Rate Conversions: Now Over-rated: Today’s best variable rates give borrowers a half-point head start versus a 5-year fixed. If one assumes the latest widely-held rate forecasts are correct (see below), prime – 0.35% or better variables still have a projected edge based on interest cost alone. And many are still willing to make that bet despite rate discounts being 50+ bps worse than in February. They’re doing so on the assumption they can lock into a fixed rate anytime. But while that optionality is theoretically valuable, this rate cycle is different. With Canada’s overnight rate near the zero bound, chances are small that anyone will lock their variable into a fixed rate that’s below their starting rate. That, on top of slippage costs (how much you lose when locking in due to your lender’s poor conversion rate) and the cost of bad timing (how much you lose because you locked in too late, which most do) makes any rate-lock strategy a poor reason to go variable in this climate.

Muted Rate Hikes: The Bank of Canada will hike just 1/2-point between now and the third quarter of 2022, according to the latest economist survey from Bloomberg. If rates theoretically rose double that estimate (i.e., 100 bps) and then held flat for the remainder of the next five years, here’s how today’s lowest nationally available conventional 5-year rates would fare against each other:

5-year fixed: 2.69%

5-year variable: 2.35% (prime – 0.10%)

Winner: 5-year fixed

One would save about $1,200 of interest per $100,000 of mortgage balance, assuming a 25-year amortization and a mortgage carried for the full 5-year term without changes.

Exception: If you’re able to save an extra 1/4-point on your variable rate, fixed and variable are a wash, given the above assumptions.

The takeaway: If you’re suited to a variable and can find one for better than prime – 0.35%, it’s an okay bet given that rates should stay reasonably low post-recession.

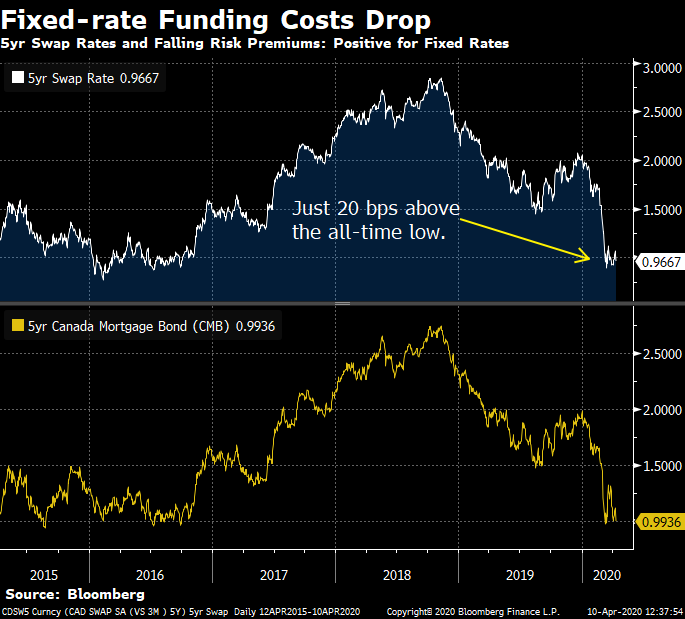

Room to Drop: This week we saw multiple big banks lower fixed rates. And there’s room for more. Until we get another flare-up in credit risk, the most competitive uninsured five-year fixed rates should move closer to the 5-year swap rate (a common benchmark for lender funding costs) plus ~150 bps. Someday we’ll get back to normal: 5-year swap plus 100 bps or so. For now, however, the trend implies we could see conventional 5-year fixed rates dip at least 20 more basis points (under 2.50%), if funding costs don’t shoot much higher. Few would have expected that a month ago. At the time, spooked investors were forcing banks to pay far more for their funding. Since then, the Bank of Canada, Finance Department and CMHC have committed to buying hundreds of billions in money market instruments, bonds and mortgage securities, putting a lid on rates.

Reverse Mortgage Records:Reverse mortgage provider Equitable Bank (EQB) is seeing record application volumes. It notes that, unlike its competitor HomeEquity Bank, “Our LTVs have not been reduced nor have we adjusted other adjudication standards.” Equitable now supports e-signing of all documents, accepts independent legal advice by video chat, is verifying ID remotely and is instructing appraisers to take pictures of interiors “through windows” with the borrower’s consent. The latter is due to the coronavirus limiting full appraisals.

Reverse Rates at Lows: “…We’ve never seen [reverse mortgage] rates this low,” says Equitable Bank VP of Prime and Reverse Mortgage Lending, Paul von Martels. “The differential between these rates and historical rates means an average borrower will save $40k+ in interest. More and more, reverse mortgage clients are researching their options and rate is often the first thing being compared.”

Largest GDP Drop Ever: That’s what the top economies will see this month, says the OECD. As for Canada, Capital Economics predicts “a 5.3% drop in GDP for 2020 as a whole.” It optimistically forecasts “GDP to rise strongly in 2021 and 2022, by 4.8% and 3.0%, respectively, but warns “that will not be enough to get the economy back to its pre-2020 trend.” Capital Economics suggests the Bank of Canada’s policy rate will “be firmly stuck at 0.25%” beyond 2022.

Ben Bernanke

Former Fed Chair Bernanke: “I don’t think it’s going to be a rapid [recovery]…We’ll probably have to restart activity fairly gradually and there may be subsequent periods of slower activity again…If anything, disinflation (low inflation) will be more of a concern in the next year than too high inflation.” Deflation is a serious threat.

e-Proof of Income: Job letters are a slow, hassle-prone means of proving income for a mortgage. CRA says it’s completed a “proof of concept” with financial institutions to send “proof of income” data directly to lenders. Were that system in place in this COVID-19 environment, it would considerably speed up the mortgage fulfillment process. For consumers’ sake, CRA should re-double its efforts on this project post-COVID.

Wise or Too Radical? Here’s one lender’s out of the box proposals on how to save Canadians billions in interest. Among his ideas, there’s some logic to freezing credit reporting for 12 months, although it would unduly give many a free-pass to ignore bills, to the detriment of creditors. On the idea of default-insuring refinances, that would lower refinance rates (both upfront and significantly on mid-term refinances for non-bank lenders). Insured refis would also improve access to refinancing before maturity at non-deposit taking lenders, which are essential bank competitors. Today, many non-bank lenders have limited ability to offer exceptional refi rates to people who break their mortgages early. The reason: they’re not able to securitize refis because the government stopped insuring them. Policymakers have already temporarily allowed refinances to be insured as part of their COVID measures. But only refinances that closed by March 20, 2020 qualify. We hear they may extend that date. As for eliminating the stress test, regulators have shown little desire to entertain that.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Thanks Andrew, The Mailchimp seems to have a mind of its own. Trying to time it better.

Unfortunately, every now and then stories are published after the cutoff time and notifications go out the next day.

So who does/doesn’t offer competitive conversion rates?

My experience with TD and BMO is that both offer competitive conversion rates. TD was 10-20bps higher than their discretionary rates for purchases, and BMO’s conversion rates were just as good as their discretionary rates for new clients.

For various reasons, not the least of which is variability, we can’t call out specific lenders on their conversion rates. But having been in the business for a decade plus, talked with countless mortgage servicing professionals and seen dozens of conversion offers, what I can say is that big banks and credit unions are hit or miss. There’s a lot of arbitrariness and no assurance like with fully transparent lenders who advertise deep discount rates online. Most lenders (not all) mark up their conversion rates 15-30+ basis points, as compared to their best rates for new originations.

If offered 2.84% by one of the top 6 banks for a 5 year fixed rate, it is logical to lock in now for an early June possession date, or to study the market if rates will still go lower? Pls advise.

Always best to lock in something as early as practical to protect against rates unexpectedly jumping.

As a general statement not specific to you, 2.84% is high — given the alternatives. Depending on loan-to-value, qualifications and other factors, one can find meaningfully lower 5yr fixed rates on the site.

Thank you Spy for this good post. It was the most helpful to me so far. It gave an idea on economy forecast, and for how long we may enjoy low prime rates, and how much we may expect them to rise year by year.

I feel lucky to have acquired a variable rate of prime-1.2% (1.25%!!) right before all the market fluctuation. Thank you for all the articles and updates you provide on this website. It has helped me to plan!

I am new in this world of mortgage. I see lower rates with less known but long time lenders. What are the pros and cons of work with them instead of the big banks?

I am checking with you frequently because I need to renew mine soon and appreciate your articles and any feedback you can give us.

That said, sometimes smaller lenders can’t compete depending on one’s needs. For example, larger banks dominate the readvanceable mortgage market, often have better refinancing options (which matters if you need to borrow more *before* maturity) and better portability. But not always. Hence why it’s so important to:

1. figure out what features you need based on your finances and 5-year plan

2. find the 2-3 lowest cost mortgages with those features and the service you need

3. ask the provider of each rate to compare its mortgage against the other(s) so you can make an informed decision.

Most importantly, remember that the lowest overall borrowing cost (including fees, penalties and costs you incur before maturity) always matters more than the lowest rate.

Thanks for the valuable information.

I have a mortgage up for renewal with TD and am having great difficulties completing the process since, I assume, all resources are focused on mortgage deferrals.

It’s hard to negotiate when nobody is available to talk.

I am thinking of going ahead with a 2 years fixed just to clear the storm.

Any pieces of advise?

If time is a factor, the first piece of advice would be to find a lender or broker that can meet your service expectations. There are lots of them out there. Closing is taking longer industry-wide but there’s no excuse for a lender not getting back to you. If for some reason you’re wed to TD, ping @TD_Canada on Twitter and tell them about the service problem you’re having. They should respond quickly.

I heard that banks might refinance only at 65 % of the home value, because they weren’t able to evaluate directly inside the house. Is it something that’s already implemented ? By every banks ? Even for low risk clients? It seems to be a bad move to fix the economy.

Some (but far from all) lenders have reduced the maximum they’re willing to lend, relative to the property value. That’s particularly true in high-risk regions like Alberta, or where the borrower has below-average qualifications. If you need the full 80% LTV on a refinance, any experienced broker can recommend multiple options.

Hi. I have a question,

I have a variable mortgage. Prime -.86% ( 4 years left). I have the option to lock it now, but I wonder if there’s room for prime mortgage rate to drop even more. What do think? Thanks,

Yolanda

Hey Bob, Could you get better? Yes — if you’re well qualified. But 2.77% is not bad, assuming it’s a 5yr fixed and that is the most suitable term for you (I wouldn’t know if it is).

Scotia has one of the most flexible big bank mortgages due to its refi, portability and early renewal policies. But like all big banks, it’s penalty policy is unfavourable if you break the mortgage early.

Also, depending on when in May, your closing date might not leave much time to apply elsewhere and close.

log in

log in

25 Comments

Light at the end of the tunnel! Thanks again and enjoy the ‘long’ weekend.

NB Any idea why the update emails arrive the day after posting?

Thanks Andrew, The Mailchimp seems to have a mind of its own. Trying to time it better.

Unfortunately, every now and then stories are published after the cutoff time and notifications go out the next day.

So who does/doesn’t offer competitive conversion rates?

My experience with TD and BMO is that both offer competitive conversion rates. TD was 10-20bps higher than their discretionary rates for purchases, and BMO’s conversion rates were just as good as their discretionary rates for new clients.

Hi Ralph,

For various reasons, not the least of which is variability, we can’t call out specific lenders on their conversion rates. But having been in the business for a decade plus, talked with countless mortgage servicing professionals and seen dozens of conversion offers, what I can say is that big banks and credit unions are hit or miss. There’s a lot of arbitrariness and no assurance like with fully transparent lenders who advertise deep discount rates online. Most lenders (not all) mark up their conversion rates 15-30+ basis points, as compared to their best rates for new originations.

If offered 2.84% by one of the top 6 banks for a 5 year fixed rate, it is logical to lock in now for an early June possession date, or to study the market if rates will still go lower? Pls advise.

KT,

Always best to lock in something as early as practical to protect against rates unexpectedly jumping.

As a general statement not specific to you, 2.84% is high — given the alternatives. Depending on loan-to-value, qualifications and other factors, one can find meaningfully lower 5yr fixed rates on the site.

Thank you Spy for this good post. It was the most helpful to me so far. It gave an idea on economy forecast, and for how long we may enjoy low prime rates, and how much we may expect them to rise year by year.

I feel lucky to have acquired a variable rate of prime-1.2% (1.25%!!) right before all the market fluctuation. Thank you for all the articles and updates you provide on this website. It has helped me to plan!

Great work, Reuben. Incredible rate.

Hi Spy,

I am new in this world of mortgage. I see lower rates with less known but long time lenders. What are the pros and cons of work with them instead of the big banks?

I am checking with you frequently because I need to renew mine soon and appreciate your articles and any feedback you can give us.

Hi Jose, Smaller lenders often yield better value. Their rates and penalties can be more favourable than big banks and there’s generally little risk to the borrower. More on that: https://www.theglobeandmail.com/real-estate/mortgages-and-rates/dont-fear-the-small-mortgage-lender/article4462402/

That said, sometimes smaller lenders can’t compete depending on one’s needs. For example, larger banks dominate the readvanceable mortgage market, often have better refinancing options (which matters if you need to borrow more *before* maturity) and better portability. But not always. Hence why it’s so important to:

1. figure out what features you need based on your finances and 5-year plan

2. find the 2-3 lowest cost mortgages with those features and the service you need

3. ask the provider of each rate to compare its mortgage against the other(s) so you can make an informed decision.

Most importantly, remember that the lowest overall borrowing cost (including fees, penalties and costs you incur before maturity) always matters more than the lowest rate.

Thanks for the valuable information.

I have a mortgage up for renewal with TD and am having great difficulties completing the process since, I assume, all resources are focused on mortgage deferrals.

It’s hard to negotiate when nobody is available to talk.

I am thinking of going ahead with a 2 years fixed just to clear the storm.

Any pieces of advise?

Hi ici.peb,

If time is a factor, the first piece of advice would be to find a lender or broker that can meet your service expectations. There are lots of them out there. Closing is taking longer industry-wide but there’s no excuse for a lender not getting back to you. If for some reason you’re wed to TD, ping @TD_Canada on Twitter and tell them about the service problem you’re having. They should respond quickly.

I heard that banks might refinance only at 65 % of the home value, because they weren’t able to evaluate directly inside the house. Is it something that’s already implemented ? By every banks ? Even for low risk clients? It seems to be a bad move to fix the economy.

Hi A,

Some (but far from all) lenders have reduced the maximum they’re willing to lend, relative to the property value. That’s particularly true in high-risk regions like Alberta, or where the borrower has below-average qualifications. If you need the full 80% LTV on a refinance, any experienced broker can recommend multiple options.

Hi all,

I have a question, need some help

– I am closing on my house early May and I have 2 options for mortgage

fixed at 2.49

variable at prime – 0.77 so currently 1.68.

what do you think is better need your help please

Hi Jake, For multiple reasons, we can’t make personalized term recommendations here. But both rates you’ve listed are excellent. Here’s more info that might help break the tie: https://www.ratespy.com/fixed-or-variable-rate-the-decision-checklist-02223752

Jake,

Looking at your 5 yr. Variable discount, you should go for 2.49 for 5 yr. Fixed. It will save you more in long run

Hi. I have a question,

I have a variable mortgage. Prime -.86% ( 4 years left). I have the option to lock it now, but I wonder if there’s room for prime mortgage rate to drop even more. What do think? Thanks,

Yolanda

Hi Yolanda,

Prime rate can drop more, but there’s a relatively small chance of that happening.

That alone doesn’t make it advisable to abandon such a great rate (1.59%). What would be your goal in locking in and what rate could you lock into?

I’d go with the prime – .77 myself. I can’t see rates rising more than one percent over five years with all the residual unemployment we’ll have.

Do you happen to know what RBC Mortgage Renewal rates are

Hi Doreen, They differ by borrower. RBC like most banks doesn’t offer the same renewal rates to every customer.

refi coming up in May with Scotia with equity (~57% LTV) being taking out for cottage purchase, have been given rate of 2.77%

Thoughts?

Hey Bob, Could you get better? Yes — if you’re well qualified. But 2.77% is not bad, assuming it’s a 5yr fixed and that is the most suitable term for you (I wouldn’t know if it is).

Scotia has one of the most flexible big bank mortgages due to its refi, portability and early renewal policies. But like all big banks, it’s penalty policy is unfavourable if you break the mortgage early.

Also, depending on when in May, your closing date might not leave much time to apply elsewhere and close.