It Might as Well Have: On Wednesday, the Bank of Canada threw caution to the wind and changed its playbook. It pledged not to hike rates until “the 2 percent inflation target is sustainably achieved.” The significance of that statement is now sinking in and here’s why. Normally, the Bank of Canada doesn’t wait for inflation to hit 2% before it starts lifting rates. “For example, when the Bank started its tightening cycle in 2017, core inflation was just 1.3%,” writes Capital Economics. But now, the Bank implies it “will wait until inflation has reached 2%, and stays there for some time, before even one rate hike,” Capital Economics says. That may lead to two things:

More Housing Juice: Remember five weeks ago when CMHC was worried about “excessive demand and unsustainable house price growth?” So much for that. Low rates are a propellant for housing. The public is now thinking rates will be anchored to zero for years. And they’re watching in horror as housing inventories fall to a 16-year low. The result: some will fear runaway home prices and start trampling other buyers, Pamplona-style. And if the benchmark qualifying rate ever drops in line with historical averages (or regulators lower the stress test rate as promised), then Katie bar the door, cuz buyers will come knockin. The main question now is, how long the bulls will keep running.

More Rate Timing: Knowing when to convert your variable to a fixed has never been so easy, right? Simply wait until average core inflation (which is the average of the top three numbers on this link) reaches 2%. It’s 1.67% now, and falling. It’ll take many quarters (years?) to get back to target, says the BoC. “…Given that [inflation is] already around zero, we’re more worried about disinflation than inflation,” Governor Macklem admits. Unfortunately, timing a rate lock isn’t as easy as this sounds, and is usually ill-advised. Reason being: when the economy recovers, bond yields—and hence fixed mortgage rates—usually climb without notice, and months before inflation hits 2%.

Fixing Your Floater: Speaking of locking in, if you’re a variable-rater looking to go fixed, here’s a strategy from Rates.ca on how to lock in smarter.

Unavoidable Risk: Canada’s central bank couldn’t be more clear. Keeping rates low is mandatory, despite housing and debt risk. Macklem told BNN Bloomberg this week: “The best predictor of whether somebody is going to pay their mortgage is whether they have a job. And so yes, high household indebtedness is a vulnerability, but supporting the recovery and reducing that vulnerability are entirely aligned and by holding interest rates low across the yield curve, that will reduce debt burdens for Canadians.”

HSBC Retakes the Lead: Canada’s most aggressive purveyor of bank mortgages is at it again. HSBC chopped a slew of rates on Friday, as follows:

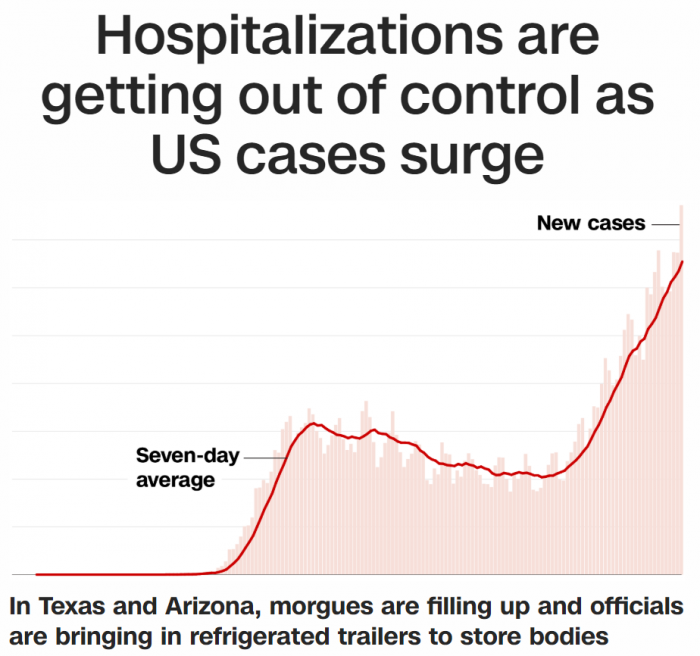

Mixed Signals: If you’re an investor, this CNN story below doesn’t sound bullish. And yet, the floor under bond yields hasn’t cracked (so far), and stocks — a traditional economic barometer — are in a chart pattern that projects potential record highs before year-end. The rate implications are clear. Falling yields would pull down fixed mortgage rates even more, and we’re already setting record lows seemingly every week. But surging stocks are normally not consistent with plunging interest rates. This stock and bond divergence is getting more epic every month. Something’s gotta give. As for which is a better indication of interest rates over the medium term, most traders put their faith in the bond market. It’s notable then that bond derivatives are now projecting (pricing in) an almost 50% chance of negative rates in the U.S. by 2022, according to Bloomberg data.

False Alarm: Social media was abuzz after Blacklocks Reporterpublished a story saying CMHC was spending $250,000 to research “a first-ever federal home equity tax.” That would have been a political firestorm given how many people rely on their home equity for retirement. CMHC quickly put out the facts, however, saying, “The headline and article are both inaccurate and misleading…There is no validity to that headline whatsoever.” More…

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

I am currently in the market and got an offer from TD for five years fixed at 2.04% (uninsured) Purchase price 1.9million mortgage amount 1.2million. Closing end of august but need to sign back by the end of the month. Do you expect the rate to come down further in the next couple of weeks? Is there a chance we can get close to 1.9%?

Hi ovrcpt, Can’t predict the future but it’s possible rates drift a bit lower. If TD drops its official pricing, your TD rate should fall as well. Keep checking back weekly to see if it has: https://www.ratespy.com/best/td-canada-trust-mortgage-rates

By the way, 2.04% is a highly competitive rate on an uninsured $1 million+ mortgage. You did well for yourself.

Sure, lower mortgage rates push housing prices higher, but it wasn’t long ago you wrote about impending defaults when payment deferrals are no longer available. The 10-12% of Canadians that are unemployed won’t be buying a home any time soon, and housing demand should be down without 30,000 new immigrants a month coming into Canada.

In 6-7 months the flu + SARS-Cov2 season should be in full swing, and I think despite low interest rates and massive government spending, February 2021 will see double the mortgage defaults vs. February 2020.

Ralph, That may all be true. For all anyone knows, the market could see a flood of listings in 6-7 months, or not.

There are so many headwinds, and yet it’s impossible to know how home values will unfold — given no one knows:

* If politicians will keep income subsidies going

* If banks will keep deferring mortgages amid high unemployment

* What percentage of the unemployed in six months will be homeowners

* How much the benchmark qualifying rate will drop

* When they’ll open up our boarders

* How corporate bankruptcies will impact employment

* When a vaccine will be widely available

* How many people will panic list their properties

* Etc. etc. etc.

What we do know is that Canada hasn’t slumped into the buyer’s market most expected with 5.5 million jobs negatively impacted by the pandemic. Given all the random unknown variables, predictions are almost better left unmade. Like Churchill said, when the future is foggy, “It’s much better to prophesy after the event has already taken place.”

We have a five year renewal offer on a variable open rate. TD bank has offered 1.92 with our mortgage coming due Sept 01 in Edmonton. I wonder if there is more room to come down?

My friend said he is paying 1.65 with an open hybrid.

I built a new home in 2009 during that financial meltdown and was paying 1.14. Why is it higher now in what looks like worse times than then?

Hey Alan, 1.92% is an exceptional rate for a variable with no penalty. You sure it’s fully open? If so, nice job.

In 2009, most discounted variables ended the year above 2%, so 1.14% seems oddly low. Either way, prime rate was 2.25% back then versus 2.45% today. And the prime overnight spread was 200 basis points versus 220 bps today (due to banks not fully passing through a few BoC rate cuts).

Add up that 20 bps + 20 bps + a 10-20 bps “pandemic risk premium” and that explains the difference.

I could not believe the rate either. Building a new custom home we were working off builders draws that were open until things were complete. We never had a set price with all the changes in finishing and not until the end. Then we stayed open. Our line of credit was closer to 2%. I am going to accept their 1.92 hoping things go lower over the near term. I just can’t see the economy getting much better with all the debt we have at all levels of government.

Higher taxes and employment cuts at the government levels are inevitable?

Hi Marie, Probably not, but it may be the best the broker is willing to do. The lowest rate available depends on your situation. Assuming you’re reasonably well qualified, fill in the fields of these filters and see what else is out there: https://www.ratespy.com/best-mortgage-rates/5-year/fixed

I ‘m currently shopping for a mortgage for my new home purchase that is closing in 5 weeks.

I’m intrigued by the HSBC 2 year fixed at 1.94% uninsured.

If the BOC is suggesting no/minimal rate increases until 2023, isn’t this an attractive option? I can begin shopping for a renewal in 21 months and possibly lock into a similar (or lower) 5 year rate then.

Am I missing something is the risk of a 2 year term fairly muted given the environment today?

Hey Scot, A lot of people are making that same bet, although I like the odds better in a cheaper 1-year fixed for most people over 80% LTV or under 65% LTV.

Many others, however, are happier to forget about their mortgage until 2025 and just lock into a 5-year fixed rate under 2%.

The wildcard is the 5-year bond yield. It’ll start marching higher once it appears core inflation could surge above 2%. That might happen sooner than 21 months or it might happen later. No way to tell. For most folks, the rate risk will likely be manageable either way.

You say the HSBC 5 year insured of 1.89% can be beaten by brokers, really? Please suggest where I should look! I would like to re-finance as rates are now a full 1 percent below what my rate is now.

Hi Scott, Yes, without a doubt HSBC’s 1.89% insured rate can, and is, being beaten in many provinces. See here (make sure the mortgage amount is more than 80% of the home value): https://www.ratespy.com/best-mortgage-rates/5-year/fixed

Note, however, that you’re referring to an *insured* rate but referencing an *uninsured* mortgage type (refinancing). For refis, as noted, HSBC has the lowest nationally advertised 5yr fixed in the game.

Rate isn’t everything, though. Certain lenders have better prepayment options, for example, at just a slightly higher price. By paying that little extra, many people save far more in the end (e.g., if they break their mortgage before five years).

Thanks, I thought HSBC was now posting 1.89 as their switch rate for new mortgages and refis that are not now customers but perhaps I saw that wrong. Love the site, info is appreciated.

log in

log in

{kind=link}

18 Comments

Central banks are building the biggest asset bubbles of all time. This can’t end well.

I’m guessing we can forget about the Department of Finance easing the benchmark rate.

Hi,

I am currently in the market and got an offer from TD for five years fixed at 2.04% (uninsured) Purchase price 1.9million mortgage amount 1.2million. Closing end of august but need to sign back by the end of the month. Do you expect the rate to come down further in the next couple of weeks? Is there a chance we can get close to 1.9%?

Hi ovrcpt, Can’t predict the future but it’s possible rates drift a bit lower. If TD drops its official pricing, your TD rate should fall as well. Keep checking back weekly to see if it has: https://www.ratespy.com/best/td-canada-trust-mortgage-rates

By the way, 2.04% is a highly competitive rate on an uninsured $1 million+ mortgage. You did well for yourself.

Sure, lower mortgage rates push housing prices higher, but it wasn’t long ago you wrote about impending defaults when payment deferrals are no longer available. The 10-12% of Canadians that are unemployed won’t be buying a home any time soon, and housing demand should be down without 30,000 new immigrants a month coming into Canada.

In 6-7 months the flu + SARS-Cov2 season should be in full swing, and I think despite low interest rates and massive government spending, February 2021 will see double the mortgage defaults vs. February 2020.

Ralph, That may all be true. For all anyone knows, the market could see a flood of listings in 6-7 months, or not.

There are so many headwinds, and yet it’s impossible to know how home values will unfold — given no one knows:

* If politicians will keep income subsidies going

* If banks will keep deferring mortgages amid high unemployment

* What percentage of the unemployed in six months will be homeowners

* How much the benchmark qualifying rate will drop

* When they’ll open up our boarders

* How corporate bankruptcies will impact employment

* When a vaccine will be widely available

* How many people will panic list their properties

* Etc. etc. etc.

What we do know is that Canada hasn’t slumped into the buyer’s market most expected with 5.5 million jobs negatively impacted by the pandemic. Given all the random unknown variables, predictions are almost better left unmade. Like Churchill said, when the future is foggy, “It’s much better to prophesy after the event has already taken place.”

We have a five year renewal offer on a variable open rate. TD bank has offered 1.92 with our mortgage coming due Sept 01 in Edmonton. I wonder if there is more room to come down?

My friend said he is paying 1.65 with an open hybrid.

I built a new home in 2009 during that financial meltdown and was paying 1.14. Why is it higher now in what looks like worse times than then?

Hey Alan, 1.92% is an exceptional rate for a variable with no penalty. You sure it’s fully open? If so, nice job.

In 2009, most discounted variables ended the year above 2%, so 1.14% seems oddly low. Either way, prime rate was 2.25% back then versus 2.45% today. And the prime overnight spread was 200 basis points versus 220 bps today (due to banks not fully passing through a few BoC rate cuts).

Add up that 20 bps + 20 bps + a 10-20 bps “pandemic risk premium” and that explains the difference.

Thanks for your insightful comments on my rate.

I could not believe the rate either. Building a new custom home we were working off builders draws that were open until things were complete. We never had a set price with all the changes in finishing and not until the end. Then we stayed open. Our line of credit was closer to 2%. I am going to accept their 1.92 hoping things go lower over the near term. I just can’t see the economy getting much better with all the debt we have at all levels of government.

Higher taxes and employment cuts at the government levels are inevitable?

Hi i am being offered 1.99% fixed for 5 years, is this the best the broker can do?

Hi Marie, Probably not, but it may be the best the broker is willing to do. The lowest rate available depends on your situation. Assuming you’re reasonably well qualified, fill in the fields of these filters and see what else is out there: https://www.ratespy.com/best-mortgage-rates/5-year/fixed

@Marie. I am in QC. My broker is going to negotiate w/ the bank for 1.89% fixed/closed/5yr/uninsured.

Hi Dan, 1.89% is way below market for an uninsured 5yr fixed. Which lender is it?

I ‘m currently shopping for a mortgage for my new home purchase that is closing in 5 weeks.

I’m intrigued by the HSBC 2 year fixed at 1.94% uninsured.

If the BOC is suggesting no/minimal rate increases until 2023, isn’t this an attractive option? I can begin shopping for a renewal in 21 months and possibly lock into a similar (or lower) 5 year rate then.

Am I missing something is the risk of a 2 year term fairly muted given the environment today?

Hey Scot, A lot of people are making that same bet, although I like the odds better in a cheaper 1-year fixed for most people over 80% LTV or under 65% LTV.

Many others, however, are happier to forget about their mortgage until 2025 and just lock into a 5-year fixed rate under 2%.

The wildcard is the 5-year bond yield. It’ll start marching higher once it appears core inflation could surge above 2%. That might happen sooner than 21 months or it might happen later. No way to tell. For most folks, the rate risk will likely be manageable either way.

You say the HSBC 5 year insured of 1.89% can be beaten by brokers, really? Please suggest where I should look! I would like to re-finance as rates are now a full 1 percent below what my rate is now.

Hi Scott, Yes, without a doubt HSBC’s 1.89% insured rate can, and is, being beaten in many provinces. See here (make sure the mortgage amount is more than 80% of the home value): https://www.ratespy.com/best-mortgage-rates/5-year/fixed

Note, however, that you’re referring to an *insured* rate but referencing an *uninsured* mortgage type (refinancing). For refis, as noted, HSBC has the lowest nationally advertised 5yr fixed in the game.

Rate isn’t everything, though. Certain lenders have better prepayment options, for example, at just a slightly higher price. By paying that little extra, many people save far more in the end (e.g., if they break their mortgage before five years).

Thanks, I thought HSBC was now posting 1.89 as their switch rate for new mortgages and refis that are not now customers but perhaps I saw that wrong. Love the site, info is appreciated.