Variable Advantage Fades: The lowest widely available 5-year fixed rates are now just 20 basis points more than the lowest variable rates. That differential has shrunk considerably in the last month or so, causing some would-be variable takers to give up and go fixed. RateSpy simulations confirm it would now only take two 1/4-point rate hikes anytime in the next three years for the lowest 5-year fixed rates to outperform variables, other things equal. That’s based on interest cost alone and assumes standard terms with no changes to the mortgage for five years. That said, there are other fixed / variable factors to consider.

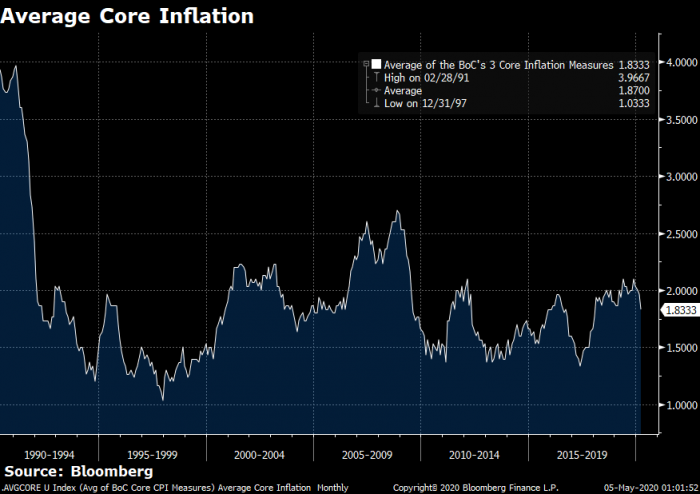

Deflation Threat: Average core inflation in Canada has never dipped below 1.40% this millennium. But it could—potentially before the end of this year as collapsing demand causes disinflation (or, God forbid, deflation). “I worry the economic structure gets damaged…(that) there is scarring, businesses get shut, people are unemployed, you can’t go back to where you left off,” says the IMF’s Tobias Adrian. If core inflation risks undershooting the BoC’s 1% minimum, incoming BoC Governor Tiff Macklem may be forced to cut rates again to get Canada back to its 2% CPI target. The danger of deflation, which can trigger vicious downward economic spirals, can’t be overstated. Is this possibility reason enough to choose a variable rate? Absolutely not. But it’s not exactly a harbinger of soaring rates either.

False Analogue: “…Comparisons to the deflation seen in the Great Depression are not helpful,” says the BoC’s Carolyn Wilkins. “For one thing, the banking sector is in much better shape than it was at that time. For another, we will not make the same policy errors,” she promises.

BMO Cuts Fixed Rates:Big bank mortgage rates continue to fall. The nation’s 4th largest bank lowered two special fixed rates on Monday:

3yr fixed: 2.99% to 2.89%

5yr ‘Smart’ Fixed (default insured): 2.99% to 2.79%

10% Drop from the Peak: That’s Moody’s prediction for home prices this year. “Not even lower interest rates will be enough to save the housing market,” said Moody’s economist Abhilasha Singh. (Especially with the stress test overinflated thanks to artificially high big bank 5-year posted rates. -ed.) “As the outlook begins to improve in early 2021, house prices are expected to rebound.”

Quotable: “We need to make it so that no Canadian relies on gains in housing wealth to feel secure…”—UBC professor, Paul Kershaw via Yahoo Finance. (Sounds good on paper, but imagine if retirement savers had to find a replacement for home appreciation. Now imagine it in a slowing economy with meagre savings rates, near-zero interest rates, less income/employment growth, higher taxes and fewer pensions. Not a pretty picture. -ed.)

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Hi Rate Spy. I have a fixed rate at 2.39% that come up for renewal in June. I can renew now at 2.52%for 5 years. We have no plans to move in less than 5 years. Should I wait or lock in now? The value is 300K.

Hi Diana,

What is the best rate that matches your criteria here (be sure to complete all fields) –> https://www.ratespy.com/best-mortgage-rates/5-year/fixed ?

Are you completely happy with your existing lender’s mortgage features/limitations, service and advice? (What lender is it?)

Are you sure a 5-year fixed is ideal for you?

Any chance you’ll need to borrow more money in 5 years?

These are just a few of the questions you need to ask before deciding.

I agree that a replacement for home appreciation might be a tough one.

Individuals need forced savings, taxed-at-source pensions, RRSP’s, Tax-free savings accounts and other incentives, otherwise most will save too little for retirement.

A paid-off house has been one of those assets that many people eventually acquired over time. It has heretofore been an entirely tax-free savings account that managed to keep pace with inflation.

The historical idea for many boomers was to sell the family home and down-size in retirement to a cheaper place or a rental, to live off of the cash from the house, plus perhaps a pension or two, plus OAS and CPP. The Canadian dream of dignity in old age.

But housing has greatly increased in price in many areas of Canada over the past 20+ years. And these long-time homeowners don’t deserve the financial windfall. I get it.

Incentivizing other assets besides principle residences might make perfect sense. But what else is there?

Perhaps even taxing the proceeds from the sale of a principle residence by a modest sum also makes perfect sense.

It will tend to push some capital around elsewhere. Increases to the current TFSA and RRSP limits could make up for some of the tax-free slack?

But, left to our own will and desire, most people are poor savers.

Thanks Appraiser, You raise multiple discussion-worthy points. One that can’t be overemphasized is the significance of forced saving. People have to make their mortgage payments. They don’t have to invest in a TFSA or RRSP. They should, but generally no one will put them on the street before retirement if they don’t.

That’s why, given Canada’s economic realities (slowing long-term growth, rising non-mortgage debt, lagging wage growth, etc.), idealistic soundbites may not address realities. Making principal payments each month is the only reliable form of self-preservation for millions of families. That’s the reality.

If we could magically drive down the cost of new homes people would certainly have more discretionary income to invest in their RRSPs/TFSAs. But price appreciation that fails to keep up with inflation has a slew of other economic side effects, over and above the negative wealth effects from lost equity.

It’s a catch 22 in so many ways. The country seems irreversibly dependent on rising home prices, largely because there are so few economic substitutes. Ottawa can tweak the incentives but there are much bigger macro and human psychology forces that will decide the outcome. These forces ensure that people will continue relying on home appreciation for years to come. That’s not without risk, of course. We all know what would happen if the bear finally comes out of hibernation.

Hi Rate Spy. I will be moving into a new home in Aug 20. I am looking for conventional mortgage. Shall I go for Conventional or high ratio because of lower interest rates. Or wait till next BOC meeting.

Hi Vijay, If you don’t already have a default insured mortgage, generally it doesn’t make sense to pay the insurance premium to get a lower insured rate. There have been exceptions to this in the past, but they’re rare. A broker can confirm in your particular case.

Hi,

My mortgage is up for renewal mid-July. I’ve had some decent offers to renew right now, but it seems like rates are still dropping as risk premiums are reduced. Does it make sense to wait until June to renew? Everything I see makes me think rates (both fixed and variable) will either stay the same or drop over the next weeks/months. Thanks!

Hey Alan, Statistically there’s easily better than a 50% chance that rates stay the same or drop in the next 30 days. And that’s unrelated to Covid. It just historical probability. But keep an eye on bond yields (https://www.ratespy.com/5-year-canada-bond-yield). A close above 0.60% on the 5yr yield could potentially lift fixed rates a notch at some lenders.

Hi Diana, Great negotiating. 2.29% is fantastic for a big bank 5yr fixed, if that’s the most suitable term for you. Just know that big bank penalties can sting if the mortgage is broken early. Moreover, collateral charges can sometimes make it more expensive to switch lenders at maturity. So, theoretically if you wanted a better product and/or rate, and you could get someone else to pay your refi costs, it might make sense to switch. But there are no 2.29% uninsured 5yr fixed options right now in the open market.

@Mojo

1.45% is a very good variable rate. Currently the best variable rate is Prime-0.5%, and I think that was referred to by some people and in this article as a not too sweet deal.

Mr. SPY,

I have a question: considering uncertainties in unemployment, inflation, economy and importance of housing market for Canada economy, do you think we will see some ease on stress test? When?

Hey David64, It’s highly probable that the minimum stress test rate will improve eventually. The government said it would and noted that it was only “suspending the coming into force of the new Benchmark Rate…”

It’s mainly a question of when and I’d only be speculating to guess. Hopefully by next year.

HI Ratespy, I have a preapproved rate of 2.39 5 years fixed for mortgage of 550,000 CAD. Is that the best rate i could get or should i explore more options in Fixed/Variable rates. It sounds like Fixed rate options are better now. I like the bank that offers this rate and i dont have other expectations. I am looking for a normal mortgage for next 5 years

Hi Vanthiya, Naturally it’s hard to say what’s most suitable for you without knowing a lot more about you. But 2.39% is a fantastic 5yr fixed rate if it’s an uninsured mortgage with features that match your 5-year plan. If you’re well qualified and putting down less than 20% or 25%+, you can find even better deals, based on rate alone: https://www.ratespy.com/best-mortgage-rates/5-year/fixed

But read the fine print as rate is just one element of overall borrowing cost.

I’m getting offered 2.59 5yr fixed from RBC. Should I lock in or wait? I plan on going with RBC, so I’m just wondering if rates will continue to drop. I need to decide by June 20th.

Hey Joel, Virtually no one knows what RBC (specifically) will do with rates between now and June 20. The best one can do is keep reading the rate news and monitoring the 5yr yield (https://www.ratespy.com/5-year-canada-bond-yield). You want to see it stay below 0.60%. Of course, nothing prevents RBC from hiking anyway but it’s a lower probability that they will if yields stay flat or fall.

Hi Ratespy, I have 3 offers:

1.88 for 3 yr fixed vs

2.19 for 5 yr fixed vs

1.82 for 5 yr var.

with 25 yr amortization.

I am inclined towards the 3 yr fixed since I pay 5k less interest and pay down extra 2k towards the principal at the end of three years as against corresponding numbers for 2.19 5 yr fixed at end of third year.

But my better half argues that rates will be lot higher to nullify that at end of 3 yr.

Have to decide in a day or two.

In your opinion, how should we choose?

It’s nice to have such good options. Can’t say what’s most suitable for you given the limited info but here’s what I can say:

Most well-qualified risk-tolerant borrowers would look at it this way. The break-even rate in three years is about 2.70%. Odds are, variable discounts will be back by then and a 1.88% three-year borrower could then renew into a prime – 1% variable and still be ahead (i.e., have a lower total interest cost). That break-even rate implies 125 basis points of BoC rate tightening (i.e., a 3.70% prime rate) in three years, which is not an unfair assumption.

This is a long way of saying, the 1.88% is a reasonable bet. And that doesn’t even factor in the 3-year’s penalty advantage, the historical edge of shorter terms, a potential long-term disinflationary outlook, etc.

If the rate you’d renew into in three years were greater than the break-even rate, the longer term (a 5yr fixed in this case) would result in less interest expense.

* Again, this is not a comment on suitability but rather a comment on the hypothetical interest cost, using standard assumptions and assuming no changes to the mortgage during the term. *

RateSpy your a great resource in this online universe! 🙂 I would like to hear feedback on my option to renew(by next week): 2.39/5yr fixed or take a P-.8 5yr var w/option to lock-into fixed if I want…btw I’ m leaning towards the var as I can sleep at night,lol

Hi Gio, If one assumes that (A) these are the only two options, (B) the products are standard without crazy fine print and (C) the borrower has no unique requirements for flexibility and is well qualified, risk tolerant and financially secure, then the 74 bps edge of the variable is compelling.

That’s so mainly given the upfront variable rate advantage and penalty advantage, and less so given historical research, the dim economic forecast and the rate lock option. (Rate lock options are mainly relevant if the lender is highly competitive with transparent low rates, and the borrower could foreseeably need to lock in.). But keep in mind that much will depend on the borrower’s 5-year plan and the contractual terms of each mortgage product.

And anyone getting a variable today must be mentally prepared for the *possibility* of at least 50-75 bps of rate increases in 18-36 months.

I currently have a variable mortgage coming up for renewal with RBC on July 1st. My current rate is 1.75%, $180,000 left to pay. I’ve been offered 2.3% variable for five years or 2.74% fixed 5 years. Do I wait till June for a better rate? Take the variable rate and if rates rise change to fixed to lock in the rate? Go ahead with the 5 year fixed and not worry about it?

Hi Fab, Please see my prior responses today (Sunday) that touch on choosing between fixed vs. variable. In your case, if you’re well qualified, those are both poor rates. Would suggest shopping a bit more as you may find find materially better savings elsewhere. As for waiting, there’s a chance both fixed and variable rates improve by June but if the 5-year government bond yield closes above 0.60% I’d lock something in immediately. And give yourself at least 40 days to close if you want to switch lenders.

log in

log in

48 Comments

Hi Rate Spy. I have a fixed rate at 2.39% that come up for renewal in June. I can renew now at 2.52%for 5 years. We have no plans to move in less than 5 years. Should I wait or lock in now? The value is 300K.

Hi Diana,

What is the best rate that matches your criteria here (be sure to complete all fields) –> https://www.ratespy.com/best-mortgage-rates/5-year/fixed ?

Are you completely happy with your existing lender’s mortgage features/limitations, service and advice? (What lender is it?)

Are you sure a 5-year fixed is ideal for you?

Any chance you’ll need to borrow more money in 5 years?

These are just a few of the questions you need to ask before deciding.

Great blog Spy.

I agree that a replacement for home appreciation might be a tough one.

Individuals need forced savings, taxed-at-source pensions, RRSP’s, Tax-free savings accounts and other incentives, otherwise most will save too little for retirement.

A paid-off house has been one of those assets that many people eventually acquired over time. It has heretofore been an entirely tax-free savings account that managed to keep pace with inflation.

The historical idea for many boomers was to sell the family home and down-size in retirement to a cheaper place or a rental, to live off of the cash from the house, plus perhaps a pension or two, plus OAS and CPP. The Canadian dream of dignity in old age.

But housing has greatly increased in price in many areas of Canada over the past 20+ years. And these long-time homeowners don’t deserve the financial windfall. I get it.

Incentivizing other assets besides principle residences might make perfect sense. But what else is there?

Perhaps even taxing the proceeds from the sale of a principle residence by a modest sum also makes perfect sense.

It will tend to push some capital around elsewhere. Increases to the current TFSA and RRSP limits could make up for some of the tax-free slack?

But, left to our own will and desire, most people are poor savers.

Thanks Appraiser, You raise multiple discussion-worthy points. One that can’t be overemphasized is the significance of forced saving. People have to make their mortgage payments. They don’t have to invest in a TFSA or RRSP. They should, but generally no one will put them on the street before retirement if they don’t.

That’s why, given Canada’s economic realities (slowing long-term growth, rising non-mortgage debt, lagging wage growth, etc.), idealistic soundbites may not address realities. Making principal payments each month is the only reliable form of self-preservation for millions of families. That’s the reality.

If we could magically drive down the cost of new homes people would certainly have more discretionary income to invest in their RRSPs/TFSAs. But price appreciation that fails to keep up with inflation has a slew of other economic side effects, over and above the negative wealth effects from lost equity.

It’s a catch 22 in so many ways. The country seems irreversibly dependent on rising home prices, largely because there are so few economic substitutes. Ottawa can tweak the incentives but there are much bigger macro and human psychology forces that will decide the outcome. These forces ensure that people will continue relying on home appreciation for years to come. That’s not without risk, of course. We all know what would happen if the bear finally comes out of hibernation.

@ Dianna

Who is offering that 5yr/2.52%

@ The Spy

Did you attach the wrong link, I don’t see any fields to fill in, unless it’s just mine that’s not opening up properly.

Hi Rob, These are the fields I’m referring to: http://prntscr.com/sbggf9

If you can’t see them on this page let us know: https://www.ratespy.com/best-mortgage-rates/5-year/fixed

If you’re on mobile, look for the “Filter Options” link on the top left of the page (under the RateSpy logo).

What happens in a deflationary economic environment exactly? Nothing good, I’m assuming.

Hey Jessie, A whole lotta bad. Here’s a short primer on deflation from the BoC: https://www.bankofcanada.ca/wp-content/uploads/2010/11/disinflation_deflation.pdf

Hi Rate Spy. I will be moving into a new home in Aug 20. I am looking for conventional mortgage. Shall I go for Conventional or high ratio because of lower interest rates. Or wait till next BOC meeting.

Hi Vijay, If you don’t already have a default insured mortgage, generally it doesn’t make sense to pay the insurance premium to get a lower insured rate. There have been exceptions to this in the past, but they’re rare. A broker can confirm in your particular case.

As for waiting to apply, there’s risk to waiting. But, so long as 5-year bond yields (https://www.ratespy.com/5-year-canada-bond-yield) don’t surge above 0.60% that risk is muted.

Hi,

My mortgage is up for renewal mid-July. I’ve had some decent offers to renew right now, but it seems like rates are still dropping as risk premiums are reduced. Does it make sense to wait until June to renew? Everything I see makes me think rates (both fixed and variable) will either stay the same or drop over the next weeks/months. Thanks!

Hey Alan, Statistically there’s easily better than a 50% chance that rates stay the same or drop in the next 30 days. And that’s unrelated to Covid. It just historical probability. But keep an eye on bond yields (https://www.ratespy.com/5-year-canada-bond-yield). A close above 0.60% on the 5yr yield could potentially lift fixed rates a notch at some lenders.

@rate spy it was TD and I went back to them and said I was shopping and the rate magically dropped to 2.29%! What to do now?

Hi Diana, Great negotiating. 2.29% is fantastic for a big bank 5yr fixed, if that’s the most suitable term for you. Just know that big bank penalties can sting if the mortgage is broken early. Moreover, collateral charges can sometimes make it more expensive to switch lenders at maturity. So, theoretically if you wanted a better product and/or rate, and you could get someone else to pay your refi costs, it might make sense to switch. But there are no 2.29% uninsured 5yr fixed options right now in the open market.

@Diana

2.29% looks like a good rate. Is it possible to lock it, and still continue to shop around for a better rate?

@Diana Wow! 2.29 for 5 year fixed?

I just renewed for 1.45% prime -1 variable 5 years. What do yout hink considering you mentioned stay away from variable at this time?

Mojo, Some variables are much better than others. P-1.45% is tremendous!

Thank you for the information and advice. I will see if that is possible.

@Mojo

1.45% is a very good variable rate. Currently the best variable rate is Prime-0.5%, and I think that was referred to by some people and in this article as a not too sweet deal.

Mojo

Who offered that rate?

Mr. SPY,

I have a question: considering uncertainties in unemployment, inflation, economy and importance of housing market for Canada economy, do you think we will see some ease on stress test? When?

Hey David64, It’s highly probable that the minimum stress test rate will improve eventually. The government said it would and noted that it was only “suspending the coming into force of the new Benchmark Rate…”

It’s mainly a question of when and I’d only be speculating to guess. Hopefully by next year.

HI Ratespy, I have a preapproved rate of 2.39 5 years fixed for mortgage of 550,000 CAD. Is that the best rate i could get or should i explore more options in Fixed/Variable rates. It sounds like Fixed rate options are better now. I like the bank that offers this rate and i dont have other expectations. I am looking for a normal mortgage for next 5 years

Hi Vanthiya, Naturally it’s hard to say what’s most suitable for you without knowing a lot more about you. But 2.39% is a fantastic 5yr fixed rate if it’s an uninsured mortgage with features that match your 5-year plan. If you’re well qualified and putting down less than 20% or 25%+, you can find even better deals, based on rate alone: https://www.ratespy.com/best-mortgage-rates/5-year/fixed

But read the fine print as rate is just one element of overall borrowing cost.

Mojo, who offered that rate and when?

I’m getting offered 2.59 5yr fixed from RBC. Should I lock in or wait? I plan on going with RBC, so I’m just wondering if rates will continue to drop. I need to decide by June 20th.

Thanks,

Joel

Hey Joel, Virtually no one knows what RBC (specifically) will do with rates between now and June 20. The best one can do is keep reading the rate news and monitoring the 5yr yield (https://www.ratespy.com/5-year-canada-bond-yield). You want to see it stay below 0.60%. Of course, nothing prevents RBC from hiking anyway but it’s a lower probability that they will if yields stay flat or fall.

Hi Ratespy, I have 3 offers:

1.88 for 3 yr fixed vs

2.19 for 5 yr fixed vs

1.82 for 5 yr var.

with 25 yr amortization.

I am inclined towards the 3 yr fixed since I pay 5k less interest and pay down extra 2k towards the principal at the end of three years as against corresponding numbers for 2.19 5 yr fixed at end of third year.

But my better half argues that rates will be lot higher to nullify that at end of 3 yr.

Have to decide in a day or two.

In your opinion, how should we choose?

Thanks in advance.

Hi Choosy,

It’s nice to have such good options. Can’t say what’s most suitable for you given the limited info but here’s what I can say:

Most well-qualified risk-tolerant borrowers would look at it this way. The break-even rate in three years is about 2.70%. Odds are, variable discounts will be back by then and a 1.88% three-year borrower could then renew into a prime – 1% variable and still be ahead (i.e., have a lower total interest cost). That break-even rate implies 125 basis points of BoC rate tightening (i.e., a 3.70% prime rate) in three years, which is not an unfair assumption.

This is a long way of saying, the 1.88% is a reasonable bet. And that doesn’t even factor in the 3-year’s penalty advantage, the historical edge of shorter terms, a potential long-term disinflationary outlook, etc.

Choosy, who offered those rates?

Esp. 1.88 fixed? Please connect me with your broker 🙂

I’m guessing it wasn’t a broker but by all means, it would be great to know the lender, Choosy. As well as how long ago you got this rate quote.

@ Vanthiya

Who gave you the fixed rate of 2.39%

Thx

Thanks RateSpy for your opinion. What is meant by break-even rate ?

If the rate you’d renew into in three years were greater than the break-even rate, the longer term (a 5yr fixed in this case) would result in less interest expense.

* Again, this is not a comment on suitability but rather a comment on the hypothetical interest cost, using standard assumptions and assuming no changes to the mortgage during the term. *

I connected with HSBC right before the shutdown started. They have the best rates.

HSBC is the best sometimes, not all the time.

HSBC doesn’t always have the lowest rate.

Who gives variable- 1 ??

@P

Among the big banks HSBC does have the best rate. among all lenders, not all the time as you said.

RateSpy your a great resource in this online universe! 🙂 I would like to hear feedback on my option to renew(by next week): 2.39/5yr fixed or take a P-.8 5yr var w/option to lock-into fixed if I want…btw I’ m leaning towards the var as I can sleep at night,lol

Hi Gio, If one assumes that (A) these are the only two options, (B) the products are standard without crazy fine print and (C) the borrower has no unique requirements for flexibility and is well qualified, risk tolerant and financially secure, then the 74 bps edge of the variable is compelling.

That’s so mainly given the upfront variable rate advantage and penalty advantage, and less so given historical research, the dim economic forecast and the rate lock option. (Rate lock options are mainly relevant if the lender is highly competitive with transparent low rates, and the borrower could foreseeably need to lock in.). But keep in mind that much will depend on the borrower’s 5-year plan and the contractual terms of each mortgage product.

And anyone getting a variable today must be mentally prepared for the *possibility* of at least 50-75 bps of rate increases in 18-36 months.

@Gio

Who is giving you the 2.39/5yr fixed rate

Thx

Tangerine renewal offer letter.

I currently have a variable mortgage coming up for renewal with RBC on July 1st. My current rate is 1.75%, $180,000 left to pay. I’ve been offered 2.3% variable for five years or 2.74% fixed 5 years. Do I wait till June for a better rate? Take the variable rate and if rates rise change to fixed to lock in the rate? Go ahead with the 5 year fixed and not worry about it?

Hi Fab, Please see my prior responses today (Sunday) that touch on choosing between fixed vs. variable. In your case, if you’re well qualified, those are both poor rates. Would suggest shopping a bit more as you may find find materially better savings elsewhere. As for waiting, there’s a chance both fixed and variable rates improve by June but if the 5-year government bond yield closes above 0.60% I’d lock something in immediately. And give yourself at least 40 days to close if you want to switch lenders.

Its coming from multiple banks Rob.

BMO,TD,CIBC

Choosy,

hi I just wanted to know who is your broker . Thanks