Big Drops from HSBC: The online mortgage juggernaut keeps shaking competitors’ trees. This time with Canada’s lowest bank-advertised 5-year fixed rate ever, according to our records. It’s also the first bank to crack the 2% barrier on a 5-fixed, albeit it’s for default-insured mortgages only. HSBC’s move not only reflects historically low funding costs, but its continued drive to brand itself as Canada’s most competitive lender. The likes of RBC, TD, Scotiabank, BMO and CIBC could easily undercut this rate if they wanted to, but they likely won’t near-term. Here’s more on this record-breaking rate and a look at what other rates HSBC trimmed:

Special fixed rates:

2yr: 2.34% to 2.04%

This is Canada’s lowest 2-year rate by a long shot. It’s a decent alternative if you’re waiting for better variable-rate discounts. The best part is that you can either:

A) Blend and extend into a 5-year fixed mortgage anytime without fees or penalties (in case you think rates will spike and you want to lock in). And you can do so at HSBC’s low, transparent website rates. Your new rate is a weighted average of your remaining 2-year rate and HSBC’s then-current 5-year rate.

B) Renew 120 days early at discounted rates with no fees/penalties.

One warning: HSBC has a big-bank-style—i.e., “potentially costly”—interest rate differential (IRD) charge. That penalty can apply if you break this mortgage early, depending on where rates are at the time. Keep that in mind if there’s any chance whatsoever that you’ll sell or refinance before 2025.

5yr: 2.44% to 2.29%

This is the lowest widely advertised conventional 5-year fixed rate in Canada. Scotiabank’s eHOME website is showing 2.27% for certain borrowers, but you have to create an eHOME account to see it.

We’re getting closer to prime – 1.00% every day. It’s coming. For now, this is Canada’s lowest rate for insured borrowers who want to float their mortgage.

5yr: 2.15% to 2.05% (prime – 0.40)

This is Canada’s lowest lender-advertised variable for conventional mortgages and refinances.

RBC cuts: Big blue lowered the following rates, but as usual actual big bank mortgage rates are much lower than advertised.

Special fixed rates:

3yr: 2.74% to 2.64%

4yr: 2.74% to 2.69%

5yr: 2.99% to 2.89%

7yr: 3.49% to 3.39%

Special variable rate:

5yr closed: 2.45% to 2.40% (prime – 0.05)

The only reason this sub-par rate is relevant is because it symbolizes improving floating-rate pricing. RBC hiked this rate to prime + 0.25% seven weeks ago. But now COVID-related funding pressures have eased and pricing is slowly getting back to normal.

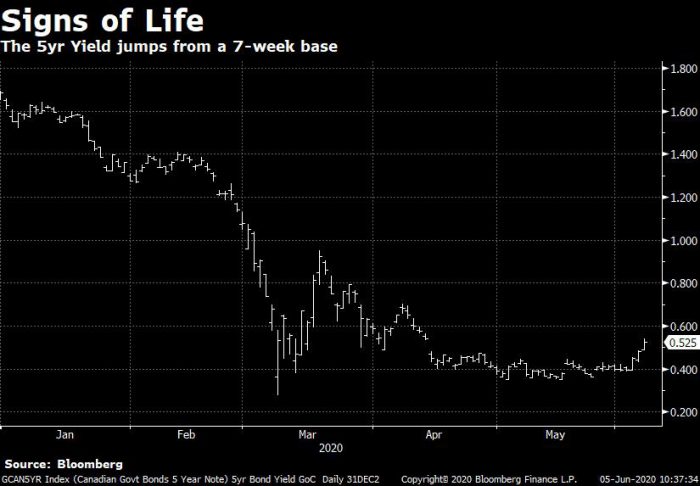

Bright Ray of Hope: Canada’s 5-year government yield is climbing on the back of surging economic optimism and a much stronger-than-expected jobs report. The market expected half a million lost jobs, but Canada posted an estimated 289,600 gain. U.S. employment gains vastly surpassed expectations as well. If this march higher in yields continues into the 0.60% or 0.70% range, we could see the lowest 5-year fixed rates jump at least 5 to 10 basis points. If this is a longer-term bottom for yields (which no one can predict but many will speculate on) then today’s 5-year rates in the low-2s are a bargain for people who must lock in.

Reality Check: “…It is still likely to take years for the labour market to fully heal,” says Capital Economics. Rates might lift off for weeks or months—along with recovering employment—but they’ll likely remain historically low longer-term.

Speaking of Locking In: CMHC says an overwhelming 96.6% of default-insured borrowers chose a fixed rate in the first quarter.

Posting Too High: Posted 5-year fixed rates are still massively inflated with the typical big-bank posted rate 100 bps above its long-term average, relative to bond yields. That matters for two reasons:

It keeps the minimum stress test rate artificially high, reducing the mortgage amount that otherwise-qualified borrowers can get

Some say that’s good in a riskier housing market. Others disagree, saying it’s a drag on the economy to shut out borrowers because of arbitrarily high interest rates.

It makes fixed-rate IRD penalties bigger if you break your mortgage early to sell or refinance

The reason: High posted rates create a falsely large “discount.” The top 10 banks use that discount from posted rates against you in their penalty formulas.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

We have about two and a half months left on our P – 0.65 variable and I’ve been watching the discounts for conventional mortgages sloooowly improve. A broker has offered P – 0.45 but I’m not feeling a rush to sign on it given the direction things are going. Hopefully, things continue in the same direction and we end up with a discount close to what we’ve already been enjoying!

Unfair IRD penalties based on artificially high posted rates are a scourge on society. Time to implement those previously proposed changes to calculate the stress test. Also time for The Dept. of Finance and / or OSFI to crack down on overly zealous IRD charges.

Hey Jeff, It’s so hard to say. Looking back at history, there’s often a violent spike up in bond yields to accompany a rapid change in inflation expectations. That marks the point where the rate trend changes from sideways to up. But it’s not always like that.

June 5 I just signed a refinance $300,000 30 year not insured mortgage 5 year fixed term at 2.39% with $1,200. cash back at HSBC. I also had to open a free chequing account at HSBC to get the cash back.

HSBC is great for owner-occupied properties, but not for rentals. The maximum LTV on rentals is 70%, while BMO and Scotia will do 80%. HSBC also has a rather unfavorable rental add-back formula for calculating TDS.

My mortgage term is due in two weeks. I am torn between fixed and variable. TD offer a fixed rate of 2.19 and variable of 1.95. Need help on this please.Thank you!

@Brent – If you wait until 30 days before renewal the discounts might be 0.1% better. Conventional variable rates seem to be permanently worse than high ratio rates and I don’t see that changing this summer.

@appraiser. So you want government to come in and solve your IRD problem. Hey I have a solution, a market solution. Choose another freaking lender!!! Spy talks about fair lenders all the time. If there is anything consistent with this broker based website (which is fantastic by the way), its the amount of sucking and blowing from the brokers, realtors, and commentators. Government please come in and solve my IRD problem. Oh, and don’t you dare tighten your insured underwriting policies even though you are taking on all the risk. suck. blow. suck. blow. rinse. repeat.

CMHC’s risk to taxpayers is the most exaggerated lie that housing bears perpetrate.

2) You could outlaw penalties tomorrow and all that would happen is the banks would rates rates and fees. Then EVERYONE with a mortgage would pay more instead of just people who break their mortgage contract. Careful what you wish for. Banks always win, one way or another.

We have a three year fixed term @ 2.39 that is coming due on September 01.

TD is offering us 2.10 for two years. I know the variable rate should be in the 1.6 % range because that is what a friend of mine is paying at the moment.

In 2009 when the Prime rate was this low I was on a variable rate down at 1.14. I know that there is room to come down for customers with history with their lender.

Requalifing with another lender involves a lot of legwork but might be worth it?

One might have to tell his lender if he goes to all in on the research with a competitor then he is going to go with them. What is their best offer?

They will not want to see your credit cards and investments cross the street.

Rates are going to go lower and it will take years for the economy to recover as it did after 2009. The bank of Canada might even reduce the rate another .25 over the next few months. It will be no quick recovery so raising them again in the next few three years or more is not going to happen.

13% unemployment with an economy that is going to go through a complete restructuring along with huge government debt is going to keep the BOC on the sidelines.

The CMHC is an outdated blood sucking entity. One which serves no purpose but to steal a good portion of hard working Canadians down payments.

I know a woman who was approved on her own at TD but was under the 20 % downpayment threshold. After CMHC stepped in she then had to first pay off her car, and then come up with a further $15,000 down payment in which they stole $12,000.

The banks can decide on their own who can qualify without CMHC. It is a bloated top heavy unnecessary leech with 1700 employees that transferred a annual dividend to the Federal government of $505 million in 2019.

$375 million in 2018.

How much less interest over time could average Canadians save on their mortgages with a larger down payment. Just another Tax and government created jobs. Sad .. Time for my antidepressants

@Broker – I agree with your analysis. We won’t get back to a “good” discount on conventional variables before our renewal in August, but I’m willing to wait and see. Cheers.

I just submitted docs last nite on my 2.49

30 yr fixed with 4500.00 back from previous lender.

Was that a smart move having to pay about 9 k in closing and fees?Previous was 3.75.

Hi my rate is 3.65 for 5 years and I have 3.8 years left I In my term and my bank giving me 2.14 for five years with the penalty 4200$ can any one give me any advice What I will do I really appreciate that.

Sultan, you need to provide more information for an exact calculation (at least the mortgage amount, amortization).

But, with a 1.51 rate difference, a 100K mortgage will cost you roughly 1500$ more each year. (A little bit less depending on amortization, and the amount of principal you are paying each month). That will be more than 5000$ in the next 3.5 years.

So, as a rule of thumb, if your mortgage amount is more than 100,000$ and you can afford the penalty now, it will probably be worth doing it.

But, man, they robbed you at 3.65 last year (I assume it was a 5 year mortgage). I would never bank with them if I were you 😀 If you are going to break it, you might as well take it some where else. Some offer better rates, and some offer cash backs that covers at least part of the penalty. Some offer both.

Another thing to consider is, if you are likely to break it again. If you are planning to up-size or down-size any time soon, it may not be worth breaking now for a 5 year fixed. You may want to go variable or stay put.

Thank you for ur reply M, I already calculate my numbers how much I’m going to save in my principal and how much I’ll pay the interest if I change my mortgage rate to 2.14 % . My question is is this a good time to do the renewal or should I wait one more month , and also I can’t go to other bank because of my wife’s job so I have to stick with my current bank ?

Sorry the 4200$ penalty and the rates you mentioned in your first comment confused me, as they have nothing to do with the question you are asking 😉

If you have done the math, you already know how many months of wait is worth waiting for every 10 bps drop in the rate. So, tell us, how much the rate should drop further for a 3 month wait to be worth it?

But if you are asking if the rates are expected to drop further, and if yes, when and by how much, I’ll leave that to the Spy to answer.

log in

log in

24 Comments

We have about two and a half months left on our P – 0.65 variable and I’ve been watching the discounts for conventional mortgages sloooowly improve. A broker has offered P – 0.45 but I’m not feeling a rush to sign on it given the direction things are going. Hopefully, things continue in the same direction and we end up with a discount close to what we’ve already been enjoying!

Unfair IRD penalties based on artificially high posted rates are a scourge on society. Time to implement those previously proposed changes to calculate the stress test. Also time for The Dept. of Finance and / or OSFI to crack down on overly zealous IRD charges.

I know it’s hard to tell but are there any clues that can help us know when rates bottom?

Thanks

Hey Jeff, It’s so hard to say. Looking back at history, there’s often a violent spike up in bond yields to accompany a rapid change in inflation expectations. That marks the point where the rate trend changes from sideways to up. But it’s not always like that.

June 5 I just signed a refinance $300,000 30 year not insured mortgage 5 year fixed term at 2.39% with $1,200. cash back at HSBC. I also had to open a free chequing account at HSBC to get the cash back.

Hey Gary, Yes, all the big banks rope you into opening a bank account to get their cash lure.

HSBC is great for owner-occupied properties, but not for rentals. The maximum LTV on rentals is 70%, while BMO and Scotia will do 80%. HSBC also has a rather unfavorable rental add-back formula for calculating TDS.

My mortgage term is due in two weeks. I am torn between fixed and variable. TD offer a fixed rate of 2.19 and variable of 1.95. Need help on this please.Thank you!

Hi CC, See: https://www.ratespy.com/fixed-or-variable-rate-the-decision-checklist-02223752

@Brent – If you wait until 30 days before renewal the discounts might be 0.1% better. Conventional variable rates seem to be permanently worse than high ratio rates and I don’t see that changing this summer.

@CC my renewal is Sept 1 and TD is still offering me 2.27 variable and 2.36 five year.

@appraiser. So you want government to come in and solve your IRD problem. Hey I have a solution, a market solution. Choose another freaking lender!!! Spy talks about fair lenders all the time. If there is anything consistent with this broker based website (which is fantastic by the way), its the amount of sucking and blowing from the brokers, realtors, and commentators. Government please come in and solve my IRD problem. Oh, and don’t you dare tighten your insured underwriting policies even though you are taking on all the risk. suck. blow. suck. blow. rinse. repeat.

1) What risk is the government really taking? Do you think CMHC is lying when it says it has ample capital to survive a 30% national price crash?

https://www.cbc.ca/news/business/cmhc-stress-test-1.3855434

CMHC’s risk to taxpayers is the most exaggerated lie that housing bears perpetrate.

2) You could outlaw penalties tomorrow and all that would happen is the banks would rates rates and fees. Then EVERYONE with a mortgage would pay more instead of just people who break their mortgage contract. Careful what you wish for. Banks always win, one way or another.

Get Real, Regarding #2, that’s absolutely right.

We have a three year fixed term @ 2.39 that is coming due on September 01.

TD is offering us 2.10 for two years. I know the variable rate should be in the 1.6 % range because that is what a friend of mine is paying at the moment.

In 2009 when the Prime rate was this low I was on a variable rate down at 1.14. I know that there is room to come down for customers with history with their lender.

Requalifing with another lender involves a lot of legwork but might be worth it?

One might have to tell his lender if he goes to all in on the research with a competitor then he is going to go with them. What is their best offer?

They will not want to see your credit cards and investments cross the street.

Rates are going to go lower and it will take years for the economy to recover as it did after 2009. The bank of Canada might even reduce the rate another .25 over the next few months. It will be no quick recovery so raising them again in the next few three years or more is not going to happen.

13% unemployment with an economy that is going to go through a complete restructuring along with huge government debt is going to keep the BOC on the sidelines.

The CMHC is an outdated blood sucking entity. One which serves no purpose but to steal a good portion of hard working Canadians down payments.

I know a woman who was approved on her own at TD but was under the 20 % downpayment threshold. After CMHC stepped in she then had to first pay off her car, and then come up with a further $15,000 down payment in which they stole $12,000.

The banks can decide on their own who can qualify without CMHC. It is a bloated top heavy unnecessary leech with 1700 employees that transferred a annual dividend to the Federal government of $505 million in 2019.

$375 million in 2018.

How much less interest over time could average Canadians save on their mortgages with a larger down payment. Just another Tax and government created jobs. Sad .. Time for my antidepressants

Hey Alan, But other than that CMHC is great for Canadians, right? 😉

P.S. Check those dividend numbers. They were much higher on an annual basis.

@Broker – I agree with your analysis. We won’t get back to a “good” discount on conventional variables before our renewal in August, but I’m willing to wait and see. Cheers.

Well said Alan Pugh.

I just submitted docs last nite on my 2.49

30 yr fixed with 4500.00 back from previous lender.

Was that a smart move having to pay about 9 k in closing and fees?Previous was 3.75.

Hi Russ, Depends on your remaining term and mortgage amount, among other things. Here’s a calculator to determine the savings from your new rate: https://www.ratespy.com/mortgage-rate-comparison-calculator

Hi my rate is 3.65 for 5 years and I have 3.8 years left I In my term and my bank giving me 2.14 for five years with the penalty 4200$ can any one give me any advice What I will do I really appreciate that.

Sultan, you need to provide more information for an exact calculation (at least the mortgage amount, amortization).

But, with a 1.51 rate difference, a 100K mortgage will cost you roughly 1500$ more each year. (A little bit less depending on amortization, and the amount of principal you are paying each month). That will be more than 5000$ in the next 3.5 years.

So, as a rule of thumb, if your mortgage amount is more than 100,000$ and you can afford the penalty now, it will probably be worth doing it.

But, man, they robbed you at 3.65 last year (I assume it was a 5 year mortgage). I would never bank with them if I were you 😀 If you are going to break it, you might as well take it some where else. Some offer better rates, and some offer cash backs that covers at least part of the penalty. Some offer both.

Another thing to consider is, if you are likely to break it again. If you are planning to up-size or down-size any time soon, it may not be worth breaking now for a 5 year fixed. You may want to go variable or stay put.

Thank you for ur reply M, I already calculate my numbers how much I’m going to save in my principal and how much I’ll pay the interest if I change my mortgage rate to 2.14 % . My question is is this a good time to do the renewal or should I wait one more month , and also I can’t go to other bank because of my wife’s job so I have to stick with my current bank ?

Sultan,

Sorry the 4200$ penalty and the rates you mentioned in your first comment confused me, as they have nothing to do with the question you are asking 😉

If you have done the math, you already know how many months of wait is worth waiting for every 10 bps drop in the rate. So, tell us, how much the rate should drop further for a 3 month wait to be worth it?

But if you are asking if the rates are expected to drop further, and if yes, when and by how much, I’ll leave that to the Spy to answer.