log in

log in“Young folks with mortgages regularly thank me for keeping interest rates low.“

—Bank of Canada Governor, Stephen Poloz

In fact, Mr. Poloz’s decisions to keep rates low have practically been made for him, by serially disappointing economic data. Monetary policy has merely reacted to what he terms “a steady decline in the potential growth rate of the economy.”

In fact, Mr. Poloz’s decisions to keep rates low have practically been made for him, by serially disappointing economic data. Monetary policy has merely reacted to what he terms “a steady decline in the potential growth rate of the economy.”

In fact, Mr. Poloz’s decisions to keep rates low have practically been made for him, by serially disappointing economic data. Monetary policy has merely reacted to what he terms “a steady decline in the potential growth rate of the economy.”The BoC chief went on to reiterate a cold hard truth this week (or at least a cold hard forecast). That is, that our economy could grow at listless “1.5% for the next number of years.”

Good God. The next thing you know, LeBron James will be averaging less than 10 points a game. These are paradigm-shifting low numbers.

The BoC’s GDP forecast is so dim that if realized, 1.5% growth almost rules out rate increases. Almost.

Note his very legitimate rate warning: “…We’re dealing with lower for longer, not lower forever.”

That brings up the next point…

Canadian Rates Will Climb

But not tomorrow.

But not tomorrow.

And not likely in 2017.

Nonetheless, rates will defy expectations when we least expect it. And this just happened to be the topic of this week’s Globe & Mail mortgage column.

Despite that story’s alarming headline, “Variable Rates Will Soar…” (in case you’re wondering, columnists like me don’t get to write our own headlines), it had a less alarming purpose: to get people prepared for rate hikes—even if they think they’ll be dead before we see them.

The reason is simple. Interest rates can be devilishly deceptive. In the short to medium term, they can do what you never thought they could, faster than you ever think they will.

Planning prevents panic. Knowing what could happen after a 1- or 2-point surge in prime rate helps borrowers avoid calling their lender in dismay to convert a perfectly good variable into a fixed rate.

Of course, if the sound of a 4.70% prime rate scares the bodily fluids out of you, you likely belong in a fixed-rate from the get-go.

Fed Kicks the Can to Late 2016

The Fed met today and chose not to pull the trigger on a rate hike. But it cautioned, “The case for an increase in the federal funds rate has strengthened.”

The Fed met today and chose not to pull the trigger on a rate hike. But it cautioned, “The case for an increase in the federal funds rate has strengthened.”

That has trader-types placing better-than-even odds on a Fed increase in December, one full year after its last hike.

Team Yellen has once again prophesied “only gradual [rate] increases” to come. If she’s right that core inflation won’t hit its 2.00% target until 2018, U.S. rates will keep growing slower than a saguaro cactus.

Canadian Rate Scene

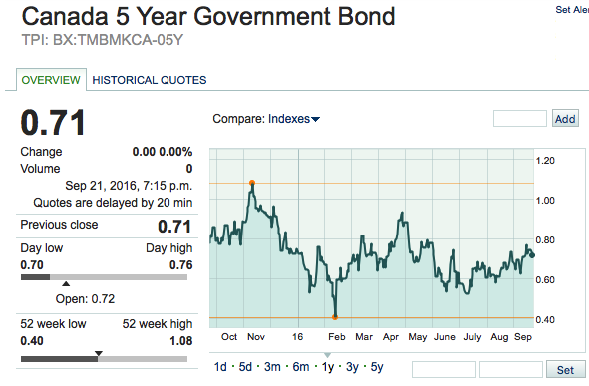

Fed drama barely budged Canada’s 5-year bond yield today, which shows what a non-event its announcement was on our side of the border.

Source: MarketWatch.com

In the past week, short- and long-term mortgage rates, be they fixed or variable, held steady Eddy. Average 5-year fixed rates are still just 11 basis points above variable rates—an unnaturally tight spread.

Don’t expect any widespread mortgage rate shifts until the 5-year yield closes above 0.96% or below 0.49%. In the meantime, the best values remain in 1-, 2- and 5-year fixed terms. The short terms provide minimal lender commitment with maximum interest savings, and the 5-year is a set-and-forget solution at a historically ridic rate.