By The Spy on

February 22, 2021

People hear the Bank of Canada predicting no rate increases until 2023 and take that as gospel. Maybe they shouldn’t. The Bank of Canada’s key overnight rate—which more directly impacts floating-rate mortgages—doesn’t constrain fixed mortgage rates in the same way. The latter are driven more by what the bond market thinks the Bank of Canada (and the economy) will do...

read more

By The Spy on

February 18, 2021

A scattering of lenders are starting to warn of impending rate increases. No surprise—given Canada’s 5-year bond yield, which drives fixed mortgage rates, hit a new relative high on Thursday. At 0.60%, it’s now the highest it’s been since April 9, 2020. When the 5-year yield was last at these levels, your typical discretionary 5-year fixed rate at a Big...

read more

By The Spy on

February 16, 2021

The entire mortgage market was waiting, and now, after 10 months, it finally happened. Canada’s 5-year bond yield (which influences fixed mortgage rates) broke through major resistance, resistance that goes all the way back to April of last year. It’s a signal that better economic times lie ahead. A sign that inflation should no longer be just an afterthought. A...

read more

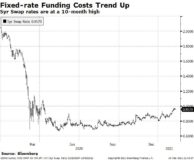

By The Spy on

February 10, 2021

It’s not getting any cheaper for banks to fund a fixed-rate mortgage. In fact, Canada’s 5-year swap rate, a common measure of 5-year funding costs at the big banks, is running at a 10-month high. Yet, still we’re seeing lenders trim 5-year fixed rates as the cut-throat spring market approaches. RBC chopped its 5-year fixed by 18 bps last week....

read more

By The Spy on

February 6, 2021

5-year fixed mortgage rates tend to shadow 5-year government yields. And for most of nine months, the 5-year yield has been locked in a 21-basis-point range, a range so tight it was practically inconceivable prior to COVID. And, while no one has ever seen a range like this in our lifetimes, ultimately the 5-year yield will break out. When that...

read more

By The Spy on

January 27, 2021

Despite record-low short-term interest rates, most banks are offering junk 1-, 2- and 3-year rates on uninsured mortgages through the broker channel. We’re seeing 5-year variable pricing as low as 1.45% or less at major banks. Yet, on a one-year fixed, for example, they quote mortgage brokers over 2.40%. That’s well above the discretionary rates bank customers are reporting to...

read more

By The Spy on

January 14, 2021

Variable rates on new mortgages could get a little cheaper this quarter, for one of four reasons, or maybe all four: Bankers’ acceptance (BA) rates — a general proxy for variable-rate funding costs — are at an all-time low. That’s boosted the spread between prime rate and BAs to almost a 12-year high. Think of that spread as a rough...

read more

By The Spy on

January 6, 2021

The Mortgage Report: Jan. 6, 2021 U.S. 5-year yields leaped to a 7-week high on Wednesday as Democrats took control of all three houses of government, thanks to their historic win in Georgia. Canada’s 5-year yield rose in sympathy by a less notable 2 bps, but economists nonetheless expect more of an incline in rates this year. The reason: Democrats...

read more

By The Spy on

January 4, 2021

The Mortgage Report: Jan. 4, 2021 2020 was a year that took pleasure in humiliating forecasters. From the remarkable bounce in housing, to the resilience of mortgage volumes, to the devastation in big-city rental markets, to the homeowner exodus from urban cores to the lows of contract mortgage rates, to the persistence of high qualifying rates — 2020 made the...

read more

By The Spy on

December 24, 2020

“Vaccines have come too late to avoid a bleak winter,” said Capital Economics in a report last week. The market agrees. Canada’s two-year bond yield, often used to forecast Bank of Canada rate policy, hit a record low on Thursday. That coincides with recent BoC comments that it could cut the overnight rate by less than the standard 25 basis...

read more

log in

log in