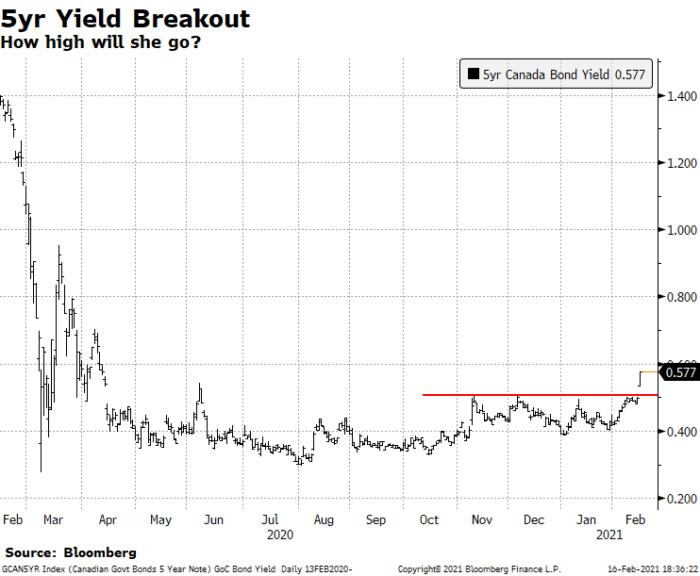

The entire mortgage market was waiting, and now, after 10 months, it finally happened. Canada’s 5-year bond yield (which influences fixed mortgage rates) broke through major resistance, resistance that goes all the way back to April of last year.

It’s a signal that better economic times lie ahead. A sign that inflation should no longer be just an afterthought. A sign that the lowest fixed rates in Canadian history are in danger of vanishing.

Bond yields are climbing because traders see the economy in a much better place in 2022, and because North American governments have deteriorating balance sheets and need to flood the market with their debt.

Those who brush aside the inflationary aspect of that last point should note that after the next round of U.S. stimulus, 40% of all dollars in circulation will have been printed in just the last 12 months. Money supply still matters.

An epic surge in fixed rates may not be in the cards, however. At least not according to analysts like John Stoltzfus, Chief Investment Strategist at Oppenheimer Asset Management. In a report released Wednesday, he wrote, “We expect that a process of reflation—rather than untoward levels of inflation—will see interest rates rise modestly…We also point out that…markets, as discount mechanisms pricing the future, can indeed get ahead of themselves.”

No doubt, a lot can go wrong with the inflationary / higher rate thesis in the coming quarters. For all anyone knows, the Bank of Canada could embark on yield-curve control and cap 5-year rates for months on end. Or perhaps a third virus wave will leave far deeper economic scars.

Either way, for now the risk of near-term fixed-rate hikes is legit. And that’s without even considering the potential for surging refinance volumes in the next 30-60 days as people rush to lock in.

In 2018, many paid over 3.50% for their mortgage, two points higher than they can get today.

A mini-refi boom would spike mortgage demand further, which in turn would boost demand for hedging through interest rate swaps, which (without getting too much in the weeds here) would further push up mortgage funding costs.

Given how integral oil is to Canada’s economy, it’s easy to understand why crude prices influence mortgage rates. That’s why a Bank of America report today caught our eye. It said, and I summarize: “While electric vehicles are unlikely to impact oil demand materially near term, they should trigger a global oil demand peak by around 2030.”

Other things equal and over time, that would be somewhat disinflationary and somewhat bearish for interest rates. “Over the next three years,” however, “we see a window of strong oil demand with consumption rising at the fastest pace since the 70s,” the bank said.

That’s all the more fuel for rising rates since higher oil prices often coincide with higher inflation.

How do you use this information to pick a mortgage? You probably can’t, at least not with reliability and precision. It’s simply the type of thing that adds one more (tiny) reason to go fixed for your next term and perhaps variable thereafter, particularly if long-term fixed rates shoot 100-125+ basis points above variable rates.

This & That

At 91%, Canada’s sales-to-new-listings ratio is almost unfathomable. Parabolic prices will coax homeowners to list their properties, particularly when lockdowns are in the rearview mirror. The question is, how high will prices run before that happens? Prepare for a whirlwind spring market.

CMHC has re-confirmed that “the new First-Time Home Buyer Incentive expansion should be available to apply to in the spring.”

“Given such low interest rates, some [HELOC] borrowers are relying on home equity appreciation to more than cover the interest cost of [their] additional debt. That may be fine over the short-term, but is a poor long-term plan.”—Rona Birenbaum, CFP (via the Globe & Mail)

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Hey Ralph, That’s particularly true with covered bonds. Most fixed-rate funding is geared off of Canadian yields, however, which are closely linked to U.S. yields. Not coincidentally, the U.S. is also undergoing a reflationary trend.

I paid a chunky pre-payment penalty to get out of my Scotia 3.29% mortgage early 2020 and was able to get an HSBC Prime – 1.11% (1.34%, open after 3 years) variable mortgage. I said then, never go fixed again.

But now, I’m having doubts. I can convert to fixed at 1.69% on a new 5 year term with HSBC. I don’t plan to move in the near future and can’t afford to (Van prices), but the flexibility of the variable is very appealing and the large penalty is still fresh on my mind.

The economic rebound and likely inflationary pressure are what has brought me to this point. Do we really think prime rate won’t be increased until late 2022 or 2023? And then of course, what will the variable/fixed rates look like then?

Spy, and community, what are your thoughts? Thanks.

Hey Jim, If you qualify, you can find lenders with fair penalties and 5yr fixed rates as low as 1.59% (non-default insured) on this site. It’s likely that if someone broke early with these lenders, they’d pay just a 3-month interest charge.

As for prime rate, the market expects the first hike in mid 2022, despite BoC messaging that 2023 is more likely. If we get 2+ hikes in either mid-2022 or mid-2023, it is extremely likely that a 5yr fixed at 1.59% would beat a 1.34% variable (based on interest cost alone).

Speaking of 10 year rates, are they required to pass the stress test? They won’t be up for renewal in 5 years, seems wrong that they have same bar to jump as 5 year mortgages.

I am in the process of switching my mortgage to Tangerine for a 10 year rate @ 2.04%, I have been keeping a close eye on the US treasury bonds as well as the Canadian treasury bonds. For me having a known rate is worth paying a small premium right now. We will see how the rates look in 2026-2031.

Hey Luis, I’ve never been a big 10yr fan but if there were ever a time to lock in for a decade, now may be it. But I’d never remotely consider it if the lender didn’t have fair penalties, which Tangerine does.

Yes, I find tangerine has many good things on their mortgages, the only down side for some people may be the use of collateral charges but in my case I also took the opportunity to get a HELOC for a rainy day or to finance big purchases. So that works for me!!!

I have less than 2 yr left on my mortgage (5yr variable) but need to refinance and current lender only offering a 5yr fixed @ 1.60%

Should I lock in or switch lender (pay 3 mths interest penalty) and go 5yr variable @ 1.39 % or other option 2 yr fixed @ 1.59 % fixed

Your thoughts

Thanks

Bob

log in

log in

13 Comments

I bet 10 year rates at 1.98% are going to look REALLY good in 6 months.

It’s a global market. Canadian banks in recent years have been tapping the European market for cheap money. Even when inflation gets over 2% in Canada, any significant upward movement in yields will be heavily influenced by foreign markets.

https://www.pfandbrief.market/en/covered-bond-market-review-and-outlook-for-2020/

Hey Ralph, That’s particularly true with covered bonds. Most fixed-rate funding is geared off of Canadian yields, however, which are closely linked to U.S. yields. Not coincidentally, the U.S. is also undergoing a reflationary trend.

I paid a chunky pre-payment penalty to get out of my Scotia 3.29% mortgage early 2020 and was able to get an HSBC Prime – 1.11% (1.34%, open after 3 years) variable mortgage. I said then, never go fixed again.

But now, I’m having doubts. I can convert to fixed at 1.69% on a new 5 year term with HSBC. I don’t plan to move in the near future and can’t afford to (Van prices), but the flexibility of the variable is very appealing and the large penalty is still fresh on my mind.

The economic rebound and likely inflationary pressure are what has brought me to this point. Do we really think prime rate won’t be increased until late 2022 or 2023? And then of course, what will the variable/fixed rates look like then?

Spy, and community, what are your thoughts? Thanks.

Hey Jim, If you qualify, you can find lenders with fair penalties and 5yr fixed rates as low as 1.59% (non-default insured) on this site. It’s likely that if someone broke early with these lenders, they’d pay just a 3-month interest charge.

As for prime rate, the market expects the first hike in mid 2022, despite BoC messaging that 2023 is more likely. If we get 2+ hikes in either mid-2022 or mid-2023, it is extremely likely that a 5yr fixed at 1.59% would beat a 1.34% variable (based on interest cost alone).

Speaking of 10 year rates, are they required to pass the stress test? They won’t be up for renewal in 5 years, seems wrong that they have same bar to jump as 5 year mortgages.

Hey Scott, You’re preaching to the choir my friend. The answer is yes, 10yr terms are stress tested just like 5yr terms.

I am in the process of switching my mortgage to Tangerine for a 10 year rate @ 2.04%, I have been keeping a close eye on the US treasury bonds as well as the Canadian treasury bonds. For me having a known rate is worth paying a small premium right now. We will see how the rates look in 2026-2031.

Hey Luis, I’ve never been a big 10yr fan but if there were ever a time to lock in for a decade, now may be it. But I’d never remotely consider it if the lender didn’t have fair penalties, which Tangerine does.

Yes, I find tangerine has many good things on their mortgages, the only down side for some people may be the use of collateral charges but in my case I also took the opportunity to get a HELOC for a rainy day or to finance big purchases. So that works for me!!!

Yep, and a collateral charge is less of an issue on a long 10-year term.

Thanks Spy. Having switched mortgage providers less than a year ago, I don’t want to do that again now and pay the various costs associated with that.

So for me it’s one of two options with HSBC. Thanks for the comments re expected rate hikes. Still deciding!

I have less than 2 yr left on my mortgage (5yr variable) but need to refinance and current lender only offering a 5yr fixed @ 1.60%

Should I lock in or switch lender (pay 3 mths interest penalty) and go 5yr variable @ 1.39 % or other option 2 yr fixed @ 1.59 % fixed

Your thoughts

Thanks

Bob