log in

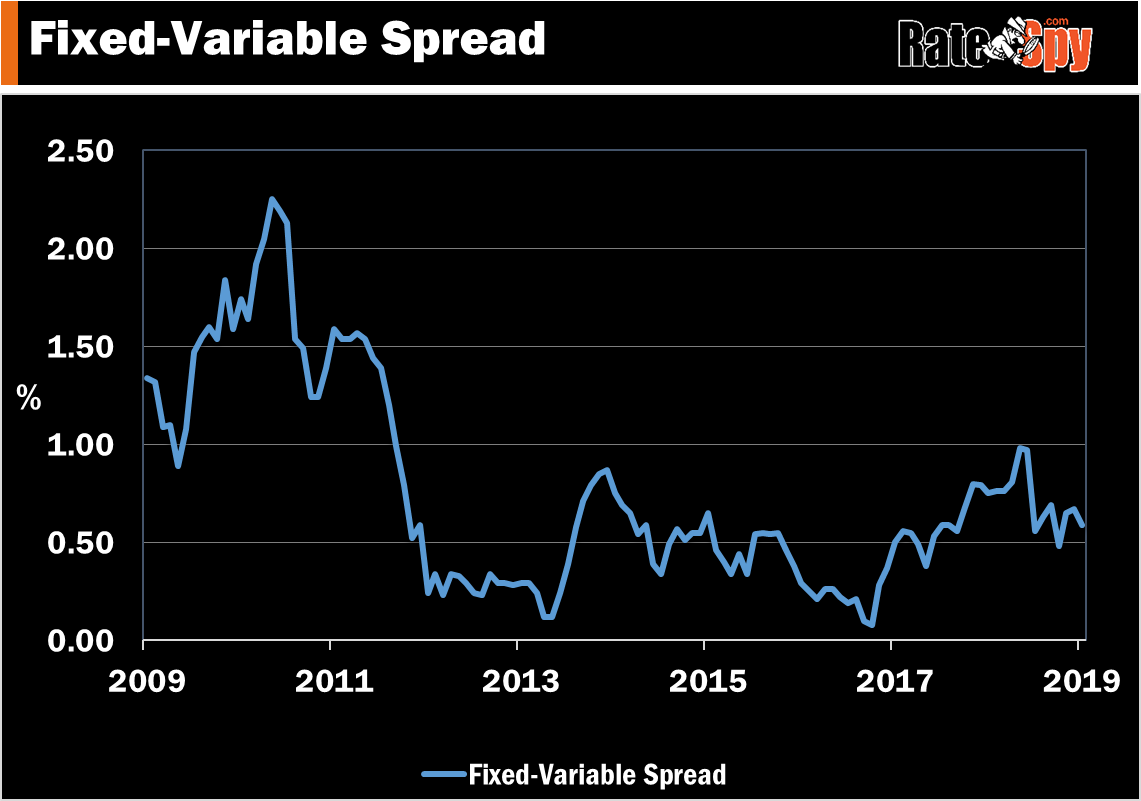

log inA regular consideration when choosing between a fixed or variable rate is the difference between them. As of late that “fixed-variable spread,” as we jargony industry people call it, has been slowly narrowing.

So far, it has mostly been a result of diminishing variable-rate discounts. Just this morning, for example, TD hiked its advertised variable rate a head-turning 20 bps. While TD mortgage rates don’t necessarily dictate what other lenders do, this news does follow a series of public and internal variable-rate hikes from other banks.

More importantly, TD’s move today is reflective of the margin compression big banks are seeing, and expect to see, in the floating-rate market. (Note: TD’s increase affects only new variable-rate customers, not existing borrowers.)

Fixed rates are also a factor. As fixed rates drop, the spread tightens further. Most in the industry fully expect 5-year fixed rates to edge lower this quarter, which could narrow the fixed-variable spread in a meaningful way.

Swaying Decisions

If this trend continues, the fixed/variable decision will become incrementally more difficult, at least for some.

Historically, whenever the spread has approached 1/2 percentage point or less, more people start considering fixed rates, which are viewed as a form of rate insurance.

But unless it shrinks considerably the spread may remain a secondary factor for term selection. We don’t expect significant shrinkage unless/until the economy weakens further. That’s when investors could become more worried about big bank risks, which in turn could increase banks’ funding costs.

For now, factors like the general outperformance of variable rates, Canada’s less-bullish rate outlook, the penalty advantage of floating rates and their upfront rate advantage are more salient to most borrowers.

Fixed Rate Update

Just yesterday, Canada’s lowest 5-year fixed rate dropped to 3.14%. That’s the lowest it’s been since October. Unfortunately, this deal only applies to insured purchases closing by Feb 28 and it’s available only via brokers.

The lowest 5-year fixed rates on lender switches and refinances are still stubbornly high—as are discretionary rates at most big banks.

Give it time, however. The more bank competitors drop their fixed rates, the closer we get to the Big 6 dropping theirs…and the more the fixed-variable spread will come into play.

12 Comments

Hi,

Why is it that HSBC’s rates are generally better than the major banks?

E.g. 5 year variable = prime – 0.96 vs other banks at prime – 0.8?

Hi Clinton,

Here’s the answer: https://www.ratespy.com/hsbc-making-mortgages-easier-11187175

In essence, HSBC is buying market share and offsetting the cost of doing that (the extra discount) by cross-selling the consumer other financial products.

It’s a great model because the client saves interest and the bank has a sustainable model. Moreover, HSBC doesn’t take a hard sell approach, unlike some banks that actually put their mortgage reps on cross-sale quotas (e.g., we expect you to sell one creditor life insurance policy for every 3 mortgages).

I took a five year variable with TD in November 2018 for 3.25%. At the time, our annual rate was TD mortgage prime rate less 0.85%. So the TD mortgage prime rate was 4.10% (less 0.85) = 3.25%

Am i still getting that 3.25% rate or am i now at a higher rate?

Hi J,

If you’re paying as agreed, your variable rate won’t go up unless TD raises its “mortgage prime” rate. It hasn’t done that since the Bank of Canada hiked in October.

Thanks for the reply 🙂

Upon renewal, historically, has HSBC’s rates been competitive too, relative to other banks?

Are there any precautions when going with HSBC compared to other major banks?

It seems also that they have put their best rates (with no rooms for further discounts) online on their website. Is this true?

Would you agree that Prime – 0.96% for a 5 Year Variable rate a good one to take? They were offering Prime – 1.06 + $1000 cash back in the summer of 2018 but i think those days were over. I’m still trying to ask them if they can offer me the $1000 cash back but i’m still waiting for answers.

Thank you for the help!

HSBC renews people at the bank’s best advertised rates, which—as you have noted—are generally quite good.

Yes, unlike the majors who play games with their published rates, HSBC puts its best foot forward and advertises its lowest rates online (including here).

If you switch your mortgage and qualify, you get prime – 1.01.

One money-saving (and rare) feature with HSBC is that its variable is fully open after three years. That can save borrowers a prepayment charge if they discharge early.

Like all big banks, HSBC has a posted-rate IRD penalty on fixed-rate mortgages, which can get costly if you break before 5 years (costly relative to those non-big-bank lenders with cheaper penalties).

Desjardins Bank is trying to get us to renew our mortgage as quickly as possible before the mid-March renewal date as they predict rates are going up. Twice they have guaranteed us rates for 2 weeks at a time, and as we can see, the posted rates are not changing lately. They provided fixed rates for 1-5 years with discounts to the prime rates on 3, 4, or 5 years. Should I continue to request they extend the offer for as long as I can, do they typically just keep guaranteeing for weeks at a time? Also, for a borrower comfortable with fixed rates, do you have advice for term length?

It’s pretty common for lenders to create a sense of urgency by only offering to guarantee a rate for a short period. They want you to commit to them and stop shopping around. But more than that, lenders can’t hold a rate quote indefinitely because the market moves regularly. If you want to lock something in, you need to apply.

Bond yields, which *usually* guide fixed rates, appear in no danger of making new relative highs near-term. As such, rate risk is less than normal and therefore I wouldn’t rush to lock in unless you’re getting a great deal.

Historically, shorter fixed terms have outperformed longer fixed mortgages. But term length also depends on a lot of personal factors like sensitivity to rate volatility, moving plans, potential of refinancing, job mobility, etc. So it’s tough to provide personalized advice on that one without a little Q&A.

Thank you for the replies! It’s very helpful 🙂

Can i also ask, you referenced that HSBC’s 5 year variable rate is closed for the first 3 years and open for the remaining 2 years. I heard this from HSBC’s rep too. It’s interesting. What’s the main advantage of this? Is it if we decide to sell the property for example in year 4 or 5, then we would not incur any penalty? Any other advantage of having this VS a 5 years variable closed?

Also, if i bought a pre-sale condo in 2015 that’s let’s say 300k and today it’s worth 600k, and the condo is completing within the next 2-3 months (down payment of 20% paid), am i able to take a HELOC based on the assessed market value at completion as opposed to a HELOC that’s based on the purchase price? How much HELOC would i be able to set up?

I asked Scotiabank and they told me that they’re able to do it using their STEP program and i asked HSBC and they told me that they’re only able to set up a HELOC based on the purchase price (300k), not the assessed market value upon completion. Is the policy different for every banks in regards to taking the purchase price vs assessed market value upon completion?

Thanks for the help! Really appreciate it!

Q: What’s the main advantage of this?

A: No penalty if you want to sell, switch or refi after 3 years.

Q: Is the policy different for every bank in regards to taking the purchase price vs assessed market value upon completion?

A: I’ll assume by “assessed” you mean “appraised.” Yes the policy varies in some cases but most prime lenders base their lending value off the purchase price.

Considering the fact that based on many predictions we may see 2-4 hikes on prime rate during next 2 years, and more penalty fees for braking a fixed rate mortgage, do you think is it still wise to choose let say 5 year variable P-1.25 (%2.7) against a 5 year %3.27 fixed rate?

Thanks

Those 2-4 hike predictions are not aligned with the market, which sees 1-2 at most. We don’t predict rates but if the market is right, a variable would be the clear winner for most well-qualified prime borrowers. 2.70% is a fantastic rate by the way.