“Interest rate risk could rise if the economy outperforms expectations,” said RBC Economics on Tuesday, as the bank raised three of its special fixed rates:

3yr: 2.19% to 2.24%

4yr: 2.09% to 2.29%

5yr: 2.04% to 2.24%

That leaves just CIBC with advertised 5-year fixed rates under 2.00%. But advertised and reality are two different things. If you’re a strong borrower with any luck or negotiation skills, you should be able to get 1.99% or less from any big bank. And, of course, non-bank lenders are lower still. A quick check of our rate tables will reveal uninsured 5-year rates at 1.79% to 1.69% or less.

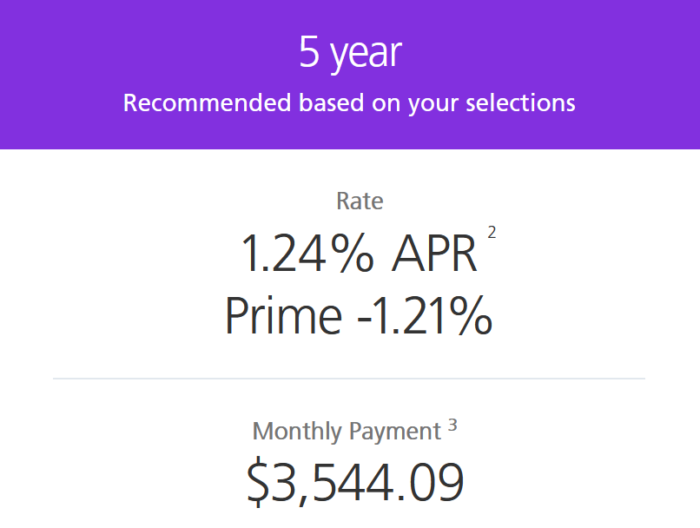

Like the other Big 5 banks, the golden lion also trimmed its special 5-year variable rate—in RBC’s case from 1.75% to 1.60% (prime -0.85%). But that’s nothing to write home about. Scotiabank’s eHOME platform is advertising as low as prime – 1.21% for insured purchases, second only to HSBC’s 0.99%.

The best uninsured 10-year fixed rate of all time is no more. Tangerine jacked the rate on its 2.14% decade-mortgage by a whopping 70 basis points to 2.84%.

That said, if you’re an inflation hawk with an urge to lock in till 2031, and can handle the prepayment penalty risk of a 10-year term, you can still find 2.24% in the biggest English-speaking provinces.

CMHC is replacing its scrappy CEO Evan Siddall with its SVP, Romy Bowers. What’s interesting is that the government began reviewing CEO applications on July 30, 2020, and five months later (at the end of Siddall’s contract), they had found no suitable replacement. And now, a few months later, Bowers—who was there all along—is named the new CEO. Her delayed appointment will make some people deem her a backup plan. That’s too bad, because Bowers is smart, accomplished and level-headed—just what CMHC needs after Evan’s controversial tenure.

Speaking of which, CMHC-talk on Twitter will be a heck of a lot more boring with Evan sailing off into the horizon. Some in the industry are looking forward to that. But Siddall’s sometimes-brash confrontational style triggered important debates about housing policy, dialogues that never would have happened under CMHC’s prior conservative leadership.

Siddall did some good in his years. He made CMHC more transparent, beefed up its data and analytics capabilities, bolstered low-income housing and improved CMHC’s risk profile. Anyone who still argues—after his tenure—that CMHC creates too much risk for taxpayers is woefully uninformed.

Unfortunately, Siddall also failed in important ways, like building consensus in the market and upholding CMHC’s obligation to enhance lender competition. The housing and mortgage industries never felt like they were on the same team as him. His sometimes insulting, argumentative and very-public statements about real estate and lending professionals, while occasionally grounded in truth, hurt CMHC’s reputation. You simply cannot solve the most pressing housing crisis of our time without inspiring all stakeholders with a common goal. Evan’s approach is a key reason the agency took a market share hit.

Siddall also failed at marshalling enough resources to address one of housing’s most pressing issues: inadequate housing supply for middle-class Canadians. A supply fix requires massive coordination at the federal, provincial and municipal levels. CMHC is Canada’s housing agency. The obligation to satisfy the affordable home purchase demands of all Canadians, not just low-income Canadians, falls in CMHC’s lap. Yet, Evan leaves his post amid chronically tight housing inventory (and yes, inventories were tight before COVID as well). On that count, the country is no further ahead today than when he took office.

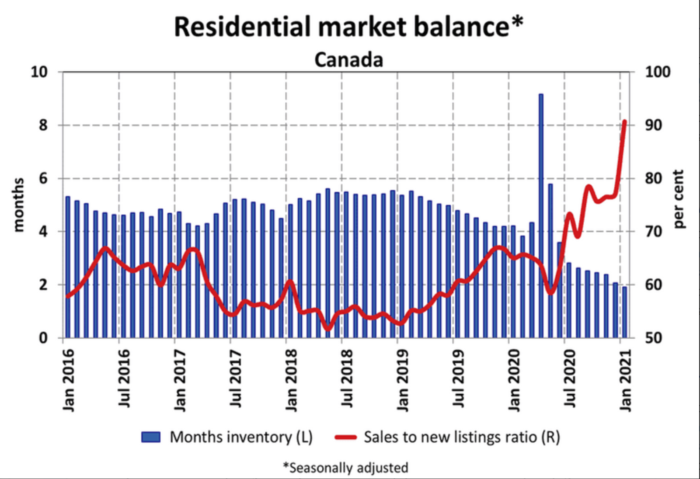

Source: CREA

This & That

2020 GDP plunged 5.4% y/y, the worst on record. But that’s old news.”[Canada’s] 9.6% annualized increase in fourth-quarter GDP was three times as strong as the consensus forecast from just a couple of months ago,” said Capital Economics…We expect GDP to return to its pre-pandemic level by the third quarter of this year.”

RBC on housing: “[The] main near-term risk is overheating, not price collapse…Odds of policy intervention increase the hotter markets get…policy-makers come under intense pressure to stabilize markets and contain household leverage risks when prices spiral upward.” (Source)

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

log in

log in

4 Comments

Scotia eHome is killing the other banks on rate. I wonder when the rest of the oligopoly will wake up and respond.

Isn’t eHome still just for purchase of owner-occupied homes? And I doubt they let you switch from a regular Scotia mortgage.

As for their rates, I don’t think they were beating CIBC and others offering 1.49% for 4yr fixed mortgages in December and January.

Noticed that with Tangerine. I locked in yesterday @ 2.14 for 10 years the day before the increase today.

Just in time as my term is up with BMO on June 25th

This is my last term with no plans on ever moving…so I am pretty happy about that rate. 10 years is a long time.

Regardless of the variable/fixed debate back and forth a 10 year fixed @ 2.14 is a steal to be honest.

Can someone explain to me why CMHC doesn’t provide good data on mortgage rates?

Mortgage rates are important for housing right?

They should provide aggregate rate data for every term on every CMHC insured mortgage, on a weekly basis. They have all the data.

Siddall has been talking about “closing housing data gaps” for years. Well here is one glaringly wide gap he and CMHC haven’t closed.