log in

log in

The Bank of Canada said today that it’ll keep coasting on rates. But the market isn’t so sure. Investors think our central bank may have to cut sooner than some expect.

Here’s a summary of this morning’s decision:

- Rate Announcement: No change

- Overnight rate: Remains at 1.75%

- Prime Rate: Remains at 3.95%

- Market Rate Forecast: One rate cut in 2020

- BoC’s Headline Quote: “…The Bank will be monitoring the extent to which the global slowdown spreads beyond manufacturing and investment…It will pay close attention to…consumer spending and housing activity–as well as to fiscal policy developments.”

- BoC on GDP Growth: “Growth in Canada is expected to slow in the second half of this year to a rate below its potential.”

- BoC on Inflation: “…The Bank expects inflation to track close to the 2 percent target…”

- BoC’s Full Statement: Click here

- Next Rate Meeting: December 4, 2019

The Spy’s Take

There’s now a clear downward bias in future rate projections. Bond yields, a reflection of future rate expectations, tanked this morning after the BoC announcement.

The 5-year yield, which strongly influences fixed mortgage rates, has plunged 13 bps as of this writing, the most in three months. Needless to say, the market interprets today’s BoC announcement as surprisingly dovish.

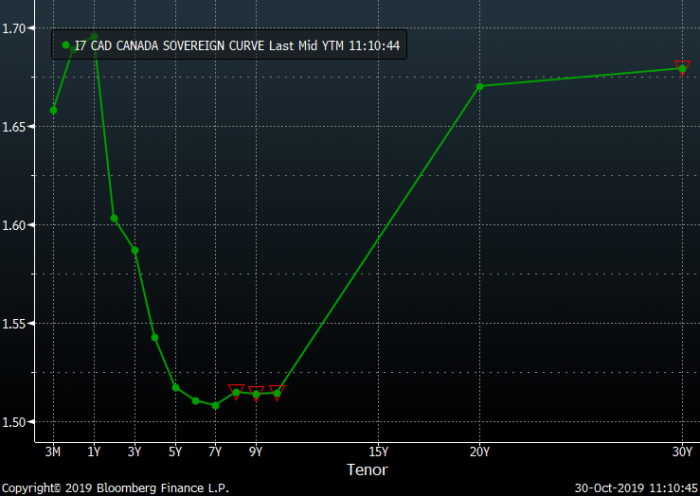

Meanwhile, Canada’s yield curve is still inverted, as this graph below shows. That implies recession risk, a 45% chance estimates Oxford Economics.

With the U.S. expected to cut rates later today, conventional thinking is that this too will sway the BoC lower. And it may. Mind you, as we wrote yesterday, U.S. and Canadian rates can deviate longer than many think.

Trade optimism, continued job growth, broad-based wage growth, a rebounding housing market and improving business sentiment may argue against further cuts, but the question is how long those positive trends will last.

They’re offset by factors like continued consumer debt accumulation, weakening consumer consumption and falling hours worked per worker (which lowers total consumer incomes and spending).

Ultimately, things may have to get much worse or much better for prime rate to change. The BoC says it “expects inflation (its #1 concern) to track close to the 2% target” for the next few years. Continued 2% inflation expectations are little reason to move rates.

The Bank also estimates long-term growth at 1.8%. Sub-2% growth is somewhat more reason to cut, if it persists and if the global slowdown worsens. Hence the downward bias we’re seeing in rate forecasts.

All in all, Canada’s prime rate is like a sailboat with winds blowing in two directions. It likely won’t move too far too fast.

How to Play It

If you give weight to the market’s and the Bank of Canada’s somewhat drab outlook, there are three logical assumptions to make about Canadian rates:

- Rates will slowly resume rising within a few years—if there’s a trade truce and particularly if the U.S. Republicans win in 2020

- Rates will go sideways for at least 1-2 years

- Rates will drop slowly starting in the next 6-18 months.

Trader-types are betting more on #2 or #3.

As a mortgage shopper, picking a term based on this information is fraught with ineffectiveness, given the wildcards that could change the outlook overnight.

But one thing seems more certain. As noted above, rates likely won’t change drastically either way. That means a strategy of choosing the lowest-cost, most flexible mortgage possible still holds. That is, unless a borrower’s mediocre finances and/or psychology dictate a long-term rate lock.

- Today’s best short-term fixed mortgage rates range from:

- Today’s best 5-year fixed rates range from:

- 2.47%-2.49% (insured) to 2.59%-2.69% (uninsured)

- Today’s best variable rates range from:

- 2.64%-2.74% (insured) to 2.74%-2.94% (uninsured)

Consider any shorter term below 2.49% a gift, assuming you’re risk-tolerant and the lender’s terms are fair. That’s especially true for anyone contemplating potential mortgage changes in the next few years.

By contrast, those who:

- plan to stay put and not refinance for five years, and/or

- would be budgetarily strained by rate increases, and/or

- don’t want to spend a dozen hours of their life renewing a mortgage in 1-3 years…

…will find 5-year mortgages still appealing at 2.89% or less.

For all you variable-rate lovers (you still out there?), the bad news is that rate cuts don’t seem imminent. And even if we do get one, there’s a good chance our big banks won’t lower prime rate by the same amount.

With a 1- or 2-year fixed, however, you can still reset lower if rates drop in 2020 or 2021. Short-term fixed rates simply take longer to adjust than variables. On the other hand, they have a much lower starting rate (as of today) and more flexibility to make up for it.

7 Comments

Trump will seal the China deal and buy the economic expansion more time. That and Fed cuts are why stocks are at record highs. No one should expect big rate moves before the U.S. election.

I just sealed an uninsured 5-yr fixed renewal from the green bank at 2.49. They’re willing to buy business it seems

Exceptional rate, Bill, assuming you never need to break the mortgage early and deal with the IRD penalty (which the green bank isn’t as generous with).

@ Bill.

I have an uninsured 5 year variable @ prime -1.15% (2.80%) from a non Big-6, non Credit union. Almost 1 year into the term. On Monday, my lender offered me a 5 yr fixed @ 2.69%. I’ve declined. Would love to know how you got the Big Green to offer 2.49%.

Yes I would like to know too since TD is quoting us 2.94% right now for a 5 year fixed.

Sorry dumb question, but is the “green bank/big green” mentioned aka for TD Canada Trust?

“is the “green bank/big green” mentioned aka for TD Canada Trust?”

exactamundo