log in

log inRBC waited exactly three hours and 11 minutes to take advantage of the Bank of Canada’s 1/4 point rate hike today.

RBC waited exactly three hours and 11 minutes to take advantage of the

RBC waited exactly three hours and 11 minutes to take advantage of the RBC, which is typically Canada’s mortgage rate leader, boosted its prime rate by the same amount, to 3.45%. The other Big 5 banks matched its move within a few hours.

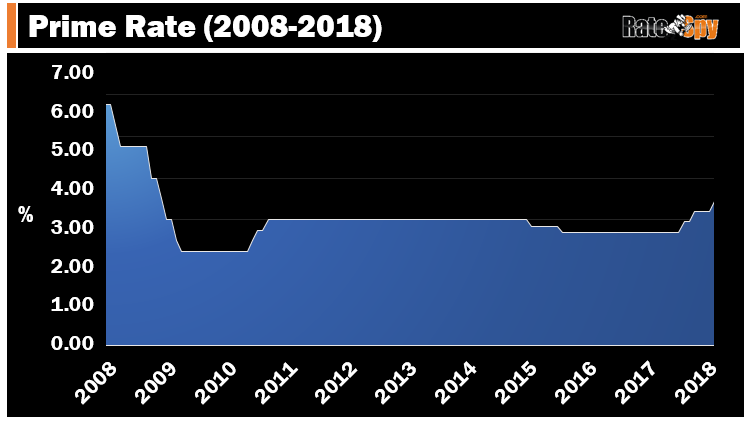

Prime Time

The new 3.45% prime rate takes effect tomorrow at most big lenders. It’s been nine long years since we’ve seen prime that high.

These rates are a whole new world for younger mortgagors or those approaching their first mortgage renewal. Variable-rate borrowers who got their mortgage before last July have now seen their rate spike 75 bps. That’s almost $75 a month for the average-sized (i.e., $200,000-ish) adjustable rate mortgage.

SpyTip: Not all floating rates have floating payments. Variable-rate mortgages have fixed payments. Hence, today’s hike won’t affect the cashflow of variable-rate borrowers, just the amount of interest they’ll cough up (they’ll pay more interest / less principal).

The Fixed Rate Situ

As for fixed mortgage rates, they’re in a holding pattern, having already risen this week and last. Their next move is dependent on whether bond traders take the 5-year yield to:

- 2.15%-or more — in which case fixed rates will likely rise

- 1.80%-or less — in which case fixed rates will likely fall

At the time I’m writing this:

- The 5-year bond yield is at 2.01%

- The best 5-year fixed rates are under 2.79% (the average full-featured conventional 5-fixed rate is about 3.39%)

- The federal “mortgage stress test” rate is 5.14% (more on that)

What Happens Next

The Bank of Canada’s takeaway line today was: “While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed.”

The Bank of Canada’s takeaway line today was: “While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed.”

The Bank of Canada’s takeaway line today was: “While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed.”As for the market, it still thinks we’ll get another hike or two later this year. As usual, bond yields will validate whether that’s true or not. If another hike is to be, it’ll be priced into yields well in advance.

If you’re trying to decipher all this and pick a mortgage term, look beyond the next few rate hikes (assuming they happen). Remember the following:

- If you plan to have a mortgage for 5+ years, your average rate over that timeframe is far more important than your rate this year.

- Rising oil prices aside, we’re in one of the biggest disinflationary cycles of the last century. Think the Amazon.com effect, automation, aging demographics, overleveraged consumers, etc. This is a long-term trend that won’t end for (potentially) years.

- Assuming you’re a well-qualified borrower, floating rates priced 1+ points below 5-year fixed rates are therefore a steal (and the best variable rates meet that criteria).

- Lenders rake you over the coals when you lock a variable-rate into a fixed rate (because they know you’re a captive customer who has to pay a penalty to get a good fixed rate elsewhere).

- Variable rates are much less risky if you have a low debt-to-income ratio, assets to fall back on and/or a short remaining amortization or small mortgage size (relative to income).

In any event, the next Bank of Canada rate party happens March 7. You may hear a cacophony of rate hike chatter before then. But don’t let it scare you too much. If prime rate breaks 4.00%, then you can worry.

2 Comments

Those 10-year fixed rates at 3.59% are starting to look a lot more appetizing these days.

Word.

Just be sure you never break it before 5 years.