Hopefully Not Reality: Despite the government’s relief plan, including mortgage payment deferrals—1 in 10 (9%) of mortgagors say they won’t be able to pay their mortgage in three months or less (Source: DART & maru/BLUE Survey). Few in the industry expect anywhere near 9% defaults, but the numbers we do get may surprise people. Back in the 1980s, prime mortgage defaults were over 1%. They peaked at 0.65% and 0.45% in the 1990-92 and 2008-09 recessions, respectively, according to CBA data.

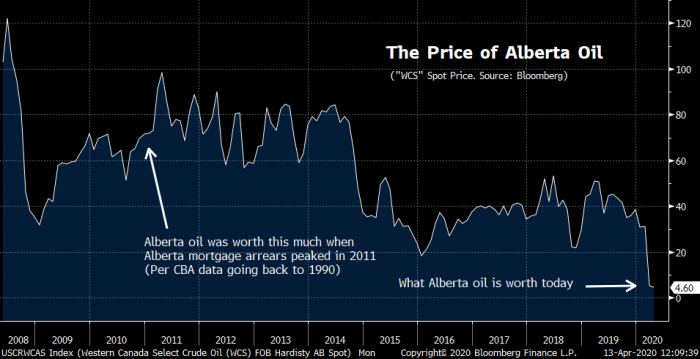

Grim AlbertaNumbers: In January 2011, the oil-dependent province posted its highest arrears rate in CBA records: 0.84%. At the time, the price of Alberta oil was 15 times what it is today. With unemployment now forecast at 25%+, late 2020 to 2022 defaults could obliterate previous records, leading to a major lending pullback—just when Albertans need refinances the most.

Hope: Seventy COVID-19 vaccines are in development, according to the World Health Organization. At least three look promising. (Bloomberg story)

A Big “If”: “In the second half of [March], [Toronto] saw a dip in both sales and new listings. When you look at it on a year-over-year basis, both were down by a similar amount. That means…there’s still a similar number of people interested in each listing. If that continues (And it won’t. -Ed.), prices might remain relatively stable…but right now it doesn’t make a lot of sense to be out there buying.”—Jason Mercer, TREB senior market analyst. (Toronto Life story)

Because They Make a Lot of Money: That’s why banks should charge zero interest on deferred mortgage payments—or forgive those payments altogether—argue some in this story. Banks get little sympathy despite their voluntary and unprecedented agreement to defer payments to keep borrowers solvent. Nonetheless, it would have been worth mentioning in the article that banks obtain much of their mortgage funds from investors. Despite not being paid by borrowers who defer, banks must continue paying investors on the money they’ve lent out. Banks losing money on deferred loans is not something the government should expect.

Stimulus: Not Enough, Nor Fast Enough: 68% of Vancouver homeowners made their mortgage payments in April. But just 55% say they’ll be able to meet their payment in May (poll). CTV reports 70% of renters paid their rent in April, and 63% said they’d be able to pay May rent.

Vancouver Mayor: If 25% of homeowners default on their property taxes, “we could shed up to an additional $325 million in revenues…Losing more than half-a-billion dollars in operating funds in 2020 would devastate the City’s financial position, forcing us to liquefy assets and exhaust every reserve fund we have — just to avoid insolvency.” Many of Canada’s 300 other cities with 10,000+ populations could be in the same boat. (CTV Story)

Insolvency Expert: “Many people will use debt to survive during this period…” You can say that again. Here’s a tip piece on negotiating credit deferrals.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Does someone with a CMHC insured loan-to-value mortgage of about 50% still qualify for those (high ratio) mortgage rates like the HSBC 2.39% 5yr. fixed or the IntelliMortgage 2.03% 5yr. fixed which I can’t seem to find now, maybe the IntelliMortgage rate was a typo.

Thx

Hey Steve, Did CIBC *just* make that offer to you Tuesday on a renewal? I’d love to see a copy of it at [email protected] if you don’t mind confidentially forwarding. Prime – 0.72% is well below every other CIBC variable rate we’ve heard of in the last few weeks. 1.73% is solid for a borrower suited to a variable. The BoC would have to hike 4+ times — probably in short order — for a well-qualified borrower to lose in this case, based on interest cost alone. Albeit, there are other considerations besides interest rate speculation.

Considering the probable lasting effects of COVID, I’d say the odds of a rush to raise rates before 2022 are very low. I’d definitely go for the variable rate and I think worse case you’ll end up break even if rates surge later on. Fixed rates are quite disappointing at the moment, I’d have expected much better.

@steve

Look at the mortgage update from April 10 on This site. It talks about economy, rates and some comparison and forecasts. It will help you.

I think things are in favor of variable rates considering your good discount.

log in

log in

8 Comments

Does someone with a CMHC insured loan-to-value mortgage of about 50% still qualify for those (high ratio) mortgage rates like the HSBC 2.39% 5yr. fixed or the IntelliMortgage 2.03% 5yr. fixed which I can’t seem to find now, maybe the IntelliMortgage rate was a typo.

Thx

Hi Rob, At some lenders, yes. At others, no. Here are HSBC’s rules: https://www.hsbc.ca/content/dam/hsbc/ca/docs/pdf/hsbc-2020-high-ratio-mortgage-rate-5-year-offer-tc-en.pdf

I was offered prime – 0.72 for 5 yrs by CIBC today. I also have an offer of 5 yr fixed of 2.42. Am I crazy to not take this prime – 0.72 offer?

Hey Steve, Did CIBC *just* make that offer to you Tuesday on a renewal? I’d love to see a copy of it at [email protected] if you don’t mind confidentially forwarding. Prime – 0.72% is well below every other CIBC variable rate we’ve heard of in the last few weeks. 1.73% is solid for a borrower suited to a variable. The BoC would have to hike 4+ times — probably in short order — for a well-qualified borrower to lose in this case, based on interest cost alone. Albeit, there are other considerations besides interest rate speculation.

Considering the probable lasting effects of COVID, I’d say the odds of a rush to raise rates before 2022 are very low. I’d definitely go for the variable rate and I think worse case you’ll end up break even if rates surge later on. Fixed rates are quite disappointing at the moment, I’d have expected much better.

Hi WillyBaldy, FWIW, economists side with your no-rush thesis.

@steve

Look at the mortgage update from April 10 on This site. It talks about economy, rates and some comparison and forecasts. It will help you.

I think things are in favor of variable rates considering your good discount.

Thanks everyone for the replies. They really

Help. I also hope everyone is staying safe out there!