Fed boss Jerome Powell pledged Wednesday that he would not hike U.S. interest rates “preemptively based on forecasts.” In saying that, the Fed once again left U.S. rates unchanged.

But more importantly, it left its general rate outlook unchanged, meaning a consensus of its members still project no Fed rate increases through 2023.

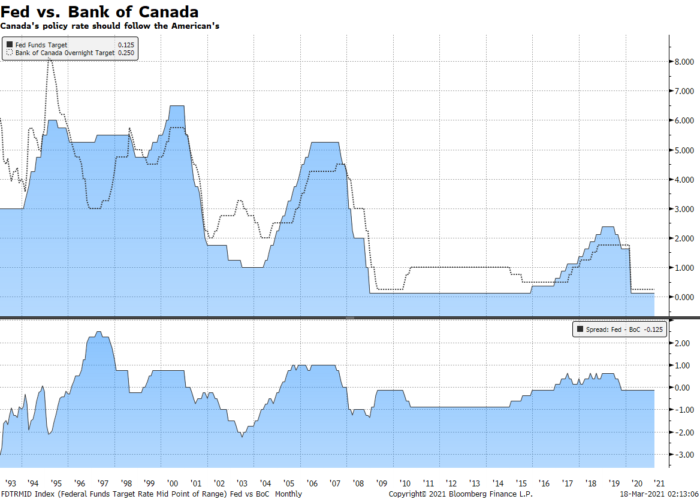

If history repeats, the Bank of Canada will likely start its rate hike cycle within 2 to 4 months of the Fed’s first move.

As inflation heats up, that rate hike timeframe will be a moving target. The Fed expects above-normal price level increases for the next three years, and it reiterated that it’s willing to let inflation run hot.

But some worry the Fed may be caught napping. If a central bank gets too far behind the curve on slowing inflation, price levels can rise faster than expected, requiring more drastic policy tightening later. That’s a rare outcome but one where you’d definitely want to be in a fixed-rate mortgage.

Source: Bloomberg

On the Canadian Front

Canadian bond yields fell on the Fed news, easing some of the upward pressure on fixed mortgage rates.

We continue to see lenders of all sorts boosting fixed rates. Among the heavy hitters this week:

National Bank boosted the following special fixed rates:

4yr: 2.19% to 2.29%

5yr: 2.24% to 2.34%

Tangerine lifted these fixed rates:

4yr: 1.74% to 1.89%

5yr: 1.89% to 2.04%

7yr: 2.49% to 2.64%

10yr: 2.84% to 3.09% (a far cry from its 2.14% last month!)

Typical uninsured5-year fixed rates at the major banks are being quoted in the 2.09% to 2.14% range on a discretionary basis, but we’re still seeing well-qualified borrowers getting 1.99% to 2.04%—and 10 basis points better if the mortgage is insured.

Variables are down to prime – 1.00% to prime – 1.05% at the major banks. That’s 70+ basis points cheaper than a 5-year fixed, a spread that’s been steadily widening. At current uninsured rates, it would now take 5+ BoC rate hikes in 2023 for a 5-year fixed to end up cheaper, based on interest cost alone.

Are 5+ hikes possible? Here’s a look back in time at how much prime rate rose in the previous four rate cycles. While weighing that possibility, we should also acknowledge that we’re swimming in new waters (unparalleled stimulus, home price appreciation, surging commodity prices, record savings, “buy domestic” mandates, supply disruptions, etc.). Hence, inflation is a legit threat, as is a growing supply of government debt—another bullish factor for fixed mortgage rates.

Fun fact: The number of people Googling “inflation” is the highest in years, reports Barrons. That’s interesting, as consumer sentiment is a powerful thing. In fact, concern about inflation often leads to inflation.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Hey VK, There’s a solid chance you’ll come out ahead in that 1.59% 5yr fixed, versus shorter/variable terms, particularly if you ride out the mortgage to term (the full five years) or if you chose a fair-penalty lender with transparent rates.

Hi, Bank is offering me 1.35% , 5 year variable with 1500$ cash back. on my first home purchase. Should i take this offer or shop around for a fix rate ?

log in

log in

4 Comments

I was in doubt for long time, finally decided for 5 year fix on 1.59 while closing my purchase last week. Stability was key….

Hey VK, There’s a solid chance you’ll come out ahead in that 1.59% 5yr fixed, versus shorter/variable terms, particularly if you ride out the mortgage to term (the full five years) or if you chose a fair-penalty lender with transparent rates.

Hi, Bank is offering me 1.35% , 5 year variable with 1500$ cash back. on my first home purchase. Should i take this offer or shop around for a fix rate ?

Hi Moe,

Have a read through this before selecting a term: https://www.ratespy.com/fixed-or-variable-rate-the-decision-checklist-02223752

Use this to figure out what that $1500 is worth in terms of rate discount: https://www.ratespy.com/mortgage-rate-comparison-calculator