Hitting Triples: Borrowers would love to see 5-year fixed rates under 2% and eventually they’ll get there. But for now, banks are “reducing mortgage rate discounts to conserve profitability,” as Deloitte put it in a recent report. Alas, we’ll have to make do with the historically low rates we already have. And for all you fixed-rate fans, the lowest fixed rate in Canada is now the triple-year (3-year) fixed at 2.09% or less. (Forgive the baseball reference. We miss MLB.) As is so often the case with the lowest rates, however, restrictions apply. This deal is available only to default-insured homebuyers or those with 35%+ down. If that matches your financing needs and you’re well-qualified and risk-tolerant, it’s worth a look. A 3-year fixed is more flexible than a longer term because it lets you refinance sooner (or discharge your mortgage sooner) with no prepayment penalty. The typical mortgagor renegotiates or discharges in roughly 3.7 years. And, for market bears who don’t think Canada will see above-target inflation in the next 33 months, a 3-year at 2.09% gives you Canada’s lowest fixed rate with no upside rate risk until mid-2023. At that time you can renew into any term you want, including a deep-discount variable, if they’re available by then (they should be). By the way, we say “33 months” because you can usually lock in great rates on your next term 90 days before your maturity date.

Five Years for 2.14%: HSBC’s default insured 5-year fixed at 2.14% remains RateSpy’s most-inquired-about rate for the second straight week. At just 5-6 bps more than the lowest fixed rate (noted above), it’s attracting a flood of interest. Several competing lenders could match this rate as profit margins support it. But, curiously, they’re not. Competitors apparently don’t believe they’ll lose enough business to HSBC’s leading discounts. Or perhaps they think people will pay extra to avoid HSBC’s potentially high big-bank-style prepayment charge.

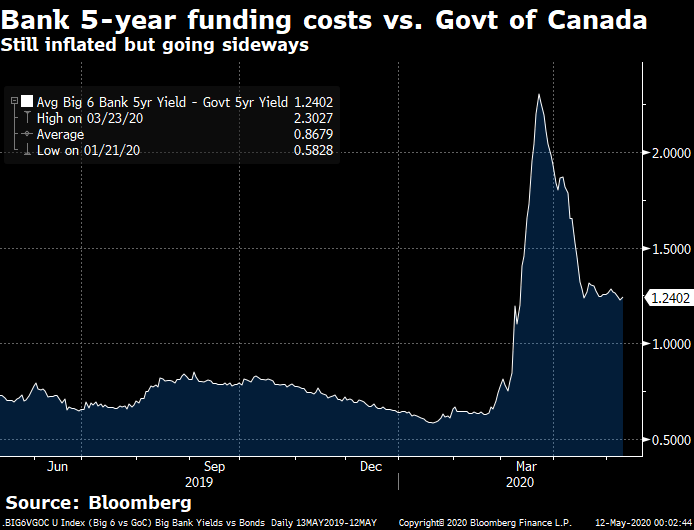

Banks Still Paying More: Big 6 Banks are still paying 35+ basis points more than normal to fund 5-year debt. That premium raises their “weighted average cost of funds,” which often leads banks to charge more for mortgages. Were funding costs more “normal” right now, we’d already be seeing 5-year fixed rates under 2%. To break that 2% floor, it’s likely that either:

base funding costs (as measured by bond yields or swap rates) must drop, or

the risk/liquidity premiums banks are forced to pay must drop. One or both could very well happen by the end of this year.

Forward Thinking: The market thinks 5-year rates will be higher in five years, about 40 bps higher based on 5-year forward contracts. These forward contracts essentially let traders bet on where rates will be in the future — in this case, in 2025. A few months ago, the market was pricing in no change in 5-year rates through 2025. BoC rate cuts and government relief measures changed that thinking mighty quick. Forwards are volatile instruments and not the most reliable mortgage selection tools, but they do provide an instructive reminder that rates can go up following economic downturns.

COVID Disloyalty: In a report this month, Deloitte says the coronavirus crisis is “likely” to encourage more switching of lenders “than ever before” as borrowers “face challenges getting banks to respond to their needs quickly and effectively.” Hence, not only will COVID cost unresponsive lenders mortgage originations today, but it’ll cost them renewals in the future.

Deferral Modelling: Another nugget in Deloitte’s report was that banks are analyzing which borrowers have requested mortgage deferrals. Banks’ purpose is understand commonalities in these customers and “capture the risk that is not inherent in [traditional] credit scoring models,” Deloitte explains. Banks will apply that knowledge in future underwriting decisions to manage their risk and adjust mortgage pricing. That means customers with a higher probability of requesting a mortgage deferral (those in higher-risk industries) might pay slightly higher mortgage rates.

CERB Kills Mortgage Approvals: Shady mortgage applicants underestimate lender due diligence. We heard from a broker this weekend about a mortgage applicant who told his lender he was working. The lender then noticed a $2,000 CERB deposit in the client’s bank account. It told the broker it was cancelling the mortgage approval since the client was either committing tax fraud or lying about their employment status. Mortgage applicants who get laid off, have their hours cut back or apply for government assistance before their mortgage closes should expect disappointment if they try to pull the wool over lenders’ eyes.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

I’m in a very time-sensitive dilemma: first time buyer, need to sign mortgage this week. So far secured an uninsured 30-yr mortgage (I’m putting down more than 20%) with 5-yr fixed at 2.49. With talk of sub-2% rates on the horizon, I am wondering if taking a 2-year term (at 2.49 or maybe lower like 2.39) then renewing is a good manoeuvre? In May 2022, do we anticipate rates to be higher, lower, same?

Hi Billy, Rate speculation is probably the least valid reason to choose one term over another, simply because it’s so easy to be wrong. 2.49% is a ***fantastic*** five-year fixed rate for a 30-year amortization. It’s mainly a question of whether that term is most suitable to your finances, mindset and five-year plan. For more see: https://www.ratespy.com/fixed-or-variable-rate-the-decision-checklist-02223752

Hi Grahame, Most credit unions have insufficient low-cost funding for prime mortgages and/or rely on a “relationship” or “community” lending model that entails higher advertised rates and more discretionary pricing. (Not our favourite approach in the digital age but that’s a story for later.)

Some of the more liquid mega-CUs are an exception. They can advertise quite competitive rates at times, and can negotiate them lower for well-qualified borrowers.

“That means customers with a higher probability of requesting a mortgage deferral (those in higher-risk industries) might pay slightly higher mortgage rates.”

It would be great if the opposite was true. If lenders recognized customers in low-risk industries with high (800+) credit scores and offered them slightly lower rates.

Hi Aaron, A minority of lenders do offer better pricing for high beacons, and it would be nice to see more such “super-prime” rates. But once you’re above a 720-760 FICO you’re usually going to get the best pricing (or near-best) anyway, assuming you’re qualified in other respects. The lender’s economics don’t improve a lot when it lends to a 800 FICO borrower versus a 760 FICO borrower.

Where the “low-risk industries” factor comes into play today is with approvals in general. Lenders are more prone to grant exceptions/approvals for borrowers who work in low-risk industries.

Hi David64, Rate forwards are instruments (interest rate derivatives) that banks and large corporations use to hedge future interest rate exposure or speculate on future rate direction. These investors are currently buying and selling such instruments at a price that implies the 5-year government bond rate will be ~ 4/10ths of a percentage point higher five years from now.

I will need to renew my mortgage in October. I will only have 2 years left. Am I eligible for that 3 yr fixed rate at 2.09% since I technically have above a 35% down payment due to equity in the house.

Hi Upforrenewalsoon, Contact the provider of that rate and they can give you the details. You may run into a problem because your amortization is too short (2 years) but ask them to confirm.

I just renewed my mortgage in February @ 2.49 five years fixed. I now have the opportunity to break that and jump into a variable @ prime-.75 with a $3000 Fee to move. Curious to know your thoughts

Hi Kris, You’ll want to run (or have a mortgage advisor run) an amortization scenario to see if it’s worthwhile. We can’t run the numbers on someone’s behalf but here’s a tool that people use to do it (use at your own risk): https://www.ratespy.com/amortization-schedule

Before reaching a conclusion, you’ll need to make certain assumptions (about future rates and refinance fees, for example). These assumptions must be taken into account in the amortization comparison of (A) doing nothing, versus (B) refinancing to a lower rate.

log in

log in

14 Comments

@Spy

Can you explain the “Forward thinking” comment above? I would like to understand the details behind that statement. Thanks

Hi David64, Happy to. What can I clarify specifically for you?

I’m in a very time-sensitive dilemma: first time buyer, need to sign mortgage this week. So far secured an uninsured 30-yr mortgage (I’m putting down more than 20%) with 5-yr fixed at 2.49. With talk of sub-2% rates on the horizon, I am wondering if taking a 2-year term (at 2.49 or maybe lower like 2.39) then renewing is a good manoeuvre? In May 2022, do we anticipate rates to be higher, lower, same?

Hi Billy, Rate speculation is probably the least valid reason to choose one term over another, simply because it’s so easy to be wrong. 2.49% is a ***fantastic*** five-year fixed rate for a 30-year amortization. It’s mainly a question of whether that term is most suitable to your finances, mindset and five-year plan. For more see: https://www.ratespy.com/fixed-or-variable-rate-the-decision-checklist-02223752

Hey Rate Spy, why do you think the credit unions are dragging their azz on giving the best rates?

Hi Grahame, Most credit unions have insufficient low-cost funding for prime mortgages and/or rely on a “relationship” or “community” lending model that entails higher advertised rates and more discretionary pricing. (Not our favourite approach in the digital age but that’s a story for later.)

Some of the more liquid mega-CUs are an exception. They can advertise quite competitive rates at times, and can negotiate them lower for well-qualified borrowers.

“That means customers with a higher probability of requesting a mortgage deferral (those in higher-risk industries) might pay slightly higher mortgage rates.”

It would be great if the opposite was true. If lenders recognized customers in low-risk industries with high (800+) credit scores and offered them slightly lower rates.

Hi Aaron, A minority of lenders do offer better pricing for high beacons, and it would be nice to see more such “super-prime” rates. But once you’re above a 720-760 FICO you’re usually going to get the best pricing (or near-best) anyway, assuming you’re qualified in other respects. The lender’s economics don’t improve a lot when it lends to a 800 FICO borrower versus a 760 FICO borrower.

Where the “low-risk industries” factor comes into play today is with approvals in general. Lenders are more prone to grant exceptions/approvals for borrowers who work in low-risk industries.

@Spy

Please clarify the part that it says the rates are expected to be 40 points higher in five years. Thanks

Hi David64, Rate forwards are instruments (interest rate derivatives) that banks and large corporations use to hedge future interest rate exposure or speculate on future rate direction. These investors are currently buying and selling such instruments at a price that implies the 5-year government bond rate will be ~ 4/10ths of a percentage point higher five years from now.

I will need to renew my mortgage in October. I will only have 2 years left. Am I eligible for that 3 yr fixed rate at 2.09% since I technically have above a 35% down payment due to equity in the house.

Hi Upforrenewalsoon, Contact the provider of that rate and they can give you the details. You may run into a problem because your amortization is too short (2 years) but ask them to confirm.

I just renewed my mortgage in February @ 2.49 five years fixed. I now have the opportunity to break that and jump into a variable @ prime-.75 with a $3000 Fee to move. Curious to know your thoughts

Hi Kris, You’ll want to run (or have a mortgage advisor run) an amortization scenario to see if it’s worthwhile. We can’t run the numbers on someone’s behalf but here’s a tool that people use to do it (use at your own risk): https://www.ratespy.com/amortization-schedule

Before reaching a conclusion, you’ll need to make certain assumptions (about future rates and refinance fees, for example). These assumptions must be taken into account in the amortization comparison of (A) doing nothing, versus (B) refinancing to a lower rate.