log in

log inPrior to the last few days, consumers had expected falling Bank of Canada rates and lower bond yields to translate into cheaper mortgage rates. And they have, big-time.

But these two benchmarks aren’t the only things that determine mortgage pricing. Borrowers were reminded this weekend that liquidity and credit risk are also in the equation.

Ten days ago we noted that mortgage rates were diving, but that liquidity constraints could potentially inflate lenders’ costs, and mortgage rates. Liquidity refers to how easily (and cheaply) banks can raise capital. Illiquidity in the banking sector is always bad news for mortgage rates.

Well, it’s happening. Gauges of how willing banks are to lend to one another have deteriorated rapidly. Here’s one such measure:

Without boring you over details, suffice it to say this chart shows investors are becoming more fearful of credit defaults and illiquidity in the banking system.

It’s not coincidence, then, that some banks are slashing their variable-rate mortgage discounts to pad revenues. Scotiabank, for example, hiked its 5-year published variable rate by a whopping 60 bps on Saturday, to 3.45%.

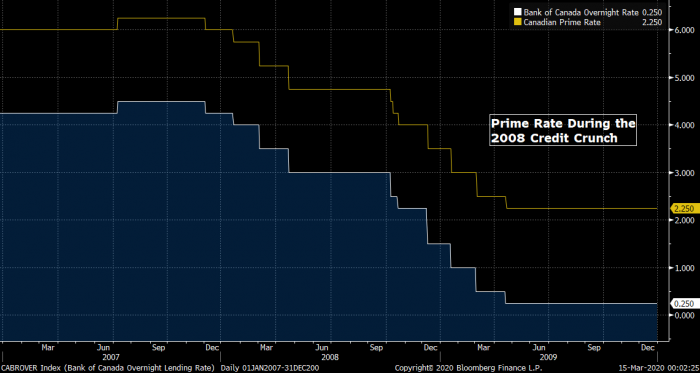

We’ve seen these shock-and-awe rate moves before. On October 6, 2008, in the midst of the credit crisis, TD shocked the market with a massive 100-bps rate increase to prime + 1.00%. It applied to new variable and HELOC customers. TD rates were below prime just days before.

Today, even fixed rates are rising at some lenders, and the pop in bond yields on Friday didn’t help. Albeit, the fixed-rate impact is nowhere near as pronounced so far.

How Long Could It Last?

When the Bank of Canada cuts rates—particularly if they’re emergency cuts or leading into recession—it doesn’t start hiking again for over two years on average. That’s based on a historical lookup back to the start of inflation targeting in 1991.

If a downturn is bad enough, like the Great Recession, subsequent rate increases can be modest—allowing variable-rate holders to outperform 5-year fixed terms, despite the hikes.

Results are heavily inflation-dependent, however. And there’s no way to forecast inflation in 2021 or 2022, as we don’t know how much economic damage CVirus will do.

What we do know is that once the virus is under control there, will be a king-sized rate rally thanks to pent-up economic demand. If history is a guide, that rally could be 100 to 200+ bps. If credit markets seize up enough, we could even see rates jump before the recovery. That’s the risk you take with a variable.

That said, recessions are never bullish for mortgage rates. Even if a floating-rate borrower gets caught in an eventual rate rally, there’s a solid chance their 5-year borrowing cost will come in lower than a typical 5-year fixed mortgage.

Of course, rate timing is a well-known form of masochism. The market exists to frustrate rate timers. When selecting a mortgage term, it’s much better to focus on factors we can control. (For examples, see: Fixed or variable?)

Home Sellers on Alert

“We are coming to the view now that because of the virus and the meltdown in financial markets, we will most likely see a decline in buying activity through at least parts of the spring market, and maybe even going into the summer market,” said RBC Economics.

Home sellers read this stuff and fear travels fast. Fewer people home shop, open houses are cancelled, more sellers try to sell online, etc.

If buyers stay on the sidelines and sellers get spooked, Canada could witness the fastest reversal in its sales-to-listings ratio since the financial crisis.

South of the border, 16% of Realtors report seeing a drop in buyer activity, according to the National Association of Realtors. In harder-hit states like Washington, the number is almost 20%. But, just 2% of Realtors report more listings in their markets as a direct result of Covid-19. (Note: This survey is 5-6 days old.)

In Perspective

As you saw in the 3-month LIBOR – OIS chart during the previous section, credit market panic is nowhere near as extreme as the 2008 crisis. It would be drastically premature to suggest it will be, although a further spike is likely.

Economic panics almost always dissipate in a year or two. Despite being a health pandemic as well, North America has got through worse. Civilization (and the stock market) quickly recovered from the far more deadly 1918 Spanish flu, which infected about 1/4 of the U.S. population, killed over half a million Americans (tens of millions worldwide) and cut life expectancy by 10-12 years in 1918, according to some estimates.

Human resiliency is worth remembering when contemplating a home purchase. No question, it’s going to be a bumpy ride through the end of this year. But financial and real estate markets will again see daylight.

Parting Tips

Four quick points for mortgage shoppers:

- Floating rates continue to look attractive and there are plenty of low-cost variables still to be had. If you need a variable mortgage before August, it would be heedless not to secure a rate now given the risks above.

- Those already in a variable don’t need to worry about discounts evaporating during their mortgage term. One’s discount from prime rate doesn’t change once the mortgage starts.

- Even during one of the worst financial crises of all time (2008-09), Canada’s benchmark prime rate still fell with each Bank of Canada overnight rate cut. Those with variable rates should assume that will continue until proven otherwise. Keep in mind, however, that each individual lender sets its own prime rate, so yours doesn’t have to follow the official benchmark.

- Fixed rates aren’t rising like variable rates, not yet. But there’s a risk they could. Get a rate guarantee soon if you need a fixed mortgage in the next four months.

8 Comments

Not clear on what Scotia Bank did March 14th . . .did they raise the variable rate? I read you to say “Slash” . I just got a letter from them early last week saying they had dropped it to 2.9 %. Please clarify as I find their customer service advice by phone confusing and my local branch rep has not responded to my request for advuce put to her colleague last Saturday in a local branch in Calgary

Hi Bill, Scotia slashed its variable-rate discount from prime which raises the rate for new customers.

Existing Scotia variable-rate customers are unaffected. They’ll only be impacted if Scotia’s prime rate changes.

Comparing COVID19 to Spanish Flu is apples to oranges. COVID19 isn’t nearly as deadly and the ease of travelling the world today versus 1918, Spanish Flu would have spread faster and had a deadlier result.

COVID19 is overreacted mostly creating Fear (capital F) in everyone and the media’s constant coverage with numerous what-if scenarios resulted in panic from the Fear of unknown. Toilet paper? Food hoarding? Yes we need to be prepared, but this is not an apocalypse. But the media is treating it like it is. Is it’s a media test run of a future deadly pandemic?

Canada is dependant on the world. Whatever happens elsewhere affects our economy. I’ve said this before, we may never see mortgage rates greater than 10% like in the 80s and 90s. And I would be bullish in suggesting we’d never see higher than 5% on a discounted basis. It would stifle economic growth.

The road to rates increasing on 5yr 5% discounted is a long and winding path.

Tbahz,

Re: “Comparing COVID19 to Spanish Flu is apples to oranges.“

Yep, and that’s the point.

Greate analysis and information as always. Thank you!

Covid19 appears to have a similar death rate to Spanish Flu.

Many Canadians likely just realized this is serious when Hockey got shut down.

See Spanish Flu, Wikipedia.

Should one have a existing variable rate currently would you advise to lock into a fixed rate?

@Bill

There is no debate. Spanish flu was the worst pandemic of the last 150 years. Its mortality rate was 1-2 percentage points higher than Covid-19.

https://virus.stanford.edu/uda/