log in

log in

Mortgage Report – May 12

- Not So Timely: The government’s 5-year bond yield, which heavily influences fixed mortgage rates, peaked in October 2018. Since then, it has collapsed 212 basis points. Meanwhile, big banks have lowered 5-year posted rates just a stingy 30 basis points. The banking regulator (OSFI) considers that a problem and proposed to de-link the mortgage stress test from posted bank rates as a result. Well, RBC did “its part” today to narrow the gap. It cut its posted 5-year fixed rate by 10 whole basis points, to 4.94%. That puts it at the lowest point since October 2017 and makes it the lowest 5-year posted rate among the Big 6 banks. Yippee ki-yay.

- Who Cares? RBC’s posted-rate cut today has dual relevance:

1) As noted, the Big banks’ posted 5-year rates determine the government’s mortgage stress test. If one more bank lowers its current 5.04% rate, the minimum stress test rate could drop, making it easier for borrowers to qualify for a mortgage. Will this happen? Yes. We just don’t know when exactly.

2) Other things equal, a lower 5-year posted rate reduces interest rate differentials (IRDs), and hence prepayment penalties. That can potentially save borrowers money if they break a big-bank 5-year fixed mortgage early.

We say “other things equal,” however, because RBC also cut its shorter-term posted fixed rates. That can have the opposite effect; i.e., it can widen IRDs and increase penalties for existing borrowers who break early. Here’s the full list of RBC’s posted fixed-rate reductions:- 6mo convertible: 3.29% to 3.04%

- 1yr: 3.19% to 3.04%

- 2yr: 3.54% to 3.39%

- 3yr: 4.05% to 3.90%

- 4yr: 4.64% to 4.44%

- 5yr: 5.04% to 4.94%

- Economic Cheat Sheet: As we parse economic events, some readers find it hard to infer how such events could impact mortgage rates. So, going forward we’re adding a bit of help. Effective today, the Spy will make an attempt to gauge the impact of economic news on mortgage rates in a clearer way. We’ll do that with a quick summary in italics following economic news blurbs. Projected rate impacts will be labelled:

- “bearish” (i.e., the news could push rates down over time, other things equal)

- “bullish” (i.e., the news could push rates up over time, other things equal), or

- “minimal” (i.e., the news may have imperceptible impact on mortgage rates).

In reality, things are never “equal.” And, more importantly, the time frames for economic developments are impossible to speculate on, so we won’t. Specific economic predictions are a fool’s errand anyhow. That said, the hope is that such commentary might help readers who are adamant about forming a mental picture of how rates might play out.

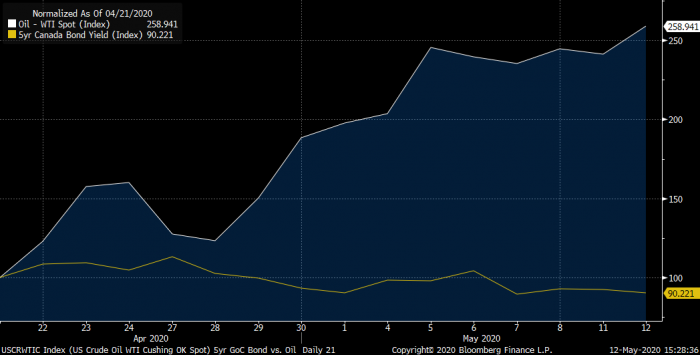

- Oil Panic Over, For Now: Just 22 days after traders couldn’t give a barrel of oil away (literally), the oil pendulum has swung towards fears of under-supply. Funny how that works. That’s got WTI oil trading near a one-month high. But, notice how oil’s 258% rebound since April 21 hasn’t budged one of Canada’s most important economic indicators, the 5-year government bond yield. Traders aren’t buying the energy turnaround story, and oil’s short-term bounce is barely impacting the long-term inflation outlook. Rate impact: somewhat bearish.

Data is expressed as indices so you can see the relative percentage changes.

- Trade Tensions Return: As if we need another cloud hanging over the economy, Washington’s denunciation of China’s handling of COVID risks jeopardizing trade progress between the two countries. Beijing showed what it can do this week by banning certain Australian meat imports, accusing the Aussies of spearheading a “malicious campaign to frame and incriminate them.” Now, with China also accusing the U.S. of a smear campaign, optimism on U.S./China trade is at a multi-month low. And yes, if things get frosty trade-wise, Canada won’t escape harm given its U.S. economic ties. Rate Impact: slightly bearish.

27 Comments

I expected some movement in the 5-year fixed rate as year bonds plunged below .4%. Nada.

Hi NatoK, We’ve seen a lot of fixed rates fall in the last few weeks — not hugely, but fall nonetheless. Like they say, rates take the stairs down and the elevator up.

“It cut its posted 5-year fixed rate by 10 whole basis points”

lolololololololololol

Oil is a dead commodity walking. Transportation accounts for most oil usage and it is all going electric eventually.

Bill you must be pretty young

Was just quoted by RBC~

2 yr fixed @ 2.34%

4 yr fixed @ 2.44%

Non high ratio/insured.

Going with the two year!

2yr rates would be far more popular if there were priced near historical levels, relative to the 2-year bond yield. But lenders are keeping them inflated.

That’s one reason we’re seeing an increasing number of people take a 2.35% fully open HELOC: https://www.ratespy.com/best/tangerine-mortgage-rates/0/heloc/3010

Their plan is to see how rates shake out by year-end, knowing it’s extremely unlikely prime rate is rising anytime soon.

The open term means no penalty and you can pick any date to switch to a better rate.

The main downsides are refinance costs and having to re-apply — but the former is often offset by lender cash-back offers.

That said, it’s definitely not a strategy for those who are less qualified, have a small mortgage, a short amortization and/or a lack of discipline with spending.

Good morning, Spy. Our mortgage renewal is coming up in August so we’re in the opportunity window and have begun shopping around. Rates look pretty good, but I’m wondering if you think they’ll reduce further in the next couple of months or should we pull the trigger now? Thanks!

Hi Steve, Rates are down-trending but that can change. Best practice is to get a rate hold (you can always switch lenders later, and most lenders will drop your rate if rates fall before closing). Some people are preferring to let it ride for a few weeks, hoping yields–and fixed rates–will drop more. There’s a small risk that rates go the wrong way if you do that, but keep an eye on the 5-year bond (https://www.ratespy.com/5-year-canada-bond-yield). If it closes above 0.60% I’d lock something in quick to be safe.

I suppose I should add: we’re looking for a 5 year fixed term, non-insured.

Good morning RateSpy

Thanks for the good work.

Thx IK

A 4.95% posted 5-year rate is still totally ridiculous.

Hey Kim, I hear you. Although, when you’re scared about plunging mortgage originations and surging credit risk, and you have oligopoly pricing power, you’re the smart one if you can pull off the ridiculous.

Bill,

I do agree with you that electric is ‘more efficient’ than the ICE. However, until you make a plane, train or ship that run on batteries, don’t underestimate the value of oil.

Also, don’t think that your ‘electric’ car is so environmental either. Where do you think the electricity comes from? Electricity in most parts of the world is either coal or nuclear. There is some solar, wind, hydro, etc, but that also requires a lot of free land which most countries don’t have.

The current oil issue is due to supply and lack of demand due to lockdown on travel. Unlike other industries, no one has regulated (or able to negotiate) the oil industry to “lockdown or reduce” (due to greed) and there is no demand as everyone is working from home.

I just realized how important it is to look at a lender’s posted rate curve when considering prepayment penalty risks. Early last summer I locked in a Scotia mortgage for 4yrs at 2.79% (1.8% discount from posted). Now that I’m considering an early renewal into a 5yr variable, the difference between the 3yr and 4yr is important. It’s 20bps (4.39 vs 4.19).

If the mortgage was at BMO, the delta is 59bps, which would make the IRD much higher.

Hi Ralph, Yep, wider rate differentials can make a mortgage discharge very unpleasant. And it can be hard to predict where those rate spreads will be some years down the road.

@Geek try TD they are offering 2.34% 5y fixed or 1.99% variable (P-0.61) for well qualified applicants.

Hi Steve,

It won’t hurt to lock into a rate now. Most Lenders will adjust the rate if it is lower when the actual renewal date comes

Tried TD Bank they offered me 2.69% while others qualified 2.34%. With over 20% down. Makes no sense

Rates dropped and crepped up again. But my opinion, it will fall sooner or later. Recession is true and fundamentals will support it.

@SpyFollower, unless my math is wrong, P-0.61 does not equal 1.99% but 1.84%…

@SpyFollower Do you know the details on TD’s criteria for “well-qualified”?

Beacon score > 720?

Investments with TD or high net worth?

<75% LTV and < 35% TDS?

All of the above?

To Chris’s comment on oil:

I said “eventually.”

Most oil is for cars and trucks. The IEA says oil growth for cars will peak in 2025. By 2035 most new 4-wheel transportation will be electric.

It isn’t just fully electric cars that will change things. Hybrids and improved fuel efficiency will reduce oil consumption more than fully electric vehicles until 2040 or so. Note I am getting my numbers from reputable sources like the IEA and EIA so don’t shoot the messenger.

As for trucks, trains, ships and heavy equipment, they may not go primarily electric for decades but natural gas and other fuels will eat into oil share.

Jet fuel is only 12% of transportation oil consumption. Oh yes and here is your electric plane

https://www.theguardian.com/world/2019/dec/11/worlds-first-fully-electric-commercial-aircraft-takes-flight-in-canada

We haven’t even talked about supply which is going to soar after the pandemic.

Anyone who thinks it’s going to stay business as usual for oil prices is smoking seven leaf plants.

That HELOC strategy is interesting but aren’t HELOCs demand loans in contrast to mortgages? Maybe more of a very short-term solution then?

I got to lock in a rate of 2.25% for 5 yrs. Would there be a possibility for the rates to go down until July 1st? Also, I have a question, if you have a 5% down payment on your initial mortgage and when renewal comes, you have less than 80% mortgage ratio. Would that still qualify as default insured mortgage on your new lender when 1st renewal comes up?

Hi Nada, On the first question, yes, there is a possibility fixed rates drop before July 1, but *if* it happens, I’d be surprised if the drop were significant. Maybe 5 to 20 bps at most.

On the second question, as long as you don’t refinance you can keep the mortgage default insured, regardless if the loan-to-value keeps dropping. If you switch lenders, just ask the new lender (or your mortgage broker) to confirm that your default insurance will remain in force.