log in

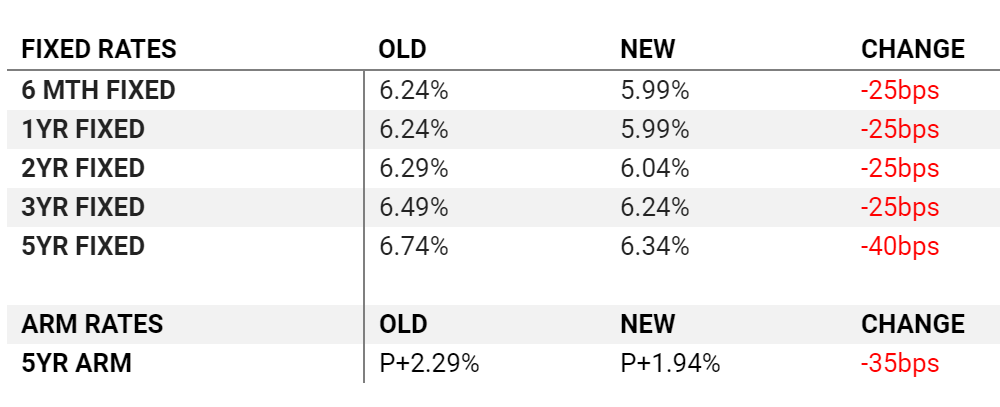

log in Equitable Bank has slashed its reverse mortgage rates. That’s welcome news for seniors needing to tap home equity, particularly those who can’t qualify for regular financing or don’t want the payments.

Equitable Bank has slashed its reverse mortgage rates. That’s welcome news for seniors needing to tap home equity, particularly those who can’t qualify for regular financing or don’t want the payments.

The company—which has remained in HomeEquity Bank’s shadow—is now working noticeably harder to separate itself from its better-known rival. And its rate cuts this week do just that, assuming HomeEquity Bank doesn’t match them.

“This [rate] reduction is consistent with Equitable Bank’s strategy of providing clients with options that help preserve hard-earned equity and is reflective of a decline in [funding costs],” said Paul von Martels, VP, Prime and Reverse Mortgage Credit at Equitable Bank.

How Much Do These Rates Save People?

“All else being equal, an applicant advancing a $200,000 PATH [reverse mortgage] for a 5-year interest rate…will save about $5,300 of interest over five years with our new rate offerings,” Von Martels calculates. “Many loans will be outstanding for more than five years, so this $5300 of savings could be much more significant if you consider it over the life of a loan.”

Equitable uses GICs to fund its reverse mortgages. It tries to “match-fund” (i.e., take the money it gets from GIC deposits and use it to fund reverse mortgages with a similar expected borrowing timeframe). That makes 5-year GICs the primary source of capital it lends out as reverse mortgages. The reason that matters is because its 5-year GIC rates have fallen “~40-50 bps” since its last rate change, says von Martels. “I think the story is that we’ve taken the lead on passing this funding cost difference back to the customer in short order,” he adds.

We suspect HomeEquity Bank won’t be too far behind with rate cuts of its own. Whether it matches these moves by Equitable will be interesting to watch.

Other Reverse Mortgage Differences

This move adds to Equitable’s recent reverse mortgage improvements, which include slashing its prepayment penalties to just five months’ interest or less. Compare that to penalties of up to 5% of principal at its competitor.

This move adds to Equitable’s recent reverse mortgage improvements, which include slashing its prepayment penalties to just five months’ interest or less. Compare that to penalties of up to 5% of

This move adds to Equitable’s recent reverse mortgage improvements, which include slashing its prepayment penalties to just five months’ interest or less. Compare that to penalties of up to 5% of If you paid off a $150,000 reverse mortgage in the second year of your term, for example, you’d pay about $3,400 at Equitable Bank, versus $6,000+ at HomeEquity Bank.

Spy tip: There is zero prepayment penalty at both companies in the event of death, and a 50% discount if the borrower moves into long-term care.

The biggest knock on Equitable’s PATH Reverse Mortgage has been its lower loan-to-value limits compared with HomeEquity Bank. In other words, seniors may not qualify for as much money. (For those who don’t need the extra cash, this is mostly a moot point.)

Von Martels says, “We have no immediate plans of increasing LTVs…I believe that over time the market will benefit from the acute differences [in the two products]. The lower LTV strategy is consistent with our focus on equity preservation.”

“Interestingly, we see the majority of our clients having available undrawn funds; meaning they qualify for x, and at origination draw 75% of x, leaving the undrawn [amount] for future needs…”

Equitable’s lower loan-to-values also reduce its capital costs. By keeping its maximum loan amounts to no more than 40% of the property value at origination (a key threshold with the banking regulator), it reduces the amount of liquid assets the bank must keep on hand. That enables Equitable to (at least theoretically) be more competitive on things like rates, fees and prepayment charges.

Sidebar: Equitable Bank also recently released a product that lets people get a line of credit secured against their whole life insurance policy. They call it the “Cash Surrender Value (CSV) Line of Credit.” To qualify, your life insurance policy must have a “cash surrender value” (i.e., it’s not available on term life insurance). The interest rate is currently very reasonable at prime rate plus 1.25%. Contact the bank for more details.

7 Comments

Never would I use a reverse mortgag……ever.

Some people have no better options so it really doesn’t matter what you’d do.

Isn’t a Interest-only Homeowners Line of Credit much cheaper where one can pay the interest from LoC itself? Or, am I missing something here?

Hi Qamar. I’m a mortgage broker. Yes a homeowner’s line of credit could be 1.5 to 2% cheaper. However a client has to qualify for it. And it’s much tougher to qualify with all the new rules.

Many seniors with a pension may only qualify for a very small line of credit, even though the home could be worth a million dollars. With a reverse product, they could get hundreds of thousands of dollars if they wish.

One good advantage of a reverse mortgage is there are no payments to make ever. If you want to pay the monthly interest, you still can.

Secondly, a line of credit can be called at any time by the bank. For example, a client went to her bank of many decades (the Big Blue one) to notify them her husband passed away. Bank immediately called her $80,000 home line of credit on a $1,000,000 home. This will never happen with a reverse mortgage. You keep it until you sell the home, pass away, or permanently move to a nursing home.

Another example. Imagine we dip into recession and home prices fall. The bank will call back many lines of credit. Imagine being 80 years old and forced to sell your home just because prices dropped. This also will never happen with reverse mortgage.

Long story short (or is it too late for that), there are many things to consider, other than just rate. There’s no one answer that fits everybody. Definitely speak to a mortgage broker who has ALL the options.

Sorry for any errors in the above message. I’m using voice to text. 😉

Steve makes several good points.

The only thing I’d add is that lines of credits are still often the best choice in my opinion if

a) you can qualify for one (which is much easier at some lenders than others)

b) you are not depleting all of your credit limit at once

and

c) your line of credit limit is small enough so you can refinance it into a reverse mortgage later if needed

I would not recommend that any senior with cash flow challenges get a HELOC for more than 30-40% of their home’s value.

And yes, Qamar. In some cases you can pay the interest from the LOC itself. However, I would not do that unless you do your banking from the LOC as well. There are certain banks that are more open to this than others. Talk to a broker for details.

Update: 12 days later, HomeEquity Bank has now matched some of Equitable’s rates: https://twitter.com/RateSpy/status/1110178276847296513