“What’s the lowest rate?” is one of those questions you can’t answer with one number. There are just too many factors that determine the rate someone pays. You have to ask more questions, like:

Wouldn’t it be nice if there was one simple page you could scan for all the best deals in Canada?

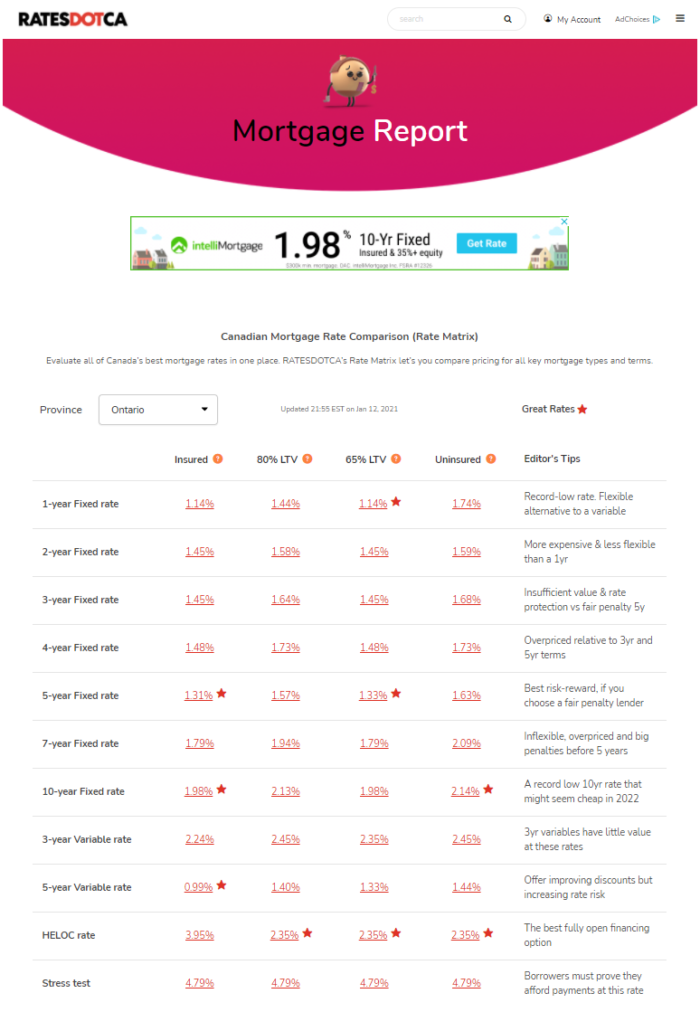

We thought so too, so our sister site, RATESDOTCA, created one. Its brand new rate matrix now tracks all of the lowest rates we know of across the nation — for all key terms and all key loan-to-values. (Caveat: It’s intended for qualified borrowers purchasing or refinancing an owner-occupied property.)

Inflation expectations are the #1 factor behind interest rate moves. It’s notable, then, that the Bank of Canada’s Q4 Business Outlook Survey (BOS) now suggests the market may be underestimating inflation risk.

57% of firms surveyed said they’d have trouble meeting an unexpected rise in demand. That’s up 13%-pts and “far above the long-run average of 35%,” reports Capital Economics. Firms also expect their:

input costs to increase at the fastest pace in two years

product/service prices to rise at the fastest pace in four years.

The BoC puts a lot of weight on this report. Analysts say it reduces the probability of a rate cut by the Bank of Canada next week, all else equal. But as the next paragraph conveys, all else is not equal.

State of Emergency

The State of Emergency declared by Ontario on Tuesday could weigh heavily on the Bank of Canada when it meets next Wednesday. The last state of emergency lasted over four months and resulted in hundreds of thousands of jobs lost. This one is bound to push back Canada’s economic recovery, and for that reason it increases the chance of a further 10-15 bps rate cut this quarter.

The BoC hasn’t cut less than 25 bps since it adopted the overnight rate as its main policy lever in 1996. But other central banks, like the Reserve Bank of Australia, have already done it.

A rate cut may not prevent Canada’s 5-year bond yield from rallying, however. Canada’s bond market is looking well past any short-term COVID adversity while simultaneously keying off rising U.S. bond yields. That means the path of least resistance for fixed rates is likely sideways near-term and up longer-term.

Scotiabank Cuts

The #1 lender in the mortgage broker channel, Scotiabank, lowered the following posted fixed rates today:

1yr: 3.09% to 2.79%

2yr: 3.19% to 2.89%

3yr: 3.79% to 3.49%

4yr: 4.19% to 3.89%

7yr: 5.39% to 5.29%

10yr: 5.89% to 5.69%

Those lower 1- and 2-year rates will unfortunately boost prepayment penalties for Scotia customers looking to refinance a mortgage with one or two years left on their term.

You’ll also notice that the bank cut all of its key fixed terms except the critical 5-year posted rate. It’s used to calculate the minimum stress test rate. Regulators are more than happy to see banks leave their 5-year posted rates right where they’re at to avoid further housing stimulus.

This & That

RBC CEO Dave McKay: “…We see growth continuing quite strongly right now, in the mortgage market…you’re seeing more rural areas shift into high demand. You’re seeing a little bit of softness in condo demand right now, but I expect that to come back because…you’ll see a surge of immigration.”—via Seeking Alpha

TD CEO Bharat Masrani: “In Canada…we’ve seen record numbers coming out of our mortgage book.”—via Seeking Alpha

Oppenheimer says the latest jump in bond yields is “misguided” given “the relentless downward pressure on prices that stems from the secular forces of algorithms in offices, robotics on factory floors, as well as trends in globalization affecting commodities, labour and corporate pricing.”

“…We see no change in the BoC’s policy stance on January 20th and continue to expect vaccines to lead to an acceleration in growth later this year.”—RBC Capital Markets

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

log in

log in