Payment Worries: 1 in 3 Canadians fear they’ll miss a rent or mortgage payment (Survey.) If you’re one of them, here’s an updated list of lender links for payment deferral info.

Appraisal Stop-gap: More lenders are announcing that they will accept “Modified Full Appraisals.” That’s where appraisers do virtual inspections of the property with the homeowner’s help, using tools like FaceTime, WhatsApp or Skype. Screenshots of those videos are then used in the appraisal report.

HSBC Hikes Most Rates: Online mortgage leader HSBC has lifted the following rates:

5yr fixed special (HR): 2.29% to 2.49%

10yr fixed special: 3.04% to 3.24%

5yr variable special (purchase/switch): 2.74% to 3.05%

5yr variable special (refi): 2.84% to 3.15% (prime + 0.20)

Quite the hefty increase. Fortunately, Tangerine still leads all HELOC rates at 2.85% (prime – 0.10%)

HSBC also tossed a cut in there, dropping its 2-year special from 2.64% to 2.54%.

Stubborn Spreads: Credit spreads in the mortgage market (i.e., how much more banks pay for funding than the federal government) keep increasing. That’s despite epic liquidity support from Ottawa and Washington. The spread between banks and government remains near crisis highs. That’s keeping the uptrend in mortgage rates alive.

Alberta Oil Woes: Today brought more devastation in WCS oil (Alberta’s oil price benchmark). It plunged to its lowest point on record, $6.45. Most producers are not profitable at roughly 3 times that number. Capital Economics’ Stephen Brown estimates the weighted average break-even point at somewhere near $17 a barrel on WCS crude. That’s for existing oil projects. New projects are much higher. If prices remain this depressed, it’ll erase an untold amount of jobs and business investment. You can bet your stimulus cheque that the Bank of Canada would weigh that heavily in its next rate decision.

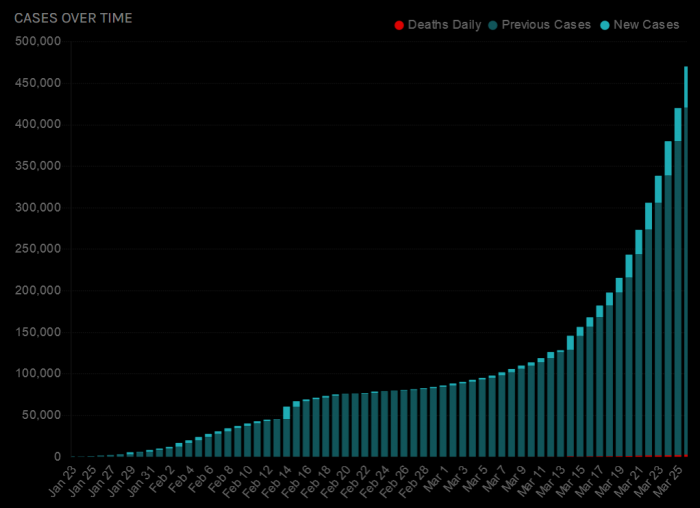

Going vertical: The latest COVID-19 chart from StatNews.

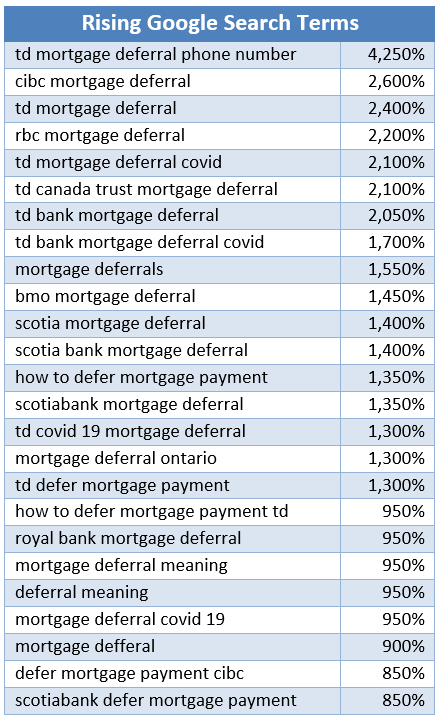

On People’s Minds: Here’s a look at the biggest increases in Google mortgage searches, as of yesterday. See any trends?

9:48 a.m. Update

Term Shift: The optimal mortgage term changes with the wind these days, and the wind has changed. Whereas variables were delectable at prime -1.20% or better just weeks ago, now not so much. With nationally available conventional 5-year fixed rates as low as 2.49% and the lowest variable at 2.59% (prime – 0.36%), the risk/reward of variables isn’t as compelling (see: sample scenario). That is, unless it takes the Bank of Canada 2+ years to gradually hike rates again. Mind you, this is based on hypothetical rate scenarios. There are many other fixed vs. variable factors to consider, including the lower potential penalty risk in a variable, the ability to lock in a variable later, etc.

TD Hikes: Big-bank pricing increases have been relentless. TD Canada Trust just raised the following special fixed rates:

The bank also removed its special 5-year variable rate of 2.95% and raised its posted 5yr variable from 3.10% to 3.15% (i.e., TD mortgage prime + .05% or actual prime + 0.20%).

Non-stop Liquidity: To ensure “stable funding” for mortgage lenders, the government said it’s now going to buy up to three times more insured mortgages from lenders, $150 billion vs. the previously planned $50 billion. CMHC also said it’s ready to “expand the issuance of Canada Mortgage Bonds.”

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

When can I apply for HELOC?

I bought property in dec 2019, and current market value of similar property is 50k+ more than my purchase price. I paid 20% downpayment and also have a PLOC of 50k, but the rate on my PLOC is too high, around 9%. So I was wondering, can I apply for HELOC now, to get a better rate? My current credit score is 650+. Thanks

Hey Marcus, You don’t need a mortgage with Tangerine to get a HELOC with them. If your home is free and clear, you can apply.

If you already have a mortgage with another lender, Tangerine would not be an option unless you moved your mortgage to Tangerine. In other words, Tangerine’s HELOC cannot go behind another lender’s first mortgage.

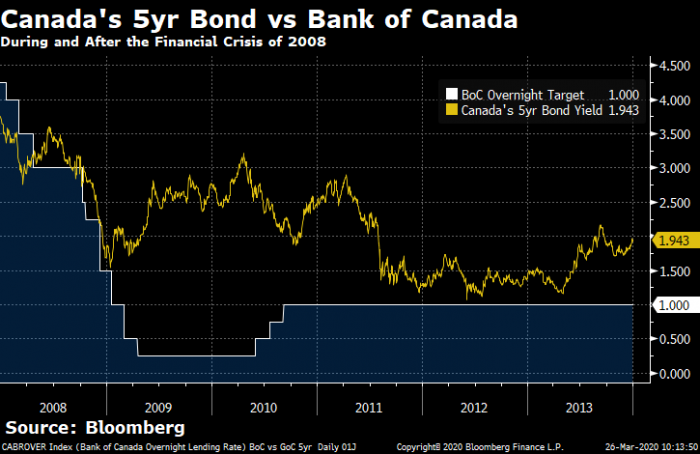

? how long does it take for a 5 year fixed mortgage rate to adjust to the 5 year canada bond yield?

The bond yield has been crushed and is at all time lows but the 5 year fixed rates have not moved down.

Am I right to assume that the 5 year fixed rate will follow with lower rates sometime over the next month?

Hi Brad, Normally 5yr fixed rates move with yields, with a lag that can range from 1-3 weeks. One exception is during crises where lenders are forced to pay risk/liquidity premiums to raise lending capital. That’s what we’ve been seeing lately. It’s impossible to know when the 5yr fixed / 5yr yield correlation will get back on track. It definitely will, but I’m not overly optimistic it’ll be sooner than later.

log in

log in

6 Comments

When can I apply for HELOC?

I bought property in dec 2019, and current market value of similar property is 50k+ more than my purchase price. I paid 20% downpayment and also have a PLOC of 50k, but the rate on my PLOC is too high, around 9%. So I was wondering, can I apply for HELOC now, to get a better rate? My current credit score is 650+. Thanks

Hi Jon, Best bet is to talk to a broker who can qualify you (i.e., assess your debt ratios, income, credit, etc.).

im looking to switch my heloc to tangerine but is it true that a 1st mortgage needs to be with tangerine to get the HELOC?

Hey Marcus, You don’t need a mortgage with Tangerine to get a HELOC with them. If your home is free and clear, you can apply.

If you already have a mortgage with another lender, Tangerine would not be an option unless you moved your mortgage to Tangerine. In other words, Tangerine’s HELOC cannot go behind another lender’s first mortgage.

? how long does it take for a 5 year fixed mortgage rate to adjust to the 5 year canada bond yield?

The bond yield has been crushed and is at all time lows but the 5 year fixed rates have not moved down.

Am I right to assume that the 5 year fixed rate will follow with lower rates sometime over the next month?

Hi Brad, Normally 5yr fixed rates move with yields, with a lag that can range from 1-3 weeks. One exception is during crises where lenders are forced to pay risk/liquidity premiums to raise lending capital. That’s what we’ve been seeing lately. It’s impossible to know when the 5yr fixed / 5yr yield correlation will get back on track. It definitely will, but I’m not overly optimistic it’ll be sooner than later.