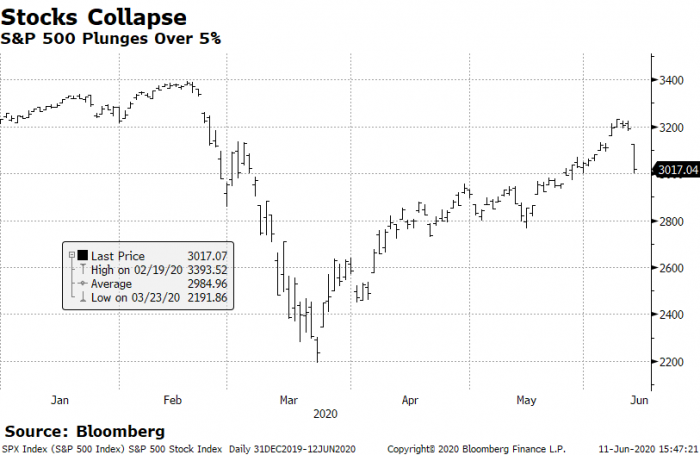

A Thursday Thumping: Fixed mortgage rates follow bond yields most of the time. Yet, despite stocks surging since March on recovery hopes, bonds have been arguably more realistic (less optimistic). Well, today stocks converged meaningfully with bonds…finally. The talking heads on TV say the Fed’s outlook and accelerating COVID cases scared the market and we’ve gone as high as we can go without more hope for a vaccine. The S&P 500 dove almost 6% as a result. Oil sank 9%. Meanwhile, Canadian 5-year yields are now once again just 10 itty bitty basis points away from their all-time lows. If we crack those lows, fixed rates will dip again, especially thanks to this next point.

Credit Spreads Have Largely Recuperated: The spike in the chart below shows how panicked investors got over Canada’s Big 6 Banks in March. It also shows how unpanicked they are now, despite banks announcing record loan loss provisions. This is glad tidings for mortgage shoppers. When this spreads drops, it typically coincides with wider profit margins for mortgage lenders. Wider margins mean banks can discount more—if they want to. Shrinking credit spreads and falling bond yields are usually a recipe for lower fixed mortgage rates. Last week, we saw 1.99% for the first time on bank-offered high-ratio5-year fixed rates. Given current margins, it’s possible we’ll see 1.99% on uninsured 5-year rates too. And with 4 out of 5 mortgages being conventional, 5-year 1.99% uninsured rates could really get borrowers’ juices flowing.

More Equity Releases This Fall: COVID-related income loss could “significantly” accelerate reverse mortgage adoption come September, says one lender. That wouldn’t be shocking, especially with reverse mortgage rates falling into the 3’s for the first time. The story…

Deferral Anxiety: With CMHC warning of a “deferral cliff” in the fall, it begs the question, how steep is the cliff? One in six mortgages are deferred and Bank of Canada staff say, “The effectiveness of the deferrals in limiting the rise in [mortgage defaults] depends crucially on the speed of the recovery in the labour market.” That could put us in a sticky spot come October, when the unemployment rate could be 68% (four percentage points) higher than it was in February, according to the latest Bloomberg economist survey. Some analysts suggest as many as 1 in 10 deferrers could default if the government doesn’t head this off at the pass. After all the money Ottawa has spent to avoid economic oblivion, we simply don’t see it letting expired deferrals take down the market. CMHC is preparing for this looming issue as we speak. Here’s to hoping employment roars back so we don’t rely so heavily on what they come up with.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Hoping this is but a blip in a so-far steady recovery. Fingers crossed the jobs keep coming back through to the fall and we can avoid this supposed “deferral cliff”!

Thursday was a big drop but let’s see what will the stock market bring today and next week. This kind of drop has happened more than once on Thursdays when the investors become scared of the unemployment numbers and I bet some automatic stop-loss orders contribute to it as well.

While I agree that the US stocks have become unreasonably expensive, a weaker US dollar, Fed’s dollar printing machine, jobs slowly coming back, and institutional investors not selling low will push it even higher in the short run. Of course, things could change rapidly after the US election, and/or as a second wave forces governments reverse the easing happening in quarantine and issue more stay at home orders.

Also don’t underestimate people/investors who made a lot of money during the strong come back since march. Another 20%-25% drop and they will start buying again, expecting a huge return in a year or two, and it will save the market from going down further

“investors become scared of the unemployment numbers”

The last unemployment reports north/south of the border exceeded the most optimistic forecasts. They are not a source of fear but a source of celebration.

That’s right. I didn’t mean only yesterday, but the whole trend in the last two to three months. Other things, mostly virus related news, have had their fair effect on the market as well. Anyways, today it looks like the decline is moving into today’s session.

Most people’s pensions (at least parts of it) is invested in the stock market so I am not sure if stock market sinking for a slight decrease in fixed mortgage rates is net positive for most people, specially the closer to retirement people with small to zero mortgages. Same with real estate.

“As of December 31, 2019, the CPP Investment Board manages over C$420 billion in investment assets for the Canada Pension Plan on behalf of 20 million Canadians.”

and

“The CPP Investment Board invests in private equity, public companies, and real estate.”

log in

log in

5 Comments

Hoping this is but a blip in a so-far steady recovery. Fingers crossed the jobs keep coming back through to the fall and we can avoid this supposed “deferral cliff”!

I’ve got to wonder if the bank vs. govt spread will inflate again when arrears start climbing.

Thursday was a big drop but let’s see what will the stock market bring today and next week. This kind of drop has happened more than once on Thursdays when the investors become scared of the unemployment numbers and I bet some automatic stop-loss orders contribute to it as well.

While I agree that the US stocks have become unreasonably expensive, a weaker US dollar, Fed’s dollar printing machine, jobs slowly coming back, and institutional investors not selling low will push it even higher in the short run. Of course, things could change rapidly after the US election, and/or as a second wave forces governments reverse the easing happening in quarantine and issue more stay at home orders.

Also don’t underestimate people/investors who made a lot of money during the strong come back since march. Another 20%-25% drop and they will start buying again, expecting a huge return in a year or two, and it will save the market from going down further

“investors become scared of the unemployment numbers”

The last unemployment reports north/south of the border exceeded the most optimistic forecasts. They are not a source of fear but a source of celebration.

That’s right. I didn’t mean only yesterday, but the whole trend in the last two to three months. Other things, mostly virus related news, have had their fair effect on the market as well. Anyways, today it looks like the decline is moving into today’s session.

Most people’s pensions (at least parts of it) is invested in the stock market so I am not sure if stock market sinking for a slight decrease in fixed mortgage rates is net positive for most people, specially the closer to retirement people with small to zero mortgages. Same with real estate.

From https://en.wikipedia.org/wiki/CPP_Investment_Board:

“As of December 31, 2019, the CPP Investment Board manages over C$420 billion in investment assets for the Canada Pension Plan on behalf of 20 million Canadians.”

and

“The CPP Investment Board invests in private equity, public companies, and real estate.”