rate advantage of variables—particularly given we’re heading into a recession, one in which prime rate should fall further. But as more lenders slash their variable rates, this advantage could evaporate quickly.

11:58 a.m. Update

Rate Changes Galore: Rates are changing at a frenetic pace. Some highlights: ⚬ HSBC now has the lowest rate in the country: a 3-year fixed (default-insured only) at 1.88% ⚬ Investors Group and HSBC have the lowest widely available uninsured 5-year fixed rates at 2.49% ⚬ HSBC has the lowest widely available insured 5-year fixed rates at 2.29%, but brokers are much lower. The latest 5-year fixed rates. ⚬ The lowest variable rates are available through brokers and still under 2%, but they’re changing rapidly. The latest variable rates.

Pay More: Don’t be penny-wise/pound foolish. If you’re taking a 5-year fixed rate, pay a slightly higher rate for mortgage flexibility (e.g., more favourable penalty policies, better porting and increased privileges, etc.). You may need it if you have to refinance or sell your home in the next five years.

Oil Rebounds: Oil (WTI crude) is/was on track for one of its best days ever. To the extent the price holds $20 (as of this writing we’re near $24), it could further support bond yields and fixed mortgage rates in the near term.

TD Boosts Variables: Canada’s second-biggest mortgage lender has raised the following advertised specials: ⚬ 3yr fixed: 2.69% to 2.89% ⚬ 5yr fixed (high ratio): 2.69% to 2.79% ⚬ 5yr variable: 2.85% to 2.95%.

9:47 a.m. Update

Day 54: It’s been 54 days since Canada’s first coronavirus case. In that timeframe: Canadian coronavirus cases have gone from 1 to 727 Prime rate is down from 3.95% to 2.95% The lowest 5-year fixed has dropped from 2.48% to 2.17% (insured) The lowest variable has dropped from 2.64% to 1.84%

Decimation: Stocks of mortgage companies have been cut in half: Home Capital: Down 54% from November high First National: Down 55% from November high

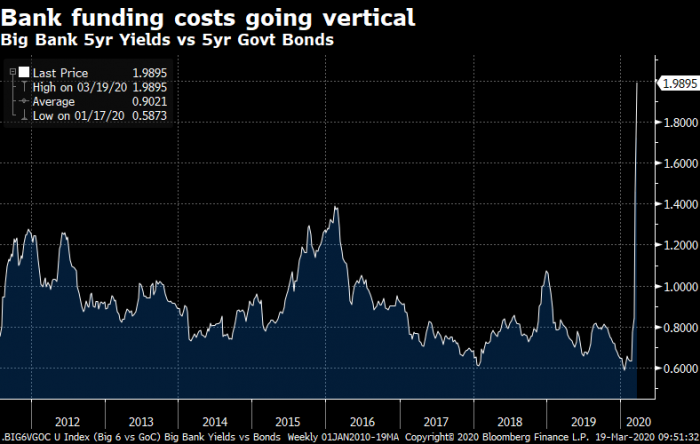

Bank Risk: Investors are once again pushing up banks’ funding costs in the bond market, relative to Canadian government bonds. The premium investors are charging banks on 5-year borrowing is now almost 200 bps, highest since the credit crisis. This is one key reason we’re seeing mortgage rates jump, despite the billions in liquidity our government has injected in the market.

Source: Bloomberg

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

@thespy how are the penalties with TD considering a 5 year fixed, they are willing to match HSBC at 2.59 (not a refinance or renewal fresh mortgage on a property I just bought)

What no one seems to be talking about is the implications of mortgage payment deferrals on personal credit bureaus, ratings and scores. In our age of automation, I suspect these will be reporting as late payment? Which could have major long term implications?

@joe it is up to the credit provider to report late payments etc to Equifax and transunion. If they are willing to defer it I doubt they are going to report late payment.

log in

log in

11 Comments

Did bank take on the new benchmark with the BoC drop to 5.04?

Hi Meridith, Yes, the official benchmark (minimum stress test rate) is now 5.04%.

I am a mortgage broker and I cannot find the stress test lowered to 5.04% anywhere. Please post your source.

Hi Elizabeth and Sam,

See time series V80691335 here: https://www.bankofcanada.ca/rates/banking-and-financial-statistics/posted-interest-rates-offered-by-chartered-banks/

Cheers

It hasnt been announced anywhere?

Why no news on this anywhere yet?

@thespy how are the penalties with TD considering a 5 year fixed, they are willing to match HSBC at 2.59 (not a refinance or renewal fresh mortgage on a property I just bought)

Thanks!

Harry

Hey Harry, They’re not much better than HSBC. Use a smaller lender if you want better penalties. Cheers..

What no one seems to be talking about is the implications of mortgage payment deferrals on personal credit bureaus, ratings and scores. In our age of automation, I suspect these will be reporting as late payment? Which could have major long term implications?

Hey Joe, Just reported on this today. See our 4:31pm update.

@joe it is up to the credit provider to report late payments etc to Equifax and transunion. If they are willing to defer it I doubt they are going to report late payment.