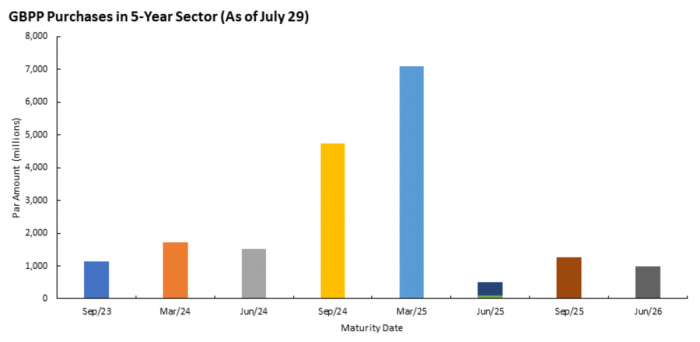

Snapping Up Bonds: Fixed-rate mortgage shoppers dreaming of lower rates better hope for lots of bond buying in the months to come. And that’s what we’re getting from the Bank of Canada. The BoC is buying a lot of 5-year bonds, which heavily influence 5-year fixed mortgage pricing. Under the Government of Canada Bond Purchase Program (GBPP), which launched on April 1, 2020, the Bank of Canada says it has purchased ~$19 billion of 5-year Government of Canada bonds in the secondary market (see chart below). That’s in addition to its ongoing auction purchases. The BoC snapping up government debt has a powerful effect on mortgage rates because Canada’s 5-year bond market isn’t that big. “…The total outstanding amount of the current 5-year Government of Canada ‘Benchmark’ bond is $32.5 billion,” says the BoC. “For the ~5-year sector [as a whole]…the total outstanding amount is approximately $120 billion.” In other words, the BoC is directly removing roughly one-sixth of the 5-year supply in the open market, and indirectly impacting the rest. That makes it easier for our central bank to move yields, but ultimately our 5-year bond takes most of its cues from American rates. So as long as the BoC and U.S. Federal Reserve keep manipulating bond markets there will be 5-year fixed bargains aplenty for months to come.

Source: Bank of Canada

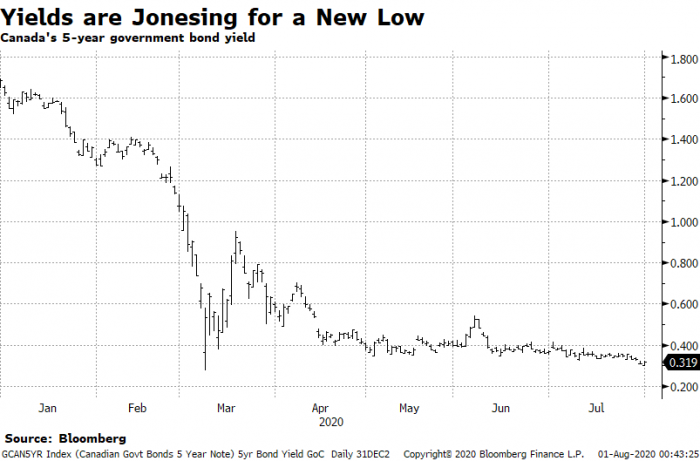

Second Dip Ahead?: “…The increase in virus cases, and the renewed measures to control it, are starting to weigh on economic activity,” said the world’s most powerful central banker Wednesday. This latest COVID spike south of the border might just be enough to sink 5-year bond yields to a record low. We’re only 5 bps away from one, as we speak—might as well get it over with already. If yields do dip lower, that’s obviously bearish for fixed mortgage rates, which are already doing the limbo under 2%. As it stands, government bonds are in one of their tightest ranges in history thanks in part to central bank interventions like that noted above. Something’s gotta give. Grab some popcorn and enjoy the suspense.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Hey Leo, This is just an educated guess but that would probably pull down the lowest insured 5yr fixed to near 1.30% to 1.45%. The lowest uninsured rates would probably fall to around 1.60% to 1.75%.

Rob, How much is BoC buying really forcing down rates? With the Libs spending so much they have to issue a lot of debt. Maybe that pushes rates higher.

Hi Jeff, Whenever you get excess buying in the bond market it typically keeps prices up and yields down (since the two always move in opposite directions). How much is hard to say but we know that yields are lower than they otherwise would be. What will likely happen is that yields don’t drop that much (due to BoC buying), but rather the BoC counteracts the upward yield influence of record-high government debt issuance. Here’s a good report on that if you’re interested: https://economics.cibccm.com/economicsweb/cds?ID=10729&TYPE=EC_PDF

Hi Jay, Not directly, for the time being. But the BoC has taken other action that improves variable-rate pricing, like implementing its Bankers’ Acceptance Purchase Facility, and of course, slashing the overnight rate. Variable-rate discounts should continue to slowly improve so long as the economy doesn’t go completely off the rails once again.

I was surprised by the rates offered to me by my green bank on an uninsured renewal this week. 1.94% for 5 yr closed variable (prime – 0.66%) and 2.19% for 5 yr fixed. My question for you is that the payments quoted to me for each didn’t make sense at face value. The payment for the variable was quoted about 10% higher despite having a lower rate. The reason I was given was that it had to do with keeping amortization should interest rates rise – that confused me. Am I being fed a bunch of baloney? Thanks Spy!

Hi Avner, Both those rates are about par for the course these days for a big bank on renewal.

Regarding TD’s variable-rate payments, I can’t speak to your particular case but generally speaking:

* TD payments remain fixed for the full five-year term

* They’re often calculated using a higher interest rate to, as TD puts it, “pay off the principal faster and to safeguard against interest rate increases.”

Spy, my bank is offering early mortgage renewal for 5 yrs fixed at 2.45%. Is it in my best interest to wait longer (closer to maturity date), as it sounds like the 5 yrs rate will keep dropping.

Hey Jan, Unfortunately I don’t know your situation (tolerance for higher payments, maturity date, ability to qualify, etc.). What I can say for sure is that 2.45% is an above-average rate, unless it’s got a long-term rate hold. For a well-qualified borrower with a maturity later this year, locking into that kind of rate probably doesn’t put the odds in his/her favour.

I have a mortgage up for renewal in December, can renew in August early, should I wait til closer to December seems the rates keep going lower and lower. Talked to the bank last week and they said 1.95% 5 year variable and 2.24% 5 year fixed.

Hey Steve, Same deal as Jan. It partly depends on how qualified you are, your financial situation, etc. If you can last until 120-days before maturity, you’ll get much better rates (sub-2%) from other lenders. That’s what I’d do personally, for what it’s worth.

TD offered me bank mortgage prime minus 0.73% today effectively 1.87% for 5 year variable closed. I think it’s too high because the rate is linked to mortgage prime and not bank prime. I am asking for a discount of another 10 basis

Points and they aren’t budging any suggestions for options for a well qualified borrower who is not in a high ratio situation

Hi Spy, Appreciate all the information you provide. I have HSBC P-1.06 variable rate. I do have a emergency fund for 1 year to survive without job. However, I am the only person in the family working now. Based on your experience is it better to lock down now.

Thanks Love, That’s an outstanding rate (1.39%) and a solid mortgage features-wise — being fully open after three years.

Not knowing your whole picture, it’s tough to provide proper advice. But given you were wise enough to build a 1-year safety net (which provides enough time to find another job and/or sell, worst case) and given you’ll save a ton in the next year or so with that 1.39% rate, I wouldn’t rush to lock in. I’m not sure how HSBC set your payment but if it makes sense, perhaps take any payment savings (vs. a 2% 5yr fixed payment) and bank it until you have another earner in the household.

Dear Spy,

Appreciate your help on clarifying everyone’s doubts.

I am a first time home buyer with limited knowledge about pitfalls of fixed mortgage. I have 2 options to take from BMO. #1) 30 years amortization , 5 years fixed interest rate1.92%

#2) 30 years amortization, 5 years variable Interest rate 1.85%. Due to family situations, there is a 50-50 chance I might sell this house at the end of 3 years or may be end of 4th year. what will be the impact of Penalty charges on Fixed rate when compare to the money that I would be saving by choosing Fixed option over variable option ( 1.85 vs 1.92) . Appreciate your suggestion on this.

log in

log in

17 Comments

Hi Spy – If the 5 year bond went to 0% what do you think that would mean for fixed rates? Thank you

Hey Leo, This is just an educated guess but that would probably pull down the lowest insured 5yr fixed to near 1.30% to 1.45%. The lowest uninsured rates would probably fall to around 1.60% to 1.75%.

Rob, How much is BoC buying really forcing down rates? With the Libs spending so much they have to issue a lot of debt. Maybe that pushes rates higher.

Hi Jeff, Whenever you get excess buying in the bond market it typically keeps prices up and yields down (since the two always move in opposite directions). How much is hard to say but we know that yields are lower than they otherwise would be. What will likely happen is that yields don’t drop that much (due to BoC buying), but rather the BoC counteracts the upward yield influence of record-high government debt issuance. Here’s a good report on that if you’re interested: https://economics.cibccm.com/economicsweb/cds?ID=10729&TYPE=EC_PDF

Spy, will this also affect variable rate mortgages – perhaps even lower rates?

Hi Jay, Not directly, for the time being. But the BoC has taken other action that improves variable-rate pricing, like implementing its Bankers’ Acceptance Purchase Facility, and of course, slashing the overnight rate. Variable-rate discounts should continue to slowly improve so long as the economy doesn’t go completely off the rails once again.

I was surprised by the rates offered to me by my green bank on an uninsured renewal this week. 1.94% for 5 yr closed variable (prime – 0.66%) and 2.19% for 5 yr fixed. My question for you is that the payments quoted to me for each didn’t make sense at face value. The payment for the variable was quoted about 10% higher despite having a lower rate. The reason I was given was that it had to do with keeping amortization should interest rates rise – that confused me. Am I being fed a bunch of baloney? Thanks Spy!

Hi Avner, Both those rates are about par for the course these days for a big bank on renewal.

Regarding TD’s variable-rate payments, I can’t speak to your particular case but generally speaking:

* TD payments remain fixed for the full five-year term

* They’re often calculated using a higher interest rate to, as TD puts it, “pay off the principal faster and to safeguard against interest rate increases.”

For peace of mind, ask TD for a copy of the amortization schedule and compare it to the amortization output of this calculator: https://itools-ioutils.fcac-acfc.gc.ca/MC-CH/MortgageCalculator.aspx?lang=eng&lang=eng

Spy, my bank is offering early mortgage renewal for 5 yrs fixed at 2.45%. Is it in my best interest to wait longer (closer to maturity date), as it sounds like the 5 yrs rate will keep dropping.

Hey Jan, Unfortunately I don’t know your situation (tolerance for higher payments, maturity date, ability to qualify, etc.). What I can say for sure is that 2.45% is an above-average rate, unless it’s got a long-term rate hold. For a well-qualified borrower with a maturity later this year, locking into that kind of rate probably doesn’t put the odds in his/her favour.

I have a mortgage up for renewal in December, can renew in August early, should I wait til closer to December seems the rates keep going lower and lower. Talked to the bank last week and they said 1.95% 5 year variable and 2.24% 5 year fixed.

Hey Steve, Same deal as Jan. It partly depends on how qualified you are, your financial situation, etc. If you can last until 120-days before maturity, you’ll get much better rates (sub-2%) from other lenders. That’s what I’d do personally, for what it’s worth.

TD offered me bank mortgage prime minus 0.73% today effectively 1.87% for 5 year variable closed. I think it’s too high because the rate is linked to mortgage prime and not bank prime. I am asking for a discount of another 10 basis

Points and they aren’t budging any suggestions for options for a well qualified borrower who is not in a high ratio situation

Hi Akalz,

Have a peek here: https://www.ratespy.com/best-mortgage-rates/500000/300000/25/any/+29/no/5-year/variable

Add information relevant to your case to see potentially applicable rates.

Use these rates as leverage with TD, or simply switch lenders if it’s worth it based on your circumstances.

Hi Spy, Appreciate all the information you provide. I have HSBC P-1.06 variable rate. I do have a emergency fund for 1 year to survive without job. However, I am the only person in the family working now. Based on your experience is it better to lock down now.

Thanks Love, That’s an outstanding rate (1.39%) and a solid mortgage features-wise — being fully open after three years.

Not knowing your whole picture, it’s tough to provide proper advice. But given you were wise enough to build a 1-year safety net (which provides enough time to find another job and/or sell, worst case) and given you’ll save a ton in the next year or so with that 1.39% rate, I wouldn’t rush to lock in. I’m not sure how HSBC set your payment but if it makes sense, perhaps take any payment savings (vs. a 2% 5yr fixed payment) and bank it until you have another earner in the household.

Dear Spy,

Appreciate your help on clarifying everyone’s doubts.

I am a first time home buyer with limited knowledge about pitfalls of fixed mortgage. I have 2 options to take from BMO. #1) 30 years amortization , 5 years fixed interest rate1.92%

#2) 30 years amortization, 5 years variable Interest rate 1.85%. Due to family situations, there is a 50-50 chance I might sell this house at the end of 3 years or may be end of 4th year. what will be the impact of Penalty charges on Fixed rate when compare to the money that I would be saving by choosing Fixed option over variable option ( 1.85 vs 1.92) . Appreciate your suggestion on this.