log in

log inCanadian mortgage rates take their cues from many things, and U.S. monetary policy is near the top of the list.

That’s why today’s Fed rate cut—the first since the financial crisis—is meaningful to borrowers. Fed decisions always move Canadian rates in some respect but in this case, key questions remain. Here are the two biggest ones.

How Many Cuts Are Coming?

Just seven months ago, the Fed was hiking rates. Many find it hard to grasp how the growth picture has deteriorated so much in such a short time.

Just seven months ago, the Fed was hiking rates. Many find it hard to grasp how the growth picture has deteriorated so much in such a short time.

The fact is, the U.S. economic outlook “remains favourable,” Fed Chair Jerome Powell said today. The Fed blamed global factors (weaker overseas growth and trade frictions) for the cut more than any domestic problems.

“There really is no reason why the expansion can’t keep going,” Powell added.

Others agree. “What the Fed is doing is unprecedented. There’s no historical precedent,” said Ethan Harris, head of global economic research at Bank of America Merrill Lynch. “There’s no example that with still above-trend growth and still above-trend labor growth [the Fed…] eased in the middle of an expansion. This is a six-sigma event.”

For reasons like these, it’s easy to see why the market views this as an “insurance cut” — one designed to head off a potentially more severe economic slowdown.

But here’s the thing with insurance cuts. Historically, they’re not as aggressive as cuts made during economic crises or periods of surging unemployment. Indeed, the Fed characterized today’s move as merely a “mid-cycle adjustment,” suggesting multiple future reductions are not written in stone.

That’s why 25-75 bps of rate easing is the most the majority of economists expect from the Fed at this point—with the market pricing in one easing more this year.

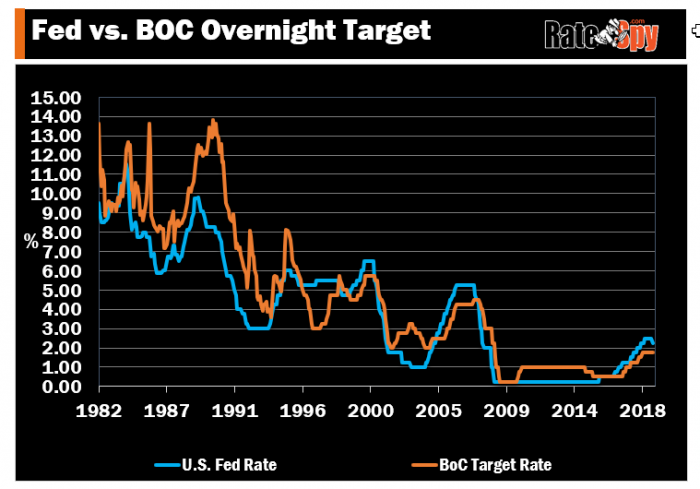

Will the Bank of Canada Follow?

Using history as a guide, there’s a high probability it will if the Fed cuts 1-2 more times.

Here’s how the country’s two key rates have moved together over time:

Today’s rate drop further reduces the odds that Canadians will see “rate normalization” (i.e., rate hikes that get us closer to the BoC’s estimated “neutral rate”) anytime soon. That neutral rate now seems worlds away at 100 bps higher than we sit today.

Canada’s benchmark 5-year bond yield was up slightly following the Fed’s announcement. That suggests traders aren’t overly worried that Fed policy will push our rates lower. Apart from that, yields offered few new clues on where Canadian mortgage rates go near-term.

As for the BoC, today’s Fed cut will not change the Bank’s gameplan (which Poloz described this spring as “on hold for a while”). Canada’s economy remains buoyant enough to deter BoC easing indefinitely.

How to Play It

A single rate meeting rarely justifies a change in one’s mortgage strategy. Today’s cut is no exception as it was fully priced into the market.

A single rate meeting rarely justifies a change in one’s mortgage strategy. Today’s cut is no exception as it was fully priced into the market.

If you’re a mortgage shopper trying to parse all this into a workable strategy, here are three quick thoughts on the best terms du jour:

- 5-year fixed mortgage rates

- Remain a decent play for risk-averse borrowers assuming they:

- Get a 15-20 bps discount to comparable variable rates, and

- Select a fair penalty lender if there’s any chance of renegotiating the mortgage before maturity

- Remain a decent play for risk-averse borrowers assuming they:

- 2-year fixed mortgage rates

- At 2.49% or less are still a tremendous alternative to variable rates, with more refinance and porting flexibility in most cases

- Variable mortgage rates

- Remain acceptable for borrowers with a big asset cushion and tolerance for volatility

- We say this partly due to their:

- Historical edge

- Cheap penalties

- Ability to ride rates lower (the big wildcard).

As for the foreseeable rate future (an oxymoron, admittedly):

- Fixed mortgage rates probably won’t drop much more until the 5-year bond yield closes below 1.25%.

- Variable rates are partly dependent on prime rate (as usual) and partly dependent on their discount to prime rate (for new borrowers). Both prime rate and the discount could remain in neutral for months, assuming the market expectations are correct.