log in

log inThe Mortgage Report: March 8

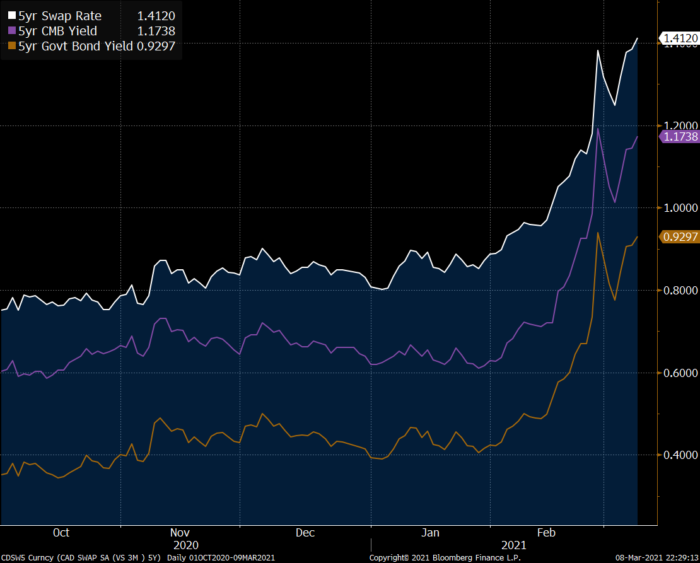

Source: Bloomberg

- It was one year ago that Canada’s 5-year yield plunged to an all-time low of 0.27%. Since then, it has more than tripled — and the bond market hasn’t taken a breather.

- Investors keep dumping bonds and driving up yields. They fear things like:

- inflation

- excessive government borrowing and stimulus

- the end of government bond-buying (which helped keep rates lower throughout the pandemic).

- Virtually every metric lenders use to set fixed-rate mortgage pricing is surging, including swap rates, Canada Mortgage Bond yields and government yields (all seen in the above chart).

- The good news is, lenders have been slow to hike retail mortgage rates. You can still find deals O’ plenty on 5-year money. Most lenders are still under 2% today, and we suspect you’ll find sub-2% deals for many days to come.

- Fun fact: This is the first March ever where 5-year fixed mortgage rates are below 2%.

- The bad news is:

- more banks are lifting fixed rates (we heard from reps at two major banks today that are boosting fixed rates 10+ basis points this week)

- depending on how hawkish the BoC’s announcement is on Wednesday, yields could potentially see another burst

- Side note: In Q4 2020 and Q1 2021, the economy ran twice as hot as the Bank of Canada had forecast. It has to acknowledge this. If our central bank can be that wrong about GDP, it can be that wrong about its 2023 rate-hike forecast. That’s partly why the bond market expects the first rate hike next year.

- most economists think the BoC will announce a tapering of its bond purchases by April’s rate meeting.

- The message: Any and all of these developments could lift fixed mortgage rates further. So, if you need financing and haven’t locked in a rate yet, you’ll likely pay more before the end of next month.

That In-the-money Feeling

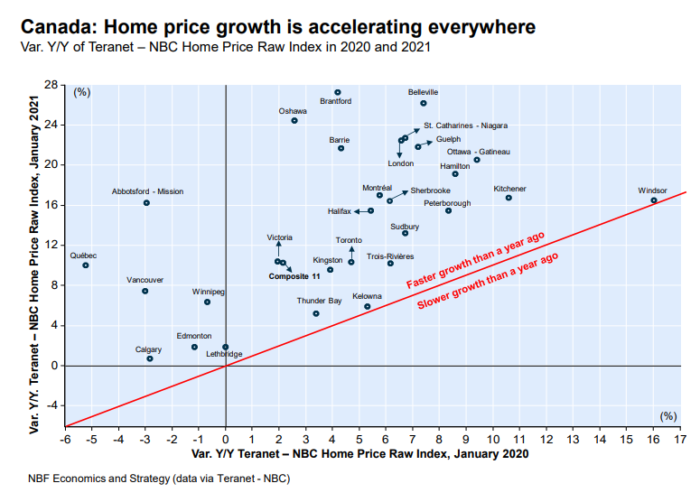

- Where could inflation come from? Lots of places, not the least of which is post-lockdown spending fuelled by housing wealth.

- As National Bank of Canada writes, price growth accelerated in all 32 markets it tracks in January. That hasn’t happened since 2010. Unless fleeting, all those equity gains will make countless consumers borrow more and spend more than they otherwise would, bolstering demand later this year.

- Other things equal, more demand amid static supply results in price pressures. Price pressure drives up inflation expectations. Rising inflation expectations increase chances of earlier BoC rate hikes.

New Mortgage Rules in the Wings?

- Scotiabank warns to “be on guard for macroprudential measures in a Spring budget…Ottawa has been caught completely off-guard in the magnitude of the housing response to very low financing costs.”

- And now, regulators are being publicly accused of “blowing” a big housing “bubble” (see Post story). Price inflation is pushing debt ratios to the max. A record 23% of non-default insured borrowers had a loan-to-income (LTI) ratio of 450% as of Q4, reports NBF.

- Ever since the Bank of Canada raised the profile of LTI last decade, government officials have kept an eagle-eye on this metric. Excessive LTI readings have been used as justification for at least two mortgage rule tightenings in the past.

3 Comments

Thank you Spy. I’ve just researched a bit about loan-to-income (LTI) ratio but can’t seem to find a clear answer. What is it exactly? The total loan (mortgage) value divided by yearly gross or net income? Is it something else? Most material you find on the web is about debt-to-income ratio, which is something else. Thank you.

All things being equal, should well qualified borrowers at fair penalty lenders switch from deeply discounted ARMs (P – 90bps or better) into 5 year fixed?

Hey Dave, Rate predictions are a dice game but if one relies on implied market forecasts, uninsured 5yr fixed rates win based on projected interest cost alone. This assumes NO changes are made to the mortgage for five years.