Unfortunately, 1.29% is only available on high-ratio insured purchases in Ontario.

Elsewhere in the nation, you can now find variables as low as prime – 1.03% (insured) through online brokers. That’s a still-not-shabby 1.42%.

Barring another unplanned economic crisis, there are two things you can bank on:

More prime – 1.00% deals to drop before year-end

More interest in variables, once that happens — especially since 2021 looks like a year where rate-hike risk is nil.

Securitization Drives 1- and 2-year Deals

With all of the falling rates and refinancing going on since the spring, lenders who securitize mortgages (i.e., sell big lots of them to investors) have been forced to pull countless mortgages out of securitization pools.

When that happens, lenders need new mortgages with similar terms (mostly shorter terms like one and two years) to replace them. Lenders then put these new short-term mortgages (called “replacement assets”) back into the pools.

This need for replacement assets—along with a general decrease in short-term rates—are key reasons why we’re seeing the best one- and two-year rates we’ve ever seen, like 1.24% one-year fixed rates on insured and insurable mortgages.

Yields Climb Ahead of Election

Canada’s 5-year yield closed above 0.40% for the first time in two months on Friday. But more importantly, the most-watched bond in the world (the U.S. 10-year) closed at its highest in almost five months.

Canadian rates are slowly following U.S. rates higher amid uncertainty (fear) surrounding a Joe Biden presidency.

On that note, U.S. stocks just had their worst week ever before an election, reports Bloomberg.

A Biden win would likely explode spending, deficits and bond issuance—even more so than a Trump victory.

“A blue (Democratic) wave means more supply and therefore higher rates,” Priya Misra, global head of rates strategy at TD Securities, told FT.

“…We would expect a material backup in longer-term sovereign bond yields” following a Democratic sweep, said Goldman Sachs in a research note this month.

Given the strong link between U.S. and Canadian rates, that suggests a Biden White House could be potentially bullish for Canadian fixed mortgage rates, as soon as 2021. (Albeit, there is virtually no danger of a prime rate increase in 2021.)

Meanwhile, on This Side of the Border

Not to be outdone by the Americans, the Trudeau government will run wild with spending in its own right. Already, Canada is vying for the highest deficit-to-GDP-ratio in the universe.

That means the Bank of Canada, which wants 5-year yields to stay low to encourage borrowing, will soon have its hands full. Why? Because Ottawa must issue a mammoth amount of bonds to finance all of its economic stimulus. With yield curve control “most likely coming in 2021,” according to CIBC Capital Markets rate guru Ian Pollick, the implication is that the BoC may have to buy a slew of 5-year bonds (or at least threaten to). That might be the only thing stopping Ottawa’s disgorgement of bond supply from taking rates to pre-COVID highs.

This begs the question: How much more buying can the BoC do, given 80% of Government bonds issued since March are already held by the central bank? The BoC doesn’t want to corner the 5-year bond market. It’ll eventually have no choice but to let market forces take yields higher.

The BoC Effect is Waning

We’re probably not far from the cycle bottom in fixed mortgage rates. CIBC economist Ben Tal told BNN Bloomberg that the Bank of Canada’s quantitative easing announcement this week could result in “maybe five basis points [of fixed rate reductions] if we’re lucky…”

“…You’re not going to take a mortgage…based on these five basis points.” he said. “Interest rates are so low to start with…the effectiveness of monetary policy in this environment is approaching zero”

David Rosenberg estimates the total net effect of BoC intervention on 10-year rates has been “a maximum reduction of roughly 30 basis points.”

The “impact of the Canadian quantitative easing adventure is dwarfed by the effects of the U.S. interventions,” he adds.

Harsh Penalty Anecdote # 3,289,347

We hear from readers all the time who are blindsided by mortgage penalties. In this latest case, the borrower is actually a mortgage lender executive himself. He works for a smaller prime mortgage lender, but got his mortgage through RBC. He wanted to refinance and wrote to me, saying:

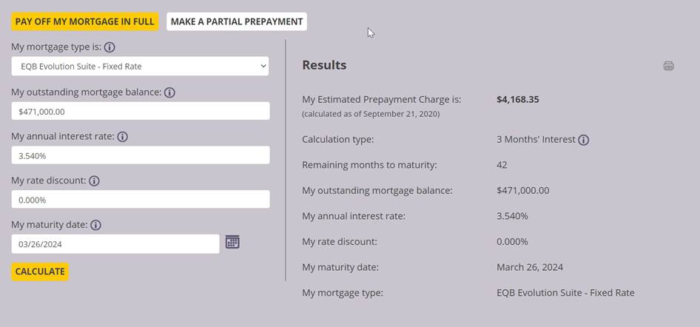

“Rob, it pains me to write this… but hope it’s helpful for other borrowers…[My RBC] prepayment charge exceeds $18,302 using their IRD calculation. If I was with [a fair penalty lender], this prepayment charge would be offset in roughly half of a year. With RBC, it takes 2.5 years.” (Note: We validated this by running the customer’s data through Equitable Bank’s prepayment calculator below.)

It just goes to show for the X-millionth time, even smart industry-types who should know how brutal penalties can be—tend to minimize the significance and the likelihood of prepayment charges.

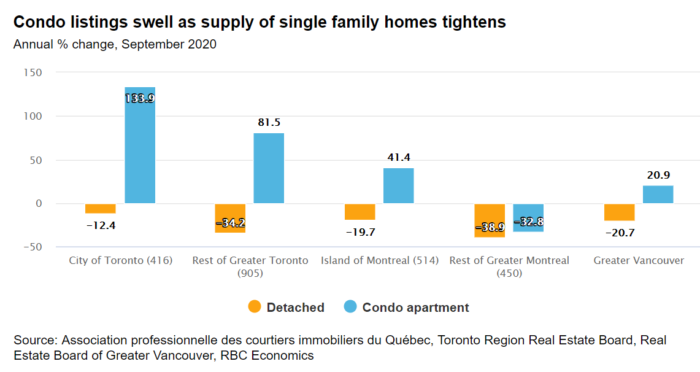

The race for space is on, all across the country. How long will the condo-to-house shift last? Perhaps until immigration gets back to full throttle and vaccines become available, well into 2021.

One Reason Why Home Prices Didn’t Crash

“Generous government income support programs for households most affected by COVID-19…made it easier to carry mortgage payments,” says RBC, as did 1+ million mortgage payment deferrals. “Overall, Canadian households received more money ($56 billion) from government aid programs…than they lost in wages and salaries due to the pandemic ($23 billion).”

Immigration Gusher

If you’re hoping for more immigration to support home prices, you’re in luck. The government just announced that it’s boosting its immigration target by 50,000 people a year to:

401,000 in 2021

411,000 in 2022

421,000 in 2023

“Since its founding in 1867, Canada has welcomed at least 300,000 immigrants in a year just five times,” writes CIC News. “Between January and August of 2020, Canada has [let in] 128,400 immigrants…”

Quotable

“Canada’s capital markets are really priced off U.S. capital markets.”—Economist, David Rosenberg

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Will the fair penalty banks offer same size mortgage for investment properties like big 6 banks? Since I know BMO and RBC are taking lots of rent as income so I can get higher mortgage credit amount.

Great question nbf2008, Depends on the lender. You’re absolutely right that if more favourable rental income treatment is necessary to get your debt ratios in line, rate and penalty considerations are usually secondary. But there are several lenders with equivalently good rental income treatment.

Hi RateSpy I am your article’s regular reader. We bought townhouse in feb2020 got posession 1stApril 2020. Due to uncertainty TD broker suggested to go with variable which was a great decision.

2.64 prime minus -.76 which is 1.83% variable 5yrs term we didn’t know that you can negotiate the rate even if its variable. Is it possible to contact them now to reduce further because recently rates went down further but our rate is the very same from day one. How we can call it variable then? Thank you

If you really have a variable at TD mortgage prime – 0.76%, the rate should be 1.84%. If that is indeed what you have and your mortgage is already closed then you cannot negotiate the rate any further.

log in

log in

4 Comments

Will the fair penalty banks offer same size mortgage for investment properties like big 6 banks? Since I know BMO and RBC are taking lots of rent as income so I can get higher mortgage credit amount.

Great question nbf2008, Depends on the lender. You’re absolutely right that if more favourable rental income treatment is necessary to get your debt ratios in line, rate and penalty considerations are usually secondary. But there are several lenders with equivalently good rental income treatment.

Hi RateSpy I am your article’s regular reader. We bought townhouse in feb2020 got posession 1stApril 2020. Due to uncertainty TD broker suggested to go with variable which was a great decision.

2.64 prime minus -.76 which is 1.83% variable 5yrs term we didn’t know that you can negotiate the rate even if its variable. Is it possible to contact them now to reduce further because recently rates went down further but our rate is the very same from day one. How we can call it variable then? Thank you

Hi Sohail, What does the 2.64% represent?

TD’s Mortgage Prime Rate is 2.60%

If you really have a variable at TD mortgage prime – 0.76%, the rate should be 1.84%. If that is indeed what you have and your mortgage is already closed then you cannot negotiate the rate any further.