Many modest-income Canadians who have never owned a home may never own a home, at least not an average home. That is, unless they can live almost anywhere (work remotely, for example), and/or they’re buying with someone else (e.g., a significant other). Here’s why…

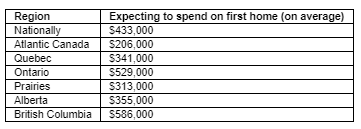

First-time homebuyers now expect to pay $433,000 on average, according to a recent BMO survey. That’s a big deal because a typical individual first-timer “only” makes around $60,000 a year, according to StatsCan. With the minimum 5% down, the most expensive home that person could qualify for is about $248,000 (assuming no condo fees and $500 in other monthly obligations, like car payments). That’s over 42% less than what first-timers plan to spend, according to the poll.

Note to single folks out there looking for love (and a new home): You might want to ensure your new sweetheart has a 720+ FICO score and enough provable income to help you pass the mortgage stress test.

Meanwhile, the country’s average home costs even more–over $678,000. That’s a jaw-dropping 25% increase in just 12 months—the biggest nationwide price gain in over three decades, per CREA’s data.

Soaring prices mean surging down payments. 36% of first-timers report they can only muster between a 5 and 10% down payment.

That’s interesting because the last time prices went parabolic to this degree (+25% y/y) was 1989. It was a historical turning point for the market. After a run-up that saw home prices double in just four years, prices sold off 13% nationally following that 1989 peak and then flat-lined for the next decade. Although, they fell far more in places like Toronto.

To say that home prices have run away from newbie buyers is an understatement. And 40% have had enough, telling BMO they’ll wait to buy a home until “prices come down.”

None of this is a prediction of what’s to come. It’s more of a reminder not to panic-buy. Soaring prices have a way of drawing out sellers and inventory always returns to the market to slow the ascent. It may not happen this month or next (market timing is for masochists), but it ultimately happens.

Source: BMO

Don’t Get Caught in the Penalty Hype

Some mortgage advisors are pushing variable rates because, “If you ever wanted to sell in a pinch, the penalties to break a fixed rate can be steep.”

On its own, that’s a weak reason to go variable…if:

In such cases, the chances of paying a steep IRD penalty on a fixed mortgage are largely reduced. Far more concerning to an average borrower should be interest rate exposure, particularly as the economic recovery becomes entrenched.

This & That

Properties not appraising for prices paid in maniacal bidding wars could be “the next problem,” says this realtor.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

For me what is most disturbing is the faith our government and the media puts on the numbers provided by the real estate organizations and even the mortgage industry, soon of later people have to realize is that it is impossible to be impartial when their main source of income is directly related to the numbers they are providing to the public

I am just waiting for my citizenship to arrive, so it is easier to migrate to US for work. With high cost of living, low quality of life and low salaries, Canada doesn’t have much to offer.

Ashley I am similar I came to Canada few years ago but is so so expensive to live meanwhile jobs pay too low.. I have family in USA so am going after pandemic to there with cheaper to live better wages lower taxes

I have family and friends in NJ, and over there a detached 4BD costs 650k that too good one. Plus, daily living is so much cheaper – gas, food,.., and salaries are higher. Healthcare is actually more expensive in Canada considering the amount of tax goes towards it, yes Healthcare is NOT FREE in Canada.

Healthcare is only free if you pay no taxes. Then the liberals and NDP give you a home, EI and healthcare for free or near free. The incentive to succeed in this country declines with every government handout. It’s sickening. Idiot politicians think they can just keep running deficits or tax the rich, who thief consider people who make over $100k a year. Have you every tried to live on $100k? With all the different layers of taxes you’re lucky to keep 5 cents in your pocket for every dollar you make. We need a government that makes all citizens pay their fair share. If you make $10,000 you should pay at least some tax. The rest of us have to.

log in

log in

7 Comments

For me what is most disturbing is the faith our government and the media puts on the numbers provided by the real estate organizations and even the mortgage industry, soon of later people have to realize is that it is impossible to be impartial when their main source of income is directly related to the numbers they are providing to the public

Some might choose to leave the country altogether. Both people exiting the market and potential first time buyers.

I am just waiting for my citizenship to arrive, so it is easier to migrate to US for work. With high cost of living, low quality of life and low salaries, Canada doesn’t have much to offer.

I would love to read an article on penalties, those who are in both categories. Thanks for all the great information.

Ashley I am similar I came to Canada few years ago but is so so expensive to live meanwhile jobs pay too low.. I have family in USA so am going after pandemic to there with cheaper to live better wages lower taxes

I have family and friends in NJ, and over there a detached 4BD costs 650k that too good one. Plus, daily living is so much cheaper – gas, food,.., and salaries are higher. Healthcare is actually more expensive in Canada considering the amount of tax goes towards it, yes Healthcare is NOT FREE in Canada.

Healthcare is only free if you pay no taxes. Then the liberals and NDP give you a home, EI and healthcare for free or near free. The incentive to succeed in this country declines with every government handout. It’s sickening. Idiot politicians think they can just keep running deficits or tax the rich, who thief consider people who make over $100k a year. Have you every tried to live on $100k? With all the different layers of taxes you’re lucky to keep 5 cents in your pocket for every dollar you make. We need a government that makes all citizens pay their fair share. If you make $10,000 you should pay at least some tax. The rest of us have to.