log in

log inThe Bank of Canada ended 2019 where it ended 2018, with prime rate frozen at 3.95%.

Here’s a summary of the Bank of Canada rate decision this morning:

- Rate Announcement: No change

- Overnight rate: Remains at 1.75%

- Prime Rate: Remains at 3.95% (see Prime Rate)

- Market Rate Forecast: One rate cut in 2020

- BoC’s Headline Quote: “Future interest rate decisions will be guided by…the adverse impact of trade conflicts against the sources of resilience in the Canadian economy—notably consumer spending and housing activity.”

- BoC on the Economy: The Bank cited “waning recession concerns”

- BoC’s Full Statement: Click here

- Next Rate Meeting: January 22, 2020

The Spy’s Take

For nine straight BoC meetings there’s been a tug of war between competing rate factors.

Here’s what the Bank’s grappling with today:

| Dovish Factors | Hawkish Factors |

|---|---|

| Trade risk | Low unemployment |

| Weak GDP | Wage growth |

| Weak exports | Housing strength |

| Drab consumer spending/confidence | Rebounding business investment |

Jargon buster: Dovish refers to factors that may support lower rates. Hawkish refers to factors that may support higher rates.

These competing influences are making the official price of Canadian goods and services rise at the BoC’s preferred pace.

“The Bank continues to expect inflation to track close to the 2% target over the next two years,” it said today. Being an inflation-targeting central bank, and given future inflation expectations are anchored near 2%, the BoC has little reason to move near-term.

The BoC reminds us that “ongoing trade conflicts…are still weighing on global economic activity, and remain the biggest source of risk to the [economic] outlook.” Add that to consumer debt risk (which lower rates could exacerbate) and steady inflation, and you can understand why the Bank left rates as is.

South of the border, the U.S. Fed meets next week. Those meetings are top-of-mind for any avid Canadian rate watcher, given Canada’s rates usually follow American rates…eventually. The Fed is expected to leave U.S. rates where they are for now, but cut once more in 2020, according to Bloomberg projections.

How to Play It

Borrowers will find few new clues in today’s Bank of Canada rate decision, save for a slightly more optimistic tone.

But its tone today has little relevance for mortgage-term selection over the medium to long run. Other more relevant factors include:

(A) Your qualifications and five-year plan

- More on that here: Should you get a fixed or variable rate?

- For example, in the next five years: Might you move or refinance? Add to your family? See an income change? Have a higher debt ratio? Split up with your significant other? Need other mortgage flexibility—to avoid penalties? etc.

(B) Canada’s flat-rate market in general.

- As we speak, the best prime mortgage rates are nearly the same, regardless of which term you prefer. For example, the difference between the lowest nationally-available conventional 5-year fixed rate and variable rate is just 10 bps. Historically it’s been over 75-125 bps on average.

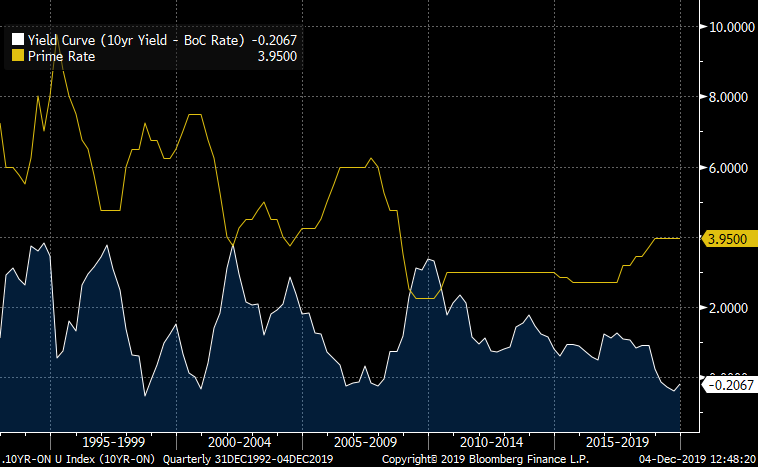

- A flat-rate market (i.e., flat “yield curve”) has historically foreshadowed flat-to-lower rates in the coming five years, as the chart below illustrates.

- With the market expecting no major rate moves for the foreseeable future, and with most people being risk averse, the vast majority are content to choose the lowest rates in the market (which are presently 5-year fixed rates).

- While market odds may arguably lend a slight advantage to shorter terms or variable rates, the convenience and “peace of mind” of not having to worry about your mortgage until 2024 (in a 5-year fixed) is completely understandable.

This chart shows Canada’s prime rate and yield spread (i.e., 10-year govt. yield minus Bank of Canada overnight rate. When it goes negative, the yield spread is a popular recession indicator. Roughly speaking, the more negative it goes, the higher the probability of recession and lower rates.)

If you do lock in for five years, please do yourself a favour and pick a lender with a fair-penalty formula (or at least one that lets you increase your mortgage at best rates with no prepayment charge).

That way, you’ll likely pay no penalty or (at worst) pay a reasonable penalty like 3-months’ interest — as opposed to a painful interest rate differential (IRD) charge. This is key if:

- the Bank of Canada ultimately ends up cutting rates and you want to reset your rate lower

- you need a bigger mortgage to upgrade your home or refinance later

- you need to break your mortgage for any of dozens of other reasons.

2 Comments

I’m renewing my investment property (rental) valued at $150.000. Remaining amount is $68.000. With TD.

They offered me 2.77 about 6 weeks ago and then they came back with 2.84. They said the rates went up a bit since we last talked. I initially had 2.89.

Do you think I can still try to get them to honour that 2.77? I meet with them on Tuesday Dec. 10th. That 2.77 is a $75.00 savings in my pocket that I really would like to hold on to.

I also don’t mind taking a 3 year term. Then I would sell it off or even 2 years if the rate is better.

Hi Violet,

Unless you applied before the rate change or got a guarantee in writing, the bank’s quote is generally subject to change.

2.84% is a great rental property rate, however, especially for a renewal on a small loan amount.

But if you can somehow negotiate a materially better 2- or 3-year rate, and are well qualified and financially secure, that may be worth a look too.