log in

log inKnowing the future wouldn’t help you pick the right mortgage.

Unless you knew all the future.

Imagine a fantasyland case where it was 100% certain that all mortgage rates would be higher in five years. With that priceless information most people would take a 2.49% five-year fixed over a 2.59% one-year fixed.

But initial rates and ending rates are only two of the variables that determine borrowing cost. There’s a lot that happens in between the start and end of your term.

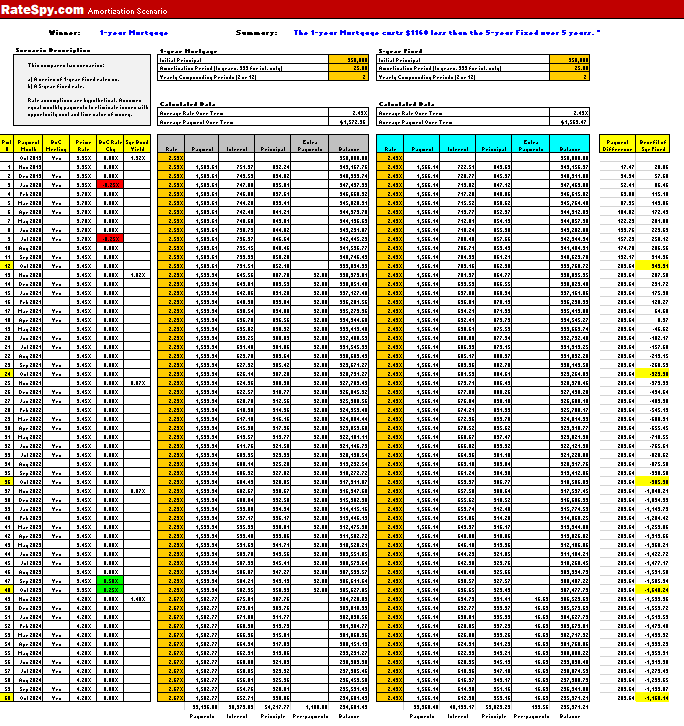

For those who don’t alter their mortgage before maturity, it’s often the path of rates that matters most. This scenario on the right (click the image) shows why.

In this hypothetical, the advantage of a lower starting rate is negated by a lower average rate over five years. There are countless ways that could happen. One of them: the Bank of Canada cuts rates in the first 12-18 months before hiking a year or so before you renew. Some argue that this is the setup that could be taking place right now.

Regardless, what anyone thinks might happen is secondary to what history shows actually does happens, more often than not. That is, shorter-term mortgages give people a solid chance at a lower average rate over five years.

Yes, you have to renew more often in a 1- or 2-year fixed and yes there is a cost for that (usually at least a $250 to $300 “discharge” or “assignment” fee from your old lender). And, on terms under three years, many lenders don’t cover transfer fees (legal and appraisal charges) either.

On the other hand, you may get lucky and have a lender that offers decent renewal rates. It helps if you choose a competitive lender that transparently advertises rates in the first place.

And borrowers for whom a short-term mortgage is suitable cannot ignore the other benefits of shorter terms:

- Unlike our example here, shorter terms are usually cheaper than 5-year mortgages (And that’s the case today. They’re up to 1/2 point lower as we speak, depending on your province and down payment.)

- Like variable mortgages, the best 1-year fixed rates have beat the best 5-year fixed rates the majority of the time.

- Less penalty risk if you renegotiate or discharge your mortgage before five years (depending on the lender you’re likely looking at a three-month interest penalty with a 1-year mortgage, versus a potentially heinous IRD penalty in a 5-year fixed.)

- Choice of any term at renewal, including the industry’s best promotional rates.

- The ability to lock into a long-term rate later if need be.

So, expect that rates might be higher five years from now. But don’t expect it to mean short-term mortgages will lose, as enticing as today’s 5-year fixed rates may be.

8 Comments

For many Canadians, going short term brings a material renewal risk for them: reduction in income, fall in credit score, unexpected events over the course of 5 years etc. Locking in for 5yrs (or longer) at stupid low rates means that you are safe and sound as long as you make your payments (regardless of income source, should income fall, unemployment etc.). Its that darn IRD that is the killer. So what’s more likely over the next 5 yrs: a reduction in your creditworthiness, or a desire to refinance or break the mortgage early (moving homes etc..). IRD vs annual renewal risk – lets do it 1988 cage match style.

Some good points, thanks David. We tend to see more qualified borrowers take 1-year terms. In general, credit degradation after approval (for borrowers who are initially well qualified) is much less common than renegotiation before maturity in five years.

To the extent there are material financial risks in one’s life, a 1-year usually isn’t a fit. But to your point, not everything can be foreseen. That’s why it’s all the more important for folks to pick transparent competitive lenders in the first place. At least with them, you’re more likely to get a renewal offer that makes switching unappealing in the first place. And as long as you make all your payments on time (don’t default) you’ll always get a renewal offer.

Groan, who wants to redo their mortgage every year?

While the math certainly makes sense, I don’t want to think about my mortgage 2 months of every year (the two months leading up to renewal). To be honest I’d probably start rate watching 3-4 months out. I’m a broker (part time) and find this to be an awful proposal. After 5 years’ time I’d have spent AT LEAST 10 months (almost a year) thinking about a renewal or going through the process. I renewed mine in Spring of 2018, if the 10 year rate at that time was what is has been in the last few months I’d have been very tempted to take the 10 year term so that I could put it to bed. That said, could entirely be situational. I have 2 young kids and live down the street from their school (future school) and don’t expect to move for ~9 years minimum.

There’s a reason 5-year terms dominate. And that is one of them.

Of course, the point wasn’t to suggest everyone should go short. It’s to show that higher rates in five years don’t necessarily mean lower savings in a shorter-term. If time and convenience are greater factors than borrowing costs (and for many they are), a 1-year won’t be your cup of tea.

And you’re right, mortgages are completely situational. For example, why bother with a 1-year to save 10 bps on a $100,000 mortgage with a 10-year remaining amortization? It’s not worth it. At $600,000 with 30-years to go, it’s a different story. That’s one of the reasons lenders offer 8-10 different terms lengths.

The last thing worth noting is that a 1-year doesn’t bind you to a 1-year for the next five years. You might see a spectacular 3-year rate in 8-12 months, for example, and want to renew into that. Shorter terms allow such options.

Fair enough – I suppose I took the post a little to literally and linear.

Thanks!

The way I see it, if you’re leaning toward a variable go short term instead. The rates are much lower. Who cares if you have to renew more often if you’re saving a few thousand $$$.

I am calling dead cat bounce on the 5 year bond rate (and all of the the other terms)

With the meetings in 6 weeks by both BOC and FED, and the Federal Election probably out of the way (unless it is a minority), I think bond rates will be on the downward slide.

Must be a rubber cat. That’s a crazy bounce.

Forget the election and central banks. Keep watching inflation to see if the cat comes back to earth.