log in

log in

— The Mortgage Report : June 17 —

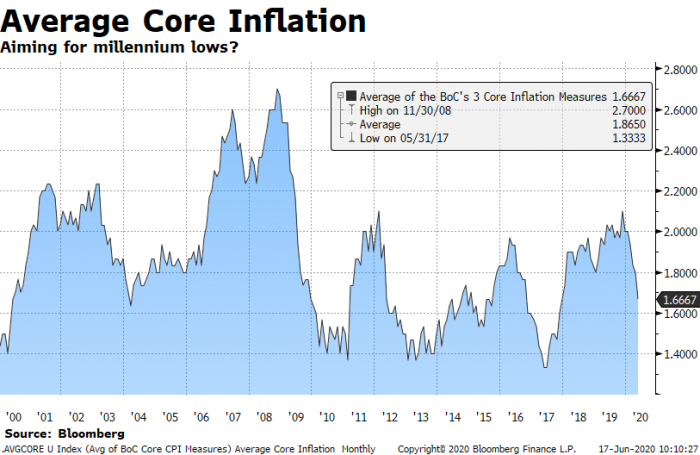

- Prices Slide: The Bank of Canada wants average core inflation at/near 2%, but it’s currently 1.67% and diving. That’s noteworthy for borrowers given inflation expectations are a primary determinant of mortgage rates. Inflation’s descent may slow thanks to rebounding oil prices, but it’ll continue dropping economists say—potentially to lows we haven’t seen in a few decades. Of course, what’s happening now is less important for rates than what’ll happen next year, and the year after. In a research note, CIBC said it has yet to speak to an investor that thinks Canada will emerge from recession faster than in 2009. At a minimum, it usually takes a couple years for inflation to rebound meaningfully above 2% following a recession, but with record unemployment this time, it could take longer. Two percent inflation is hard enough to sustain in an old economy facing over-indebtedness, an ageing population, technology-driven disinflation, etc.—let alone in a recession-ravaged economy where more than 10% of workers could remain unemployed or under-employed for years.

- Liberal Debt Ratios: Brokers now have new options for people with high debt ratios. Whereas 44% is the typical industry limit for a borrower’s total debt service ratio (i.e., the ratio of your monthly obligations to your monthly gross income), some lenders now advertise up to 60%. That may sound crazy, but high debt ratios on paper don’t always mean a borrower is a high risk. Lenders won’t lend a dime if they don’t think they’ll get their money back. No institutional lender wants to take someone’s house. These 60% TDS products are aimed at people who are a reasonable credit risk, people who have:

- 35-40% equity

- or as little as 20% on exception, for those with great credit

- proof of income to make their payments

- albeit, the borrower might have an insufficient long-term track record of income

- this could include someone who had income interruption but is back on the job, or who recently started a new business and doesn’t have the standard 2-year income history that lenders typically want

- temporarily high debt ratios

- the borrower may have a big monthly payment ending soon, an inheritance on the way, a deal closing that will generate a windfall, another property being sold, or some other event that will reduce total debt ratios.

- a marketable property in a liquid housing market

- Lenders usually have no appetite to lend at 60% TDS in small towns, or on subpar properties (e.g., a house next to a gas station or cemetary)

- satisfactory credit

- e.g. a FICO score in the 600s or higher (people with lots of equity usually have good credit)

- 35-40% equity

These 60% TDS products most often come with 1-year terms and rates in the high 3s to high 4s, plus a 1% lender fee. They’re typically available for purchases and refinances of owner-occupied properties. If you’ve had short-term financial or employment issues that are now corrected, and you can’t get approved by a bank because of a temporarily inflated debt load, a broker experienced in alternative lending may be the answer.

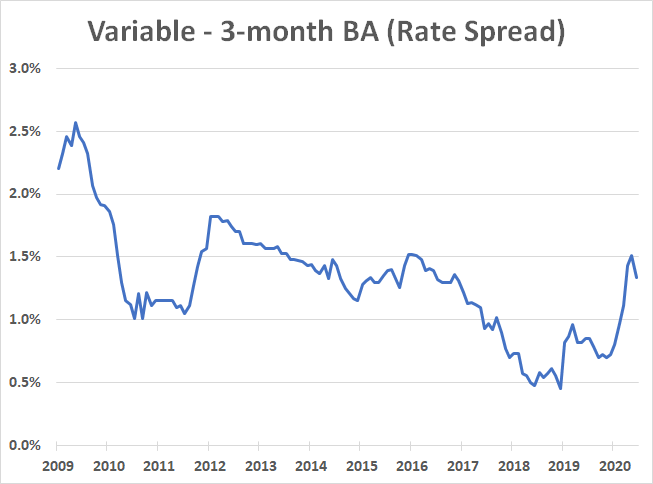

- Room to Improve: Variable rates for new borrowers will get better, even if prime rate doesn’t fall anymore. The reason: lenders’ costs have fallen after spiking during the COVID crisis. As a result, lenders have profit margin to play with. The chart below is a crude representation of that margin. It shows the difference between the lowest nationally-available variable rate minus the 3-month bankers’ acceptance yield (which is a rough proxy for a lender’s base variable-rate funding costs). If mortgage defaults don’t surge, this spread should drift closer to 1.00% before too long. When that happens, assuming prime rate stays constant, we’ll see Canada’s lowest variable rates improve. Barring the unexpected, there’s a good chance we could even see prime – 0.90% (1.55%) or better by the end of this year. (Note: None of this impacts the rates paid by existing floating-rate borrowers.)

4 Comments

Sorry for the stupid question but can inflation ever go negative?

Hey Doug, It’s great question and yes, inflation in Canada was negative in April and May — i.e., overall prices were falling.

Persistently negative inflation is known as deflation and it’s something central banks try to avoid at all costs.

Yes, inflation represents increasing prices of everything we purchase, food, clothing, vehicles, homes, even taxes are considered.

A period of price drop or negative inflation is referred to as deflation. If this occurs due to something good, like say government running well, paying its debts off, and being able to lower taxes to citizens, that is a good thing, new manufacturing technology that can aid making products that sell cheaper than the last generation is another good was to get deflation, but typically widespread deflation only occurs during prolonged recessions and depressions where demand for products drops because of reduced wages and widespread unemployment. The reduced demand will typically force manufacturers to reduce pricing trying to get rid of excess product supply.

This sounds good on the surface, but if it lasts too long, employees get layed off, or pay cuts. Businesses reduce their production as a result dragging the economy down further… It can become a bad cycle that feeds itself and can create a bad negative momentum. Once people see this start, they also tend to save more and spend less, making the economy shrink even more…

That’s why most government desparately want some optimism for inflation /growth so people continue to spend and keep the positive momentum going. That is largely why we have seen interest rates drop from their near 20% in the 80’s to effective zero today, and government over spending around the world… Its become a ponzi scheme of sorts… Eventually we will have to deal with the debt. Recessions actually produce innovation and efficiency ideas as people and companies become creative on how to do more with less, so they are short term pain for the long term gain

Great post Kevin!