log in

log inIf low rates are a yard party, the Bank of Canada has just turned up the lawn sprinklers.

If low rates are a yard party, the

If low rates are a yard party, the Here’s a rundown of what they just did:

- Rate Decision: They increased the overnight rate 25 bps

- Prime Rate: Should jump to 3.70% this week

- Market Rate Outlook: 2+ more hikes by year-end 2019

- BoC GDP Outlook: “Average growth of close to 2% over 2018-2020″ (i.e., not too hot, not too cold)

- BoC’s Headline Quote: “…Higher interest rates will be warranted to keep inflation near target and [we] will continue to take a gradual approach, guided by incoming data…the Bank is monitoring the economy’s adjustment to higher interest rates and…capacity and wage pressures, as well as the response of companies and consumers to trade actions…”

- BoC’s Full Statement: Click here

- Next Rate Meeting: September 5, 2018

The Spy’s Take: Prime rate hasn’t seen these levels in over nine years (November 2008). The hike means payments will rise roughly $12-13 a month (per $100,000 of mortgage) for those in adjustable rate mortgages. The BoC is leaning towards additional rate hikes and everyone should prepare for that possibility. Mind you, unpredictable economic developments could sidetrack those hikes in the wink of an eye (Trump slapping new tariffs on Canada, for example). “The possibility of more trade protectionism is the most important threat to global prospects,” says the Bank.

*****

The Good News

Like they say, a rate hike today is worth two in the bush.

Actually, few people say that but it’s true. By tightening monetary policy today there’s less chance the Bank of Canada falls behind inflation, allowing it to overheat. If that ever happened, Canada would need rapid (more painful) rate hikes later. And that could be nightmarish for many debt-heavy consumers.

Fortunately, “the effect of [recent tariffs] on Canadian growth and inflation is expected to be modest,” the BoC projects.

How High Can Rates Go?

Since the dawn of inflation targeting (1991):

- The average Bank of Canada rate hike cycle has lasted 2.29 percentage points.

- That’s measured from the trough to the peak of rates in each cycle.

- The average rate-tightening cycle has lasted just over a year.

So far, we’re well along the way, up one percentage point in the last 12 months.

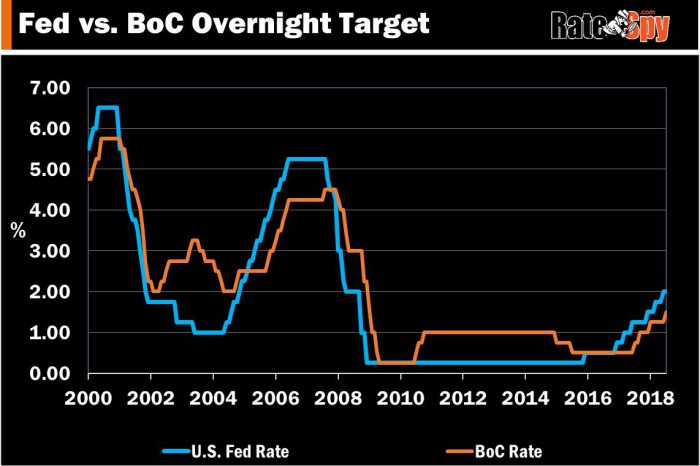

Analysts expect the Bank of Canada to remain within 50-75 bps of the U.S. Fed’s policy rate (the spread after today is 50 bps). That spread seldom exceeds 100 bps, but in the last 25 years it’s been as high as 250 bps. In other words, U.S. and Canadian rates can deviate for many months.

Ways to Play It

- Shopping for a brand new mortgage with good qualifications, risk tolerance and sufficient savings?

- Consider a variable rate mortgage. Prime – 1.00% or better (if you can get it) gives you a big head start. The risk of variable is arguably declining the higher rates go.

- Need a brand new mortgage but are more rate sensitive?

- Consider a 4-year fixed rate. You’ll save over 10-30 basis points versus most 5-year fixed mortgages, with more flexibility to refinance sooner without penalty.

- Note: There are no good 4-year fixed rates for refinances. So if you need rate hike protection on a refi, consider a 5-year fixed instead.

- In a variable-rate mortgage already?

- Prepare for the possibility of at least 50-75 bps of additional hikes.

- If you absolutely need to lock in, carefully compare fixed rates at other lenders and compare them to what your current lender is quoting. Consider the overall savings/cost by factoring in your penalty (typically 3-months’ interest) and switch costs. Most lenders quote mediocre rates on variable-to-fixed conversions so you might be better off locking in elsewhere.

4 Comments

I am getting 5yr-variable for 2.7 vs 5yr-fixed 3.2. I am paying 20% down. I am thinking to consider 3.2@5yr fixed. Although the saving is not much between the two but it will be save to lock for 5 yr. Is that correct thought

Mj, A few questions….

Is the mortgage for a purchase, switch/renewal or refinance?

What city is the property in?

What is the mortgage amount and home value?

It is for purchase of townhouse in Mississauga and mortgage amount is 450 and it is my first home. i do have commitment letter/approvals from few top banks (RBC, BMO)

would you help me with correct decision as after one month closing is there

Hey MJ, If the home value is under $1 million and all borrowers meet typical prime lending guidelines, then the best:

* Variable rates are less than 2.50% ( https://www.ratespy.com/best-mortgage-rates/5-year/variable )

* 5yr fixed rates are as low as 3.10% or less ( https://www.ratespy.com/best-mortgage-rates/5-year/fixed )

So you might want to shop around a bit more. A 0.10%-point lower rate amounts to a nominal interest savings of ~$2,100 on $450,000 over five years. Some of these discount lenders also have lower penalties than the big banks.

There’s not enough information to recommend whether a fixed or variable is best for you, but check out this fixed or variable rate checklist for some guidance.

Lastly, make sure you don’t take too long. Leave yourself at least 3-4 weeks to close.