log in

log in Quick news nuggets from Canada’s mortgage rate market:

Quick news nuggets from Canada’s mortgage rate market:

- Not only has the yield curve inverted, but in some cases the mortgage rate curve has inverted. Among uninsured mortgages available in multiple provinces, for example, the best 5-year fixed rate is now below the best variable rate.

- There’s still tremendous value in insured variable rates—now effectively as low as 2.54% in some provinces.

- Markets are now almost fully pricing in a Bank of Canada rate cut by December. If we got one, it would take prime rate down to 3.70%. That is, if banks pass along the full cut.

- The souring economic outlook, a flattening yield curve, correction fears in real estate, market volatility and geopolitical risks could pressure bank profitability and increase funding uncertainty, said one banker I spoke with. That gives banks less reason to match 2018 rate discounts this spring. Offsetting this, however, is slowing loan growth. We sense that multiple top-20 lenders are behind on their mortgage volume targets year-to-date.

- 90-day bankers’ acceptance yields (a rough proxy for base funding costs on variable mortgages) are down 36 basis points year-to-date, giving banks a bit more room to improve variable discounts, particularly on uninsured variable-rate mortgages (where rate discounts from prime are unattractive at the moment).

- Don’t trust economists to tell you when there will be a recession. They’re notoriously behind the curve in predicting downturns. Worse yet, when they finally do recognize a potential recession, they “miss the magnitude of the recession by a wide margin,” says the IMF.

- Historical odds suggest otherwise, but former Fed Chair Janet Yellen says yield curve inversion might just result in rate cuts and not a recession.

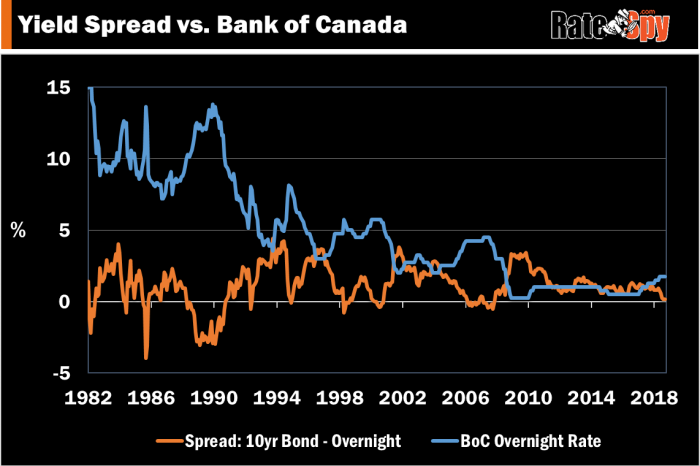

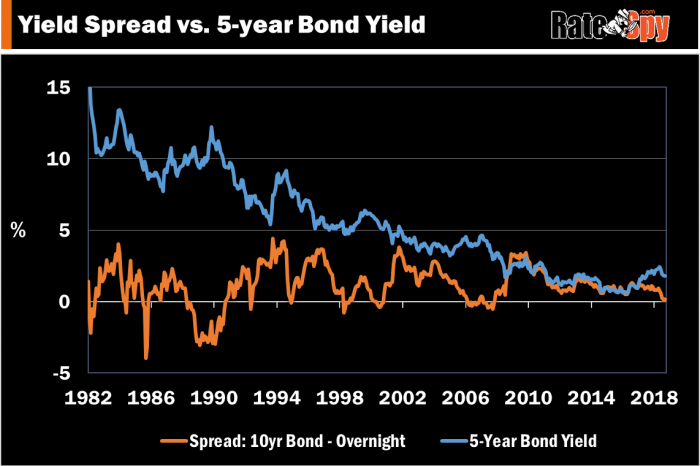

- Below are two charts showing how Canadian rates have fared after past yield curve inversions (when the 10-year yield fell below our overnight rate). The general down-sloping trend in rates biases the data somewhat, but it’s safe to say the Bank of Canada usually cuts after inversion.

12 Comments

Are variables still worth it if they are more than fixed rates?

Hi Chris, For certain risk-tolerant borrowers, yes. But in most cases, if we’re talking strictly uninsured mortgages with a $200,000+ loan amount, I’d probably lean towards a 1-year fixed under 3%.

I have to say that this website is the best of all mortgage websites. All your commentary is relevant and timely.

Q. Non insured purchase +$2M house with $400K mortgage. I just care about the lowest possible month payment over the next 5 years – but I need prepayment privileges of at least 15-20% per ann. What is your recommendation?

Hi John,

Thanks for the kind feedback. If someone wants the lowest possible payment, and that is the most suitable strategy for them, an Interest-only Flex may be the way to go. It’s a regular mortgage with 20% annual prepayment options. What’s different is that it’s not amortizing. Therefore the payment can be $500 less on a $400,000 mortgage.

I renewed my mortgage late last year and with the rate increases, it’s now at 3.10%. At what point would rock-bottom fixed rates make it worth switching to a fixed and locking in? It’s painful seeing 5yr fixeds available for under 3.00%. The only thing I can hope for now is a rate cut, which I see is looking increasingly likely.

Hi Qwerty,

Sounds like you’re in a variable. In general, we don’t recommend getting a variable with the intention of locking in. It’s hard to time rates and the conversion rates you get from lenders usually aren’t that great. A variable is meant to be a longer-term play. The idea is that you’ll pay less overall interest in a variable over five years, despite the ups and downs. So given no one knows where the bottom is in rates, the best bet (for a qualified risk tolerant borrower) is probably to ride it out. If the Bank of Canada embarks on a rate cut cycle and the market expects, it could last a while.

Is it a good idea to go for a 1yr fixed mortgage for new mortgage buyers instead of traditional 5yr fixed and by next year same time might a better idea on 5yr fixed refinance. Whats your thought on this idea ?

Hi San, Comparing a 1-year to a 5-year is like comparing a stock to a bond. They’re different animals. Since we can’t judge suitability on a website all I can do is make a few general comments:

1) People often get 1-year terms as an alternative to variable rates (they have similar risk profiles)

2) Never ever get a 1-year if you don’t have rock-solid employment, a reasonable debt load, great credit, stable finances, etc. You must ensure you can easily qualify again in one year.

3) The market is pricing in greater odds of lower rates in one year than higher. That and the inverted yield curve imply somewhat less than normal risk in a 1-year fixed

4) It’s extremely hard to time the rate market so we don’t recommend it

5) You may indeed find 5-year fixed rates lower one year from now, but you can’t count on that.

6) There is a reason one-year rates have outperformed fixed rates over the long run

7) Anyone taking a 1-year should ensure they’re saving at least 1/4 point versus a 5-year

There are other factors as well so do some research online and/or chat with a mortgage advisor before making the final call.

Excellent response from you. No wonder why people love this website more than others with an unbiased honest opinion.

The main reason why I thought better to go with 1yr vs 5yr were

1. Canadian housing market has reached its tipping point and very little room to move higher.

2. The overall economy in Europe, China , Canada does not look great. US could be the bright spot but that is getting dimmer every quarter.

3. So, I see the chances of rate cut of .25 to .5 points high in Canada within the next 6 months to 1 year. (Guess work: First cut in Oct and next cut in Mar 2020)

4. A falling housing market with rate cuts could potentially shake some ground and BoC may need to look for new ammunition.

So in that case, the market has to adjust to the new reality, kind of inverse of 2015/2016 conditions.

All the above discussed is based on my personal opinion .

Thanks

Thanks San, It’s quite possible you could be right and believe me, I (personally) would take a 1-year over a 5-year for some of the reasons you mention, as well as the reasons I posted. Of course, what’s right for me is not right for everyone.

It looks like bond yields may have hit a bottom this week. Today the 2yr yield is up 10bps on the good January GDP numbers.

The Alberta production caps helped push down the numbers for the energy sector, but those are set to bounce back as they get dialed back every month.

The WCS discount should stay below $20 for the rest of the year, which will help the GDP numbers for the energy sector.

I see little chance of a rate cut from the BoC in the next year. I also don’t expect a rate hike either, as inflation is unlikely to hold above 1.75%.

It’s never a straight line to the bottom.